March 19, 2026

Variable Private Mortgages Surge to 26% Market Share: Toronto Borrowers’ Playbook Amid BoC Hold and 3.9% Rates

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s mortgage market just sent a clear signal: borrowers are voting with their wallets, and variable is winning. As Variable Private Mortgages Surge to 26% Market Share: Toronto Borrowers’ Playbook Amid BoC Hold and 3.9% Rates becomes the defining story of 2026, Rates.ca data confirms that variable-rate uptake has nearly doubled since 2024 — and private lenders are quietly filling the gaps that banks leave behind. [1]

Key Takeaways 📌

- Variable rates now hold 26% market share in Toronto, up from 11–18% in 2024, driven by the Bank of Canada’s hold at 2.25% [1][7]

- Private variable mortgages start at 8.99%+, trading higher costs for accessibility — ideal for self-employed, credit-challenged, or equity-rich borrowers [1][2]

- Bank variable rates (3.34%–3.65%) can save ~$5,628/year versus a 5-year fixed at 3.64% in the current stable environment [1]

- GTA benchmark prices stabilized at $938,800 in February 2026, creating a buyer’s market where flexible mortgage structures matter more than ever [1]

- Private lending is projected to reach ~20% of Ontario mortgages in 2026, with FSRA increasing oversight as a top regulatory priority [1][2]

