February 8, 2026

2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Imagine standing at the threshold of homeownership in 2026, watching mortgage rates fluctuate while wondering if you’ll ever catch the perfect moment to lock in your dream home. For self-employed Canadians, this challenge becomes even more complex. The 2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers reveals a landscape of cautious optimism, where expert predictions from major financial institutions suggest rates will stabilize between 5.9% and 6.3% throughout the year[1][2]. But understanding these forecasts is only half the battle—self-employed borrowers must navigate unique documentation requirements and lender scrutiny that traditional employees rarely face.

As we move through 2026, the mortgage market presents both opportunities and obstacles. Current data shows the 30-year fixed rate at 6.23% as of early February 2026, down from 7.02% one year prior[1]. This represents significant progress, yet the journey toward optimal rates requires strategic planning, especially for entrepreneurs, freelancers, and business owners whose income streams don’t fit the traditional mold.

Key Takeaways

✅ Expert consensus predicts mortgage rates will stabilize between 5.9% and 6.3% throughout 2026, with Fannie Mae forecasting rates at 6% for most of the year and ending at 5.9%[1][2]

✅ Self-employed borrowers face stricter documentation requirements but can secure competitive rates by preparing comprehensive financial records and working with specialized mortgage brokers

✅ The Federal Reserve’s monetary policy will play a crucial role in rate movements, with potential rate cuts expected in mid-to-late 2026 if inflation remains on target[1][2]

✅ Timing your mortgage application strategically during periods of rate stabilization can save thousands over the life of your loan

✅ Alternative documentation programs and specialized lenders offer viable pathways for self-employed Canadians who may not qualify through traditional channels

Understanding the 2026 Mortgage Rate Forecast: What Experts Are Predicting

The 2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers begins with understanding what major financial institutions expect for the year ahead. Multiple authoritative sources have weighed in with remarkably consistent predictions.

Major Institutional Forecasts

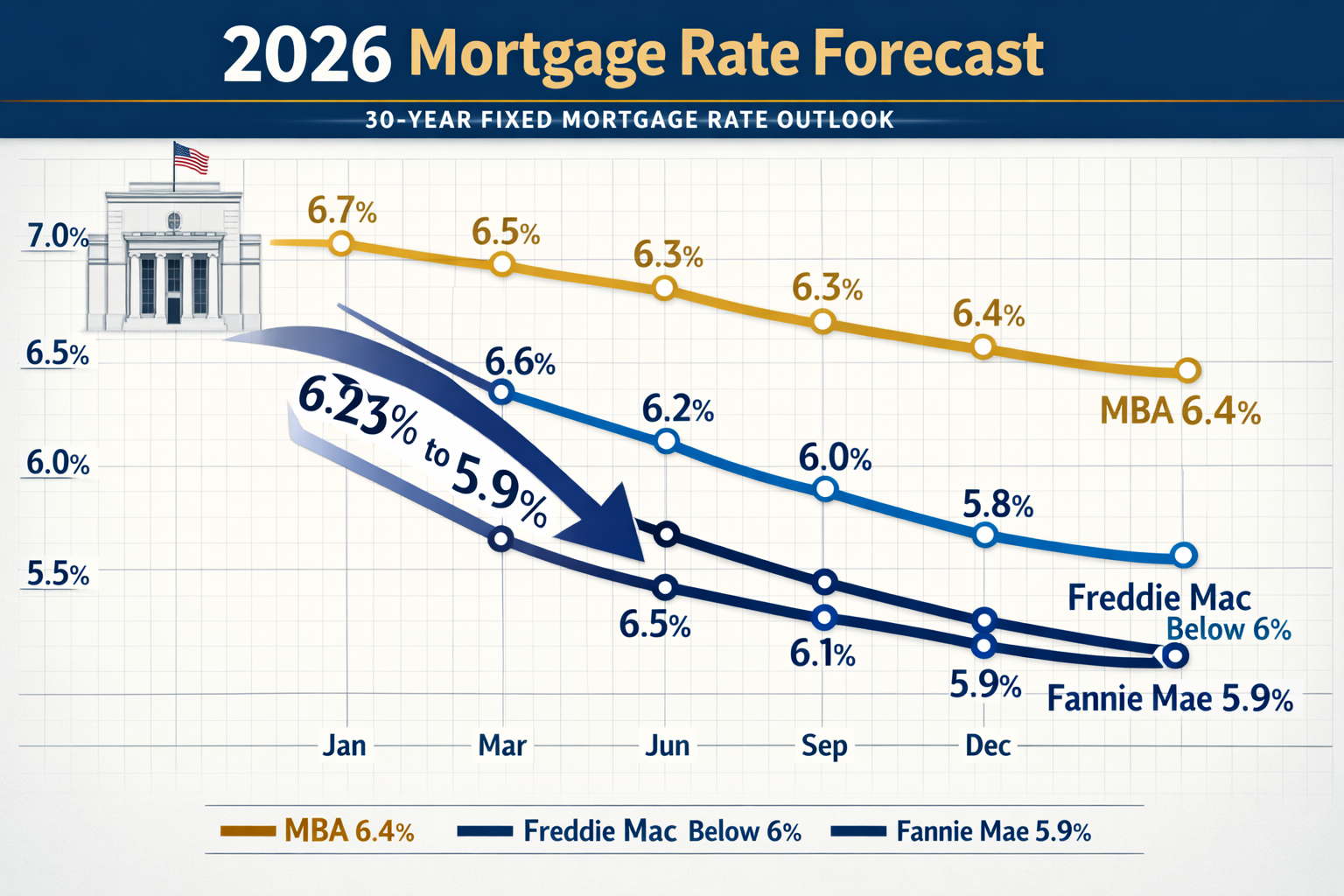

Fannie Mae’s January 2026 Housing Forecast projects that rates will sit at approximately 6% for most of 2026 and 2027, with specific forecasts showing rates ending 2026 at 5.9%[1][2][5]. This represents a gradual but steady decline from current levels.

Freddie Mac takes a slightly more optimistic stance, projecting that average 30-year fixed rates will settle below 6% in 2026[2]. Their analysis considers ongoing economic stabilization and anticipated Federal Reserve policy adjustments.

The Mortgage Bankers Association (MBA) predicts rates could fall to around 6.4% by late 2026, contingent on inflation remaining on target[2]. This forecast acknowledges the delicate balance between economic growth and price stability.

The National Association of Realtors (NAR) forecasts that mortgage rates will stabilize near 6%[2], aligning closely with other major predictions and suggesting a strong industry consensus.

Current Rate Snapshot 📊

As of early February 2026, here’s where rates stand:

| Mortgage Type | Current Rate | One Year Ago | Change |

|---|---|---|---|

| 30-Year Fixed | 6.23% | 7.02% | -0.79% |

| 15-Year Fixed | 5.61% | 6.21% | -0.60% |

| 30-Year Jumbo | 6.38% | N/A | N/A |

The 52-week low of 6.18% was achieved three weeks prior to early February[1], demonstrating that rates have already approached the lower end of expert predictions. Understanding these trends helps self-employed mortgage applicants time their applications strategically.

Economic Factors Driving the Forecast

Several key economic indicators influence the 2026 mortgage rate outlook:

Federal Reserve Policy: The Federal Reserve held its benchmark interest rate steady as of late January 2026 and is expected to consider rate cuts in mid-to-late 2026 if current economic trends continue[1][2]. These decisions directly impact mortgage rates, as lenders adjust their offerings based on the broader interest rate environment.

Government Intervention: In early January 2026, the Trump administration directed Fannie Mae and Freddie Mac to purchase $200 billion in mortgage-backed securities, which temporarily lowered rates to 6.18%[1]. However, this decline has not sustained, and academic analysis suggests such policies create only “temporary and limited reduction in mortgage rates” without coordinated Federal Reserve or Congressional support[1].

Inflation Trends: The path of inflation remains critical. If inflation continues its downward trajectory, the Federal Reserve will have more flexibility to implement rate cuts, which would support lower mortgage rates throughout the year.

“Most forecasts suggest rates will gradually decline in 2026, with averages possibly landing between 5.5% and 6%”[2]

For self-employed borrowers, understanding these macroeconomic factors provides context for planning major financial decisions. Those considering mortgage renewals should pay particular attention to these trends.

Unique Challenges Self-Employed Borrowers Face in 2026

While the 2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers shows promising rate trends, self-employed Canadians encounter distinct obstacles that traditional employees rarely face. Understanding these challenges is the first step toward overcoming them.

Income Verification Complexities

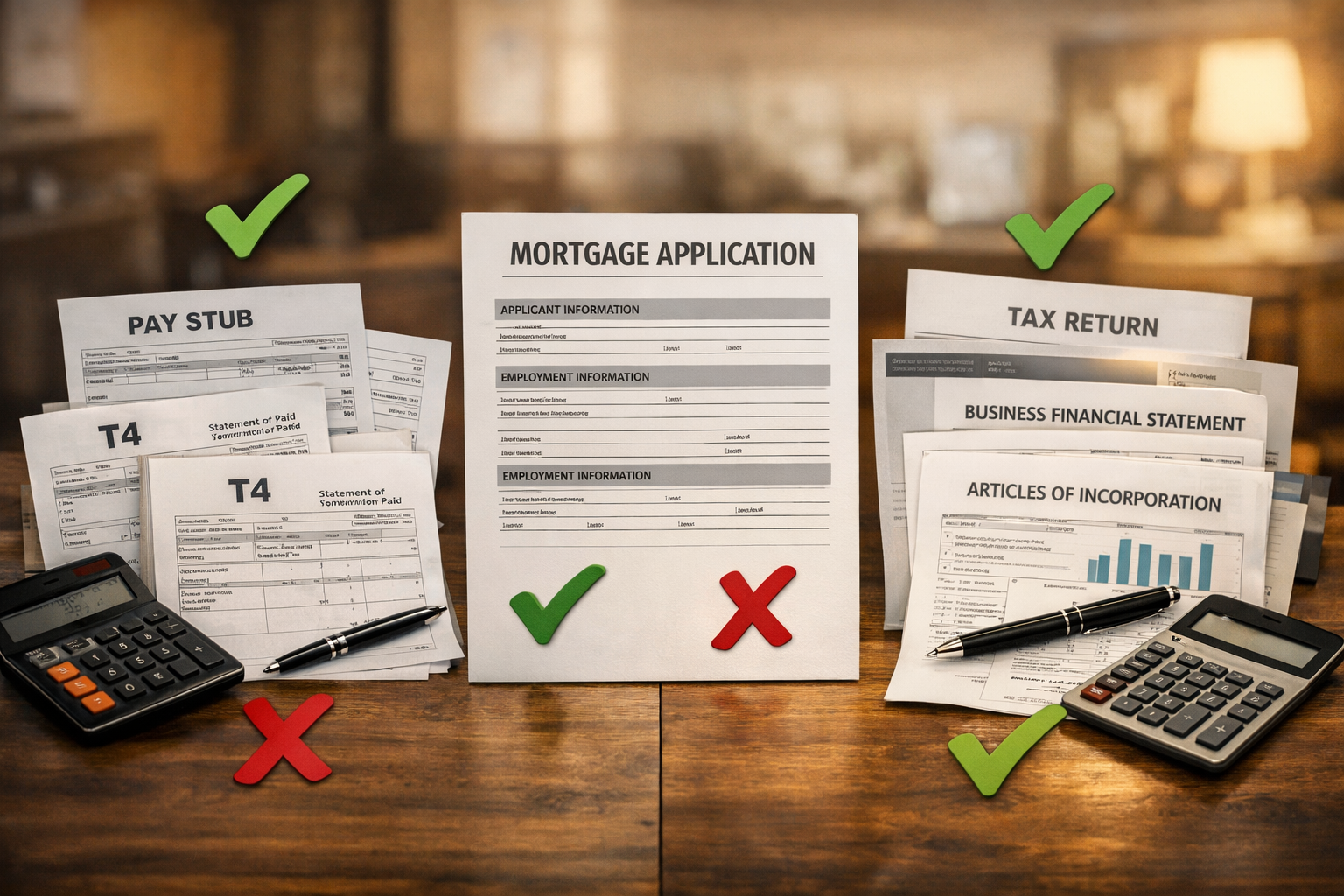

Traditional employment verification typically involves providing recent pay stubs and a letter from an employer. Self-employed borrowers must navigate a more complex process:

Tax Return Requirements: Most lenders require two years of complete tax returns, including all schedules and supporting documentation. This creates challenges for:

- Recently self-employed individuals (less than two years)

- Business owners who maximize deductions (reducing taxable income)

- Entrepreneurs experiencing year-over-year income fluctuations

Business Financial Statements: Lenders often request:

- Profit and loss statements

- Balance sheets

- Business bank statements (6-12 months)

- Accounts receivable aging reports

- Client contracts demonstrating ongoing income

The fundamental issue is that self-employed individuals often show lower taxable income due to legitimate business deductions, which can reduce their qualifying income for mortgage purposes. Learning about common mistakes self-employed homebuyers make can help avoid these pitfalls.

Documentation Requirements 📋

Self-employed borrowers should prepare to provide:

Essential Documents:

- ✅ Two years of personal tax returns (T1 Generals)

- ✅ Two years of business tax returns (T2 for corporations, T2125 for sole proprietors)

- ✅ Notice of Assessments from CRA

- ✅ Business license and registration

- ✅ Articles of incorporation (if applicable)

- ✅ Year-to-date profit and loss statement

- ✅ Business bank statements (6-12 months)

- ✅ Personal bank statements (3-6 months)

- ✅ Letter from accountant confirming income stability

Additional Documentation may include:

- Client contracts or purchase orders

- Proof of business continuity (website, business cards, marketing materials)

- Professional license or certification

- Business credit report

Higher Scrutiny and Stress Testing

Lenders apply additional scrutiny to self-employed applications because of perceived higher risk. This includes:

Income Averaging: Rather than using current income, lenders typically average income over two years, which can disadvantage growing businesses.

Add-Back Analysis: Some lenders perform “add-back” calculations, restoring certain business expenses (like depreciation) to qualifying income. However, not all lenders offer this benefit.

Debt Service Coverage: Business owners may face additional requirements to demonstrate their business generates sufficient cash flow beyond their personal draw.

Stress Testing: All borrowers must qualify at rates higher than their actual mortgage rate, but self-employed applicants often face additional verification to ensure income stability.

Industry-Specific Considerations

Certain professions face unique challenges:

Freelancers and Gig Workers: Those with multiple income streams must document each source comprehensively. Our guide to freelancer mortgages provides specialized strategies.

Medical Professionals: Doctors and healthcare practitioners have specialized mortgage programs available. Learn more about self-employed mortgages for doctors.

Business Owners: Those operating incorporated businesses face different documentation requirements than sole proprietors. Understanding how to get a mortgage as a business owner in Canada is essential.

Down Payment Expectations

While not always required, self-employed borrowers often benefit from larger down payments:

- 5-10% down: Possible but may require mortgage insurance and stronger documentation

- 15-20% down: Improves approval odds and may access better rates

- 25%+ down: Significantly strengthens application and may unlock alternative programs

The reality is that self-employed borrowers must be more prepared, more organized, and more strategic than their traditionally employed counterparts. However, with proper preparation, competitive rates are absolutely achievable.

Strategic Approaches to Securing the Best Rates as a Self-Employed Borrower

Understanding the challenges is only the beginning. The 2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers requires actionable strategies that position self-employed Canadians for success in today’s mortgage market.

Optimize Your Financial Profile

Clean Up Your Tax Strategy: While minimizing taxes is smart business, it can hurt mortgage applications. Consider these approaches:

Two-Year Planning Window: If homeownership is on your horizon, adjust your tax strategy 24 months in advance. This might mean:

- Taking fewer discretionary deductions

- Showing higher net income on tax returns

- Documenting income more conservatively

- Maintaining consistent year-over-year income

Work with a Mortgage-Savvy Accountant: Not all accountants understand mortgage qualification. Find one who can balance tax efficiency with mortgage qualification needs.

Separate Personal and Business Finances: Maintain distinct bank accounts, credit cards, and financial records. This clarity helps lenders assess your personal financial stability.

Build a Comprehensive Documentation Package

Create a Mortgage Application Binder that includes:

- Income Documentation (organized chronologically)

- Business Verification (licenses, registrations, contracts)

- Credit Information (reports, explanations for any issues)

- Asset Verification (bank statements, investment accounts)

- Debt Documentation (current obligations, payment history)

Prepare a Business Overview that tells your story:

- Nature of business and industry

- Years in operation

- Client diversity and contract stability

- Growth trajectory and future outlook

- Competitive advantages

This narrative helps lenders understand your business beyond the numbers and can be particularly valuable when working with specialized mortgage brokers.

Leverage Alternative Documentation Programs

Stated Income Programs: Some lenders offer programs where business owners can state their income with less traditional documentation, though these typically require:

- Larger down payments (25-35%)

- Higher interest rates (0.5-1.5% premium)

- Strong credit scores (680+)

- Established business history (3+ years)

Bank Statement Programs: These programs analyze business and personal bank deposits to verify income, requiring:

- 12-24 months of bank statements

- Consistent deposit patterns

- Verification that deposits represent income (not loans or transfers)

Portfolio Lending: Some lenders keep loans on their own books rather than selling them, allowing more flexibility in underwriting. These programs may consider:

- Overall net worth

- Liquid assets

- Investment portfolios

- Business equity

Understanding what you need to know about self-employed mortgages helps identify which programs suit your situation.

Timing Your Application Strategically

Monitor Rate Trends: Based on 2026 forecasts showing rates stabilizing between 5.9% and 6.3%[1][2], consider these timing strategies:

Early-to-Mid 2026: Current rates around 6.23% may represent good value if you need to purchase immediately. Waiting for the forecasted decline to 5.9% by year-end means potentially missing out on home appreciation.

Rate Lock Strategies: Once you find favorable rates, consider:

- 60-90 day rate locks: Protect against increases during the application process

- Float-down options: Some lenders allow you to capture lower rates if they drop before closing

- Rate holds: In Canada, rate holds typically last 90-120 days at no cost

Seasonal Considerations: Mortgage rates can fluctuate based on seasonal demand:

- Spring/Summer: Higher competition may mean less favorable terms

- Fall/Winter: Slower markets might offer better negotiating leverage

Work with Specialized Mortgage Professionals

Choose a Broker Experienced with Self-Employed Clients: Not all mortgage brokers understand the nuances of self-employed applications. Look for professionals who:

- Specialize in self-employed mortgages

- Have relationships with multiple lenders (including alternative lenders)

- Can explain different program options clearly

- Provide proactive communication throughout the process

- Have proven success with clients in your industry

Benefits of Broker Relationships:

- Access to multiple lenders and programs

- Expert guidance on documentation requirements

- Ability to match your profile with the right lender

- Negotiating leverage for rates and terms

- Support through the entire process

Improve Your Credit Profile

Credit Score Targets for self-employed borrowers:

| Credit Score | Typical Impact |

|---|---|

| 680-699 | Minimum for most programs; limited options |

| 700-739 | Good options; competitive rates available |

| 740-799 | Excellent options; best rates accessible |

| 800+ | Premium treatment; maximum negotiating power |

Credit Improvement Strategies:

- Pay all bills on time (35% of score)

- Reduce credit utilization below 30% (30% of score)

- Maintain older credit accounts (15% of score)

- Limit new credit applications (10% of score)

- Monitor credit reports for errors

Consider Alternative Financing Options

If traditional financing proves challenging, explore:

Private Lenders: These lenders focus more on property equity than income verification. While rates are higher (typically 7-12%), they can provide:

- Bridge financing until you qualify traditionally

- Purchase opportunities you might otherwise miss

- Flexibility for unique situations

Learn more about private mortgage rates in Ontario.

Co-Signers or Co-Borrowers: Adding someone with traditional employment can:

- Strengthen your application

- Improve qualifying income

- Access better rates and terms

Larger Down Payments: Increasing your down payment to 25-35% can:

- Reduce lender risk perception

- Eliminate mortgage insurance requirements

- Open alternative program options

- Potentially secure better rates

Pre-Approval Strategy

Get Pre-Approved Early: Pre-approval provides:

- Clear understanding of your buying power

- Competitive advantage in multiple-offer situations

- Time to address any documentation issues

- Rate protection during your home search

Maintain Pre-Approval Status:

- Avoid major purchases or new debt

- Don’t change jobs or business structure

- Keep finances stable and documented

- Communicate any changes to your broker immediately

By implementing these strategic approaches, self-employed borrowers can position themselves to secure the best possible rates in 2026’s stabilizing market. The key is preparation, documentation, and working with professionals who understand the unique landscape of self-employed mortgage financing.

Navigating Rate Locks and Mortgage Products in 2026

As the 2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers suggests rates stabilizing between 5.9% and 6.3%, understanding different mortgage products and rate lock strategies becomes crucial for maximizing your financial advantage.

Fixed vs. Variable Rate Considerations

Fixed-Rate Mortgages offer predictability and protection:

Advantages for Self-Employed Borrowers:

- Predictable monthly payments support business cash flow planning

- Protection against rate increases if forecasts prove conservative

- Simplified budgeting for variable income situations

- Peace of mind during business expansion or transition periods

Current Environment: With rates expected to stabilize rather than dramatically decline[1][2], fixed rates around 6% represent reasonable value for those prioritizing certainty.

Variable-Rate Mortgages offer potential savings:

Advantages:

- Lower starting rates (typically 0.5-1% below fixed)

- Benefit from rate decreases if Federal Reserve cuts materialize

- Flexibility to convert to fixed rates later

- Potential long-term savings if rates decline as forecasted

Risks:

- Payment uncertainty can complicate business budgeting

- Potential increases if economic conditions change

- Stress for those with variable business income

For a comprehensive comparison, review our guide on fixed vs. variable mortgages.

Rate Lock Strategies

Understanding Rate Holds: In Canada, rate holds typically last 90-120 days and protect you from rate increases while you shop for a home.

Optimal Rate Lock Timing:

Scenario 1 – Active Home Search: Lock rates once you’re seriously shopping and expect to purchase within 90 days.

Scenario 2 – Specific Property Identified: Lock immediately upon making an offer to protect against increases during the purchase process.

Scenario 3 – Market Volatility: If rates are particularly favorable or market conditions suggest increases, lock earlier rather than later.

Rate Lock Features to Negotiate:

- Lock period: 90-120 days standard; longer periods may be available

- Float-down provisions: Ability to capture lower rates if they drop

- Extension options: What happens if your closing is delayed

- Cancellation terms: Flexibility if circumstances change

Mortgage Terms and Amortization

Term Length Options:

1-2 Year Terms:

- ✅ Flexibility to refinance when rates potentially drop further

- ✅ Lower penalties if you need to break the mortgage

- ❌ Higher rates than longer terms

- ❌ Renewal risk if rates increase

3-5 Year Terms (Most Popular):

- ✅ Balance of rate security and flexibility

- ✅ Competitive rates

- ✅ Reasonable commitment period

- ❌ Moderate penalties for early termination

7-10 Year Terms:

- ✅ Maximum rate security

- ✅ Long-term payment predictability

- ❌ Higher rates than shorter terms

- ❌ Significant penalties for early termination

Amortization Considerations:

Self-employed borrowers should carefully consider amortization periods:

25-Year Amortization (Standard):

- Balanced monthly payments

- Reasonable interest costs

- Flexibility for business cash flow

30-Year Amortization:

- Lower monthly payments

- More cash available for business investment

- Higher total interest costs

- May require larger down payment

Learn about 30-year amortization options for eligible buyers.

Shorter Amortization (15-20 Years):

- Significantly lower total interest

- Builds equity faster

- Higher monthly payments (challenging for variable income)

Mortgage Features to Prioritize

Prepayment Privileges: Essential for self-employed borrowers with variable income:

Annual Lump-Sum Payments: Ability to make extra payments (typically 10-20% of original principal) when business has strong years.

Payment Increase Options: Ability to increase regular payments (typically 10-20% annually) to pay down principal faster.

Portability: Transfer your mortgage to a new property without penalty—valuable if business relocation becomes necessary.

Assumability: Allow a buyer to take over your mortgage—can be a selling feature if rates increase.

Flexibility for Business Owners:

- Refinancing options: Access equity for business expansion

- Home equity lines of credit: Backup funding for business needs

- Skip-a-payment features: Safety net during slow business periods

Specialized Programs for Self-Employed Borrowers

Professional Programs: Doctors, lawyers, and other licensed professionals may qualify for:

- Reduced documentation requirements

- Higher debt-service ratios

- Preferential rates

- Larger loan amounts

New-to-Canada Programs: Self-employed immigrants may access:

- Alternative income verification

- Foreign income consideration

- Reduced credit history requirements

Business-for-Self (BFS) Programs: Designed specifically for self-employed borrowers:

- Streamlined documentation

- Income verification through business records

- Competitive rates for qualified applicants

Negotiating Your Best Rate

Factors That Strengthen Negotiating Position:

💪 Strong Credit Score (740+): Demonstrates financial responsibility

💪 Substantial Down Payment (25%+): Reduces lender risk

💪 Established Business (3+ years): Proves income stability

💪 Low Debt-to-Income Ratio: Shows capacity to handle payments

💪 Multiple Income Sources: Diversification reduces risk

💪 Significant Assets: Demonstrates overall financial strength

Negotiation Strategies:

- Shop Multiple Lenders: Get quotes from at least 3-5 lenders

- Use Competing Offers: Leverage one lender’s offer against another

- Bundle Products: Some lenders offer better rates when you bring other business

- Timing Leverage: End-of-month or end-of-quarter may offer better deals

- Professional Representation: Brokers can often negotiate better than individuals

Monitoring Rate Trends Throughout 2026

Key Indicators to Watch:

📊 Federal Reserve Announcements: Rate decisions directly impact mortgage rates

📊 Inflation Reports: CPI data influences Federal Reserve policy

📊 Employment Numbers: Strong employment supports economic growth and rate stability

📊 Housing Market Data: Supply and demand dynamics affect lending conditions

📊 Bond Yields: Government bond rates correlate closely with mortgage rates

Staying Informed:

- Subscribe to mortgage rate newsletters

- Follow reputable financial news sources

- Maintain regular contact with your mortgage broker

- Review rate comparison websites weekly during active shopping

Understanding these mortgage products and strategies positions self-employed borrowers to make informed decisions aligned with both their homeownership goals and business realities.

Conclusion: Your Action Plan for Securing Optimal Rates in 2026

The 2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers presents a landscape of cautious optimism. With expert predictions from Fannie Mae, Freddie Mac, and the Mortgage Bankers Association converging around rates of 5.9% to 6.3%[1][2], self-employed Canadians have a clearer picture of what to expect throughout the year.

Current rates of 6.23% for 30-year fixed mortgages represent significant improvement from the 7.02% seen one year ago[1], and the trajectory suggests continued gradual decline. However, securing these favorable rates as a self-employed borrower requires strategic preparation and execution.

Your 90-Day Action Plan 🎯

Days 1-30: Financial Preparation

- Gather two years of tax returns and business financial statements

- Review credit reports and address any issues

- Consult with a mortgage-savvy accountant about income optimization

- Calculate realistic budget including stress-tested rates

- Begin building your comprehensive documentation package

Days 31-60: Professional Engagement

- Research and interview specialized mortgage brokers

- Get pre-approved to understand your buying power

- Compare multiple lender options and programs

- Identify the best mortgage product for your situation

- Establish rate monitoring system

Days 61-90: Strategic Execution

- Lock in favorable rates when identified

- Finalize documentation and application

- Maintain financial stability (no major purchases or changes)

- Stay informed on market conditions

- Prepare for closing process

Key Success Factors

Documentation Excellence: The difference between approval and denial often comes down to documentation