March 20, 2026

Private Mortgages for Toronto’s Renewal Shock Borrowers: Avoiding the 26% Payment Hit Without Selling Your Home

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Imagine opening a mortgage renewal letter and seeing your monthly payment jump by $500 or more — overnight. For thousands of Toronto homeowners in 2026, that scenario is not a nightmare. It is reality. Private Mortgages for Toronto’s Renewal Shock Borrowers: Avoiding the 26% Payment Hit Without Selling Your Home is not just a concept — it is an urgent financial strategy that is keeping families in their homes while the renewal wave crashes hardest across the GTA.

Key Takeaways 📌

- Toronto’s mortgage arrears rate quadrupled from post-pandemic lows by early 2026, with nearly 2,800 families 90+ days delinquent [10]

- Homeowners on $700,000 mortgages face $450–$680/month payment hikes at renewal — a roughly 26% increase [7]

- Private Mortgages offer a 6–36 month bridge for equity-rich borrowers who cannot qualify through traditional channels

- Private lenders focus on loan-to-value (LTV) up to 75–80%, not just credit score or income

- Starting the renewal process 120–180 days early dramatically expands your options and reduces panic decisions [3]

Understanding Toronto’s 2026 Renewal Shock

The numbers are stark. TD Economics’ “Final Reckoning” report confirms that while 25% of Canadian mortgage holders are actually seeing payment drops at renewal, Toronto and Vancouver borrowers face a very different reality [7]. Those renewing $700,000 mortgages are absorbing $450–$680 in extra monthly costs — that is the 26% payment hit that is pushing families to the financial edge.

The Bank of Canada held its overnight rate at 2.25% into early 2026 after a series of cuts, yet one-third of renewers still face payment increases [1]. For the 10% of variable-rate holders, the shock is even worse — some are seeing 40%+ jumps in monthly obligations [1].

💬 “The worst renewal shock may have passed nationally, but for Toronto homeowners, the peak pain is happening right now.” — TD Economics, March 2026 [7]

CMHC data shows Toronto’s mortgage arrears rate quadrupled from post-pandemic lows by February 2026, with a reported 450% surge in delinquencies concentrated in the GTA [3][10]. Nearly 2,800 families were 90+ days behind — and that number was rising ahead of the June renewal peak [3].

For homeowners who understand what happens when a mortgage renewal is denied, the stakes could not be higher. Power-of-sale proceedings can begin quickly once arrears accumulate, making early action critical.

What Are Private Mortgages — and Why Are They Surging in 2026?

A private mortgage is a loan secured against your home from a non-bank lender — typically a private individual, syndicate, or mortgage investment corporation (MIC). Unlike banks or credit unions, private lenders do not use the same rigid qualification criteria.

Private lenders primarily care about:

- 🏠 The value of your property (equity)

- 📊 Your loan-to-value ratio (typically capped at 75–80%)

- 📍 The location and marketability of the home

They care less about:

- Credit score dips from missed payments

- Inconsistent employment income

- Recent arrears history

This makes private mortgages a powerful tool for equity-rich but cash-flow-stressed Toronto homeowners — exactly the profile of many 2026 renewal shock borrowers.

For a complete breakdown of how this works, see this full guide to getting a mortgage with a private lender.

How Easy Is It to Actually Get One?

Approval timelines are dramatically shorter than traditional channels. Private mortgage approvals typically take 5–10 business days, compared to weeks for bank refinancing [3][6]. For borrowers racing against a renewal deadline or arrears clock, this speed matters enormously.

Mortgage expert Marcus Chen of CollectorHQ recommends private mortgages specifically as 6–36 month bridge solutions for equity-rich Toronto borrowers, emphasizing that the focus on LTV over credit or income makes them uniquely suited to the current crisis [3][6]. Learn more about how easy it is to get a private mortgage and what lenders look for.

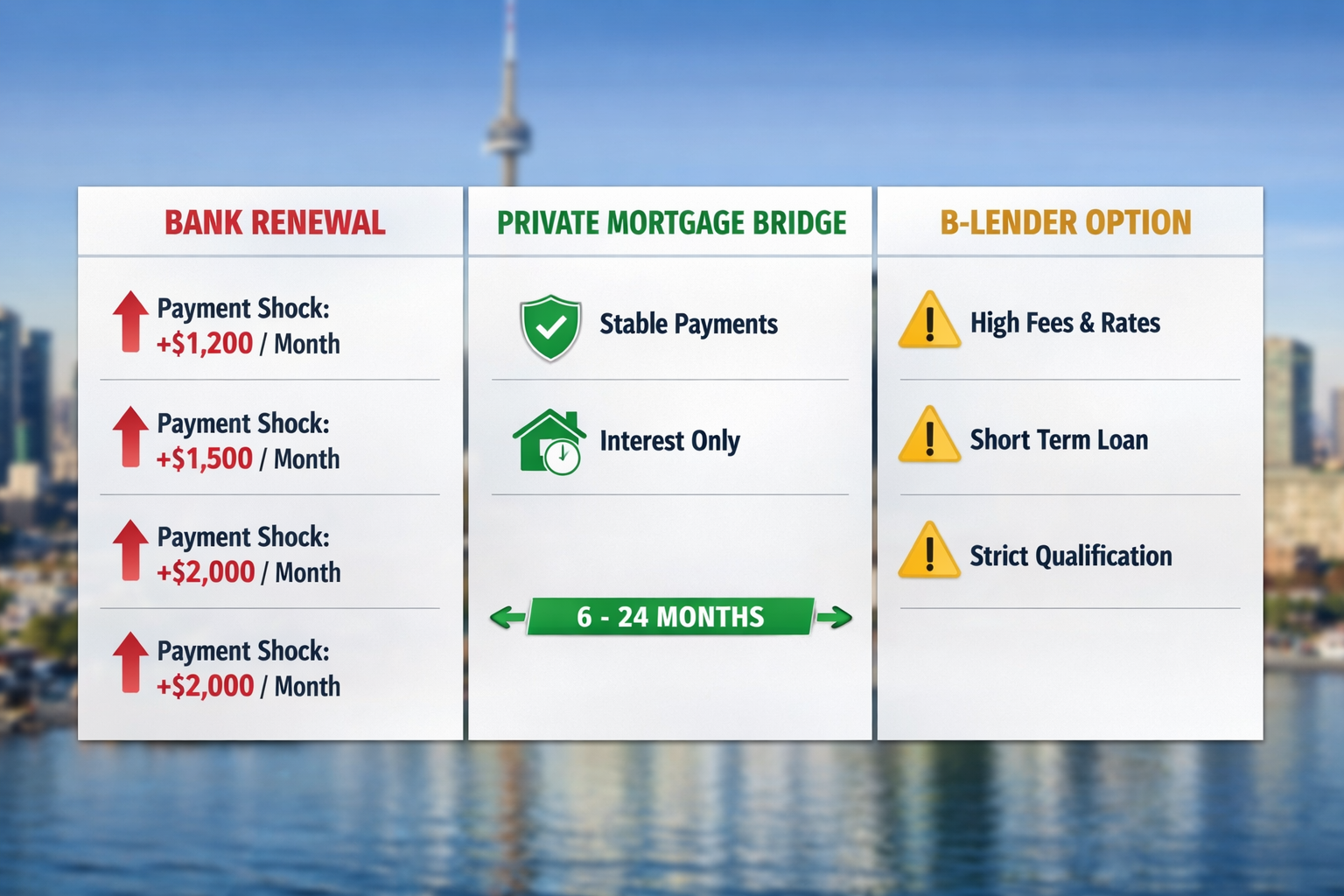

Comparing Your Options: Private Mortgages vs. Alternatives

Before committing to any path, renewal shock borrowers should understand the full landscape. Here is a clear comparison:

| Option | Rate Range | Approval Speed | Best For |

|---|---|---|---|

| Bank Renewal (standard) | 3.35–5.5% | 2–4 weeks | Strong credit, stable income |

| B-Lender / Alt-A | 7–9% | 1–2 weeks | Minor credit issues, pre-90 days arrears |

| Private Mortgage | 8–12% | 5–10 days | Equity-rich, post-arrears, urgent need |

| HELOC | 6–8% | 2–3 weeks | Existing equity, good credit |

| Amortization Extension | Bank rate | 1–2 weeks | Cash flow relief, long-term cost trade-off |

Option 1: Amortization Extension ⏳

The Bank of Canada’s own data suggests that half of borrowers facing payment increases could eliminate the payment jump entirely by extending their amortization by five years [1][7]. However, this comes at a steep long-term cost — tens of thousands of dollars in extra interest over the life of the mortgage.

Worse, bank portfolios already show 13–30% of mortgages extended beyond 35 years by 2024 [1]. Borrowers who stretched during the pandemic rate spike are now paying the price in compounding interest costs.

Option 2: B-Lenders and HELOCs 🏦

For borrowers with better credit profiles and fewer than 90 days in arrears, B-Lenders and HELOC products offer rates in the 7–9% range — preferable to private mortgage rates of 8–12% [3][6]. However, once a borrower crosses the 90-day arrears threshold, B-lender options narrow significantly.

Option 3: Lender Switch or Refinance 🔄

Shopping lenders 120 days before renewal can unlock 5-year variable rates around 3.35% [1]. This is the best outcome for borrowers who act early and qualify. The 2026 mortgage renewal guide for Toronto first-time buyers covers this path in detail.

The counterargument: banks offering quiet amortization extensions to 35+ years may trap borrowers in long-term interest traps. Private mortgages, despite higher short-term rates, can preserve equity and avoid power-of-sale losses [1][3].

Option 4: Forbearance or Sale 🏷️

The Financial Consumer Agency of Canada (FCAC) recommends exploring forbearance first. However, selling incurs real estate commissions, land transfer taxes, and capital gains exposure. For most Toronto homeowners, a 12–24 month private mortgage bridge preserves far more equity than a forced sale — even accounting for the higher interest rate [6].

How Private Mortgages for Toronto’s Renewal Shock Borrowers Actually Work in Practice

Here is a practical walkthrough of how a renewal shock borrower might use a private mortgage strategically:

Step 1: Assess Your Equity Position Calculate your current LTV. If your Toronto home is worth $900,000 and you owe $630,000, your LTV is 70% — well within the 75–80% threshold most private lenders accept.

Step 2: Start 120–180 Days Early Mortgage experts unanimously urge starting the renewal conversation 4–6 months before your renewal date [3][6]. This window keeps B-lender and even bank options open, and gives time to arrange private financing without panic.

Step 3: Work With a Mortgage Broker A licensed broker has access to dozens of private lenders and can match your specific equity profile to the right product. Understand what a mortgage broker does and how they can negotiate on your behalf — often at no direct cost to you.

Step 4: Use the Bridge Period Wisely The private mortgage term (typically 1–2 years) is not the destination — it is the bridge. During this period, borrowers should:

- ✅ Rebuild credit scores

- ✅ Reduce other debt obligations

- ✅ Document income more thoroughly (especially self-employed borrowers)

- ✅ Wait for potential further rate environment improvements

Step 5: Exit to Conventional Financing After 12–24 months of on-time private mortgage payments, most borrowers can qualify for B-lender or even bank rates again. The private mortgage has done its job.

💡 Key Insight: Lendworth Financial views private mortgages in 2026 as a proactive strategy, not a last resort. The delinquency spike makes early intervention — before arrears accumulate — the smartest financial move available to equity-rich Toronto homeowners.

Common Mistakes to Avoid ⚠️

Avoid these critical errors when navigating renewal shock:

- Waiting until arrears hit 90+ days — this closes B-lender doors permanently [3]

- Accepting the first renewal offer from your existing bank without shopping alternatives

- Ignoring the stress test implications — even private mortgage exits require qualifying; review how the mortgage stress test works before planning your exit strategy

- Underestimating private mortgage costs — factor in lender fees (1–3%), broker fees, and legal costs when calculating total bridge cost

- Failing to have a clear exit plan — private mortgages without a defined path back to conventional financing can trap borrowers in high-rate cycles

For a broader look at pitfalls, review common mistakes to avoid when applying for a mortgage in Canada.

Conclusion: Keep Your Home, Bridge the Gap, Rebuild Your Position

The 2026 renewal wave is real, and for Toronto homeowners facing a 26% payment jump, the pressure to sell can feel overwhelming. But selling is not the only option — and for most equity-rich borrowers, it is not the best option.

Private Mortgages for Toronto’s Renewal Shock Borrowers: Avoiding the 26% Payment Hit Without Selling Your Home represents a legitimate, strategic path through the crisis. By leveraging home equity, working with experienced brokers, and using a private mortgage as a deliberate 12–24 month bridge, homeowners can protect their most valuable asset while rebuilding the financial profile needed to return to conventional rates.

✅ Your Actionable Next Steps:

- Calculate your LTV today — if it is under 75–80%, you likely qualify for private financing

- Contact a licensed mortgage broker at least 120 days before your renewal date

- Request a full options comparison — bank, B-lender, and private side-by-side

- Create a 12–24 month financial improvement plan to maximize your exit from private financing

- Do not wait for arrears — act while all doors are still open

The Toronto housing market rewards those who stay in it. A well-structured private mortgage bridge could be the difference between keeping your home and losing it — and in 2026, that difference matters more than ever.

References

[1] Watch – https://www.youtube.com/watch?v=lSQJu2PTr7M [3] Private Mortgages For Toronto Homeowners Battling 450 Delinquency Surge Survival Tactics In March 2026 – https://everythingmortgages.ca/blog/private-mortgages-for-toronto-homeowners-battling-450-delinquency-surge-survival-tactics-in-march-2026/ [6] Private Mortgages For Torontos 450 Delinquency Surge Early Intervention Strategies In Q2 2026 – https://everythingmortgages.ca/blog/private-mortgages-for-torontos-450-delinquency-surge-early-intervention-strategies-in-q2-2026/ [7] Ca Mortgage Renewals March 2026 – https://economics.td.com/domains/economics.td.com/documents/reports/ms/CA_Mortgage_Renewals_March-2026.pdf [10] Mortgage Renewal Wave Strains Some Regions Borrowers – https://www.cmhc-schl.gc.ca/observer/2026/mortgage-renewal-wave-strains-some-regions-borrowers