Why Variable Private Mortgages Surge to 26% Market Share Matters Right Now

The BoC Hold That Changed Everything

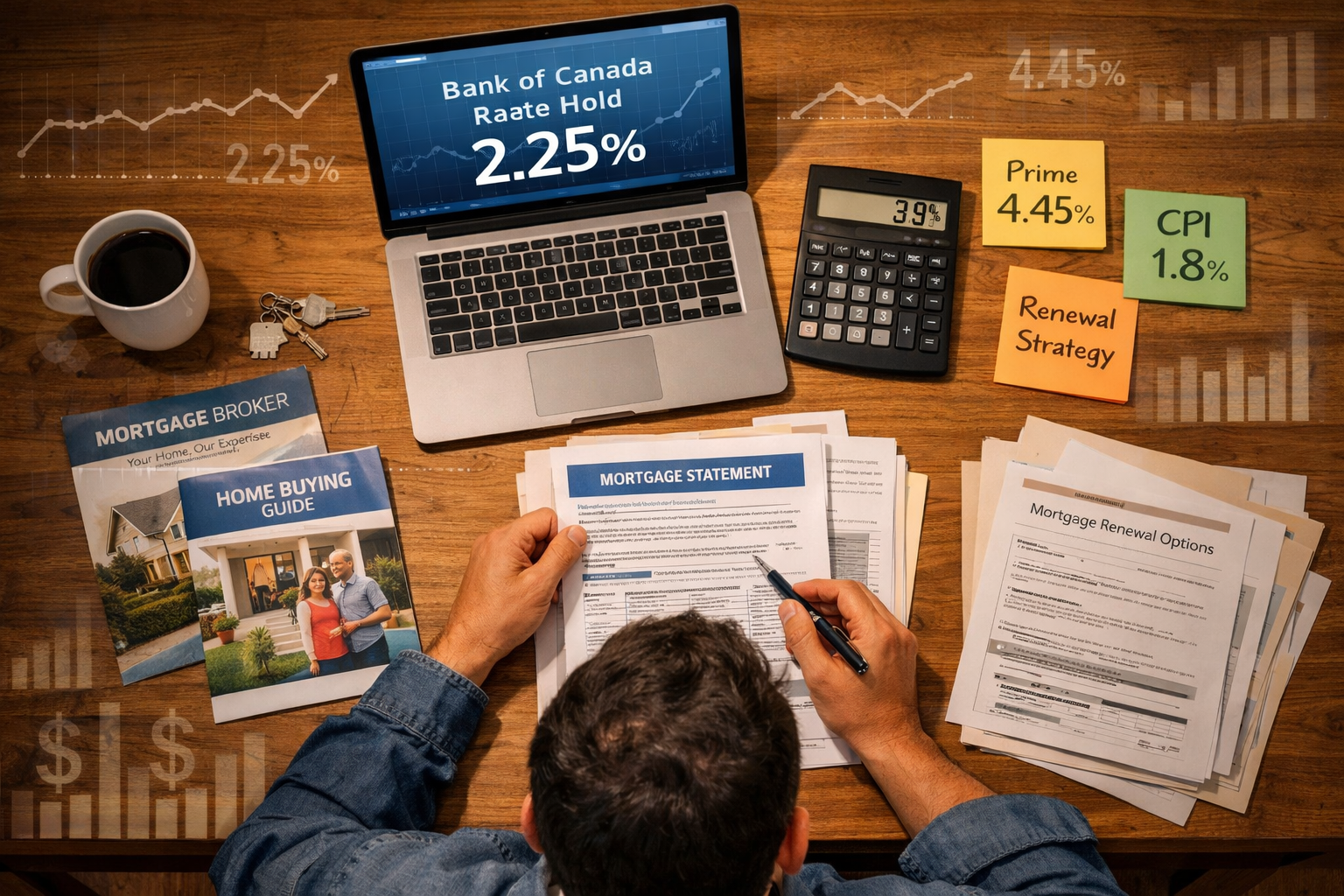

On March 18, 2026, the Bank of Canada held its policy rate at 2.25% — citing Middle East conflict risks, oil price spikes, and broader economic uncertainty. [8] That decision was a gift to variable-rate borrowers. With the prime rate sitting at 4.45%, bank variable mortgages are now priced between 3.34% and 3.65%, while fixed 5-year rates hover around 3.64%. [1]

The math is simple: when the spread between fixed and variable shrinks to roughly 30 basis points, paying a premium for payment certainty becomes hard to justify. TD Bank economist Andrew Hencic expects the BoC to stay sidelined amid oil shocks and US tariff pressures, keeping variable rates stable in the short term. [1]

💬 “This is a rare opportunity for Toronto variable-rate borrowers — the BoC hold at 2.25%, combined with convertibility options, makes variable the smart play right now.” — Mortgage Broker Manzeel Patel [1][2]

What the 26% Number Actually Tells Us

Variable rates climbed from 11–18% market share in 2024 to nearly 30% in 2025, before settling at 26% in early 2026. [1][7] That’s not a blip — it’s a structural shift. Borrowers burned by the 2022–2024 rate hike cycle are returning to variable, but this time with eyes open.

CPI inflation dropped to 1.8% in February 2026 (down from 2.3% in January), while unemployment climbed to 6.7%. [1] Both signals point toward rate stability or even modest cuts — exactly the environment where variable rates outperform. Mortgage Sandbox forecasts variable rates to remain stable until at least mid-2026, favoring them for cash-flow-strong borrowers over fixed amid narrow spreads. [5]

To understand how trigger rates work in a variable environment — and when they become a risk — see this essential guide to trigger rates in variable mortgages.

Bank Variable vs. Private Variable: Knowing the Difference 🏦

Side-by-Side Comparison

| Feature | Bank Variable | Private Variable |

|---|---|---|

| Rate Range | 3.34% – 3.65% | 8.99%+ |

| Qualification | Stress test required | Equity/asset-based |

| Ideal Borrower | Strong credit, T4 income | Self-employed, credit gaps |

| Annual Savings vs. Fixed | ~$5,628 | Varies by deal |

| Convertibility | Often available | Deal-dependent |

| FSRA Oversight | Bank Act regulated | Increasing scrutiny |

Sources: [1][2][5]

When Private Variable Makes Sense

Private variable mortgages are not a consolation prize — they’re a strategic tool. Here’s who benefits most:

- 🏗️ Self-employed borrowers who can’t document income through traditional T4s (explore current self-employed mortgage options in Toronto)

- 🔄 Renewers facing rate resets who need bridge financing while improving their credit profile

- 🏠 Equity-rich homeowners with non-traditional income streams

- ⚡ Borrowers in time-sensitive deals where bank approval timelines don’t work

Experts Ryan MacNeil and Neal Andreino (Canadian Private Lenders Podcast, February 2026) predict private lending growth will be driven by renewals and market volatility — not just credit issues. [1][2] This is a critical distinction: private lending is becoming mainstream, not marginal.

For a deeper look at how private mortgages work in Ontario, the mechanics are worth understanding before committing.

The Cost of Access

Yes, private variable rates starting at 8.99% are significantly higher than bank rates. But for borrowers who cannot access bank products, the comparison isn’t private vs. bank — it’s private vs. nothing. The real question is whether the flexibility and access justify the cost, and for many Toronto borrowers in 2026, the answer is yes. [1][2]

The impact of rate resets and the renewal wave is pushing thousands of borrowers into exactly this decision point right now.

The Toronto Borrower’s Playbook: Navigating Variable Private Mortgages in 2026

Step 1: Assess Your Rate Environment Honestly

The GTA benchmark home price stabilized at $938,800 in February 2026, down 7.9% year-over-year. [1] A buyer’s market means negotiating power — but it also means lenders are being selective. Before choosing variable, ask:

- ✅ Can your cash flow handle a rate increase of 50–100 bps without stress?

- ✅ Is your credit profile improving (making a short-term private variable a bridge strategy)?

- ✅ Does your lender offer convertibility to fixed if rates shift?

For a full breakdown of how these two rate types compare, the comprehensive guide to fixed vs. variable rates is essential reading.

Step 2: Understand the Stress Test Reality

Bank variable borrowers still face the mortgage stress test — qualifying at the higher of their contract rate plus 2%, or 5.25%. [1] This is why some fully qualified borrowers end up in private channels: not because of credit, but because of qualification math.

Understanding stress testing in the Canadian mortgage market can help borrowers prepare their application strategically rather than being surprised at approval time.

Step 3: Build Your Exit Strategy

Private variable mortgages are almost always short-term instruments — typically 1-year terms. The playbook is:

- Enter with private variable for access and flexibility

- Improve credit score, document income, reduce LTV

- Exit to a bank variable or fixed product at renewal

📊 Private lending is projected to hit ~20% of Ontario mortgages in 2026, with FSRA increasing oversight as a top priority for 2025–2026. [1][2]

Working with an experienced broker is critical here. A good broker knows which private lenders offer the cleanest exit ramps. Learn more about what a mortgage broker can do for you in a complex rate environment.

Step 4: Watch the Macro Signals

The BoC’s March 2026 hold was influenced by oil price volatility, US tariff uncertainty, and geopolitical risk. [8] These same factors could trigger a cut — or a hold — at the next decision. Variable borrowers should monitor:

- 📈 CPI inflation (currently 1.8% — below the 2% target) [1]

- 📉 Unemployment rate (6.7% and rising) [1]

- 🌍 Global oil prices and US-Canada trade dynamics

The shifting lender market shares and implications for broker strategies article offers useful context on how lender competition is reshaping the variable rate landscape.

Conclusion: Variable Private Mortgages in 2026 — Opportunity With Eyes Open 👁️

The Variable Private Mortgages Surge to 26% Market Share: Toronto Borrowers’ Playbook Amid BoC Hold and 3.9% Rates story is ultimately about one thing: strategic flexibility in an uncertain market. The BoC hold at 2.25%, combined with stable GTA prices and a growing private lending ecosystem, has created a genuine window for Toronto borrowers to leverage variable products — both bank and private — in ways that weren’t possible during the 2022–2024 hike cycle. [1][7][8]

✅ Actionable Next Steps

- Compare your renewal options now — don’t wait for your lender’s renewal offer

- Get pre-qualified for both bank and private variable products to understand your full range of options

- Stress-test your own budget at rates 1–2% higher than today’s variable rates

- Consult a licensed mortgage broker who has access to both A-lender and private channels

- Set a rate-watch alert for BoC decision dates (next announcement: April 2026)

The borrowers who win in 2026 won’t be the ones who guessed the rate direction perfectly — they’ll be the ones who built flexible, exit-ready mortgage structures from the start.

References

[1] Variable Private Mortgages In Toronto Why Theyre Gaining Traction Amid 2026 Rate Stability – https://everythingmortgages.ca/blog/variable-private-mortgages-in-toronto-why-theyre-gaining-traction-amid-2026-rate-stability/

[2] Watch – https://www.youtube.com/watch?v=aJwBbua9_XQ

[5] Mortgage Interest Rate Forecast – https://www.mortgagesandbox.com/mortgage-interest-rate-forecast

[7] Gta Mortgage Trends Variable Rates Gain Traction In 2026 – https://www.realestategtatoday.ca/index.php/2026/03/02/gta-mortgage-trends-variable-rates-gain-traction-in-2026/

[8] Bank Canada Holds Rate 225 Amid Global Tensions And Economic Certainty – https://rates.ca/resources/bank-canada-holds-rate-225-amid-global-tensions-and-economic-certainty

[10] Variable Rate Mortgages Regain Popularity As Morningstar Flags Rising Risks – https://www.canadianmortgagetrends.com/2026/02/variable-rate-mortgages-regain-popularity-as-morningstar-flags-rising-risks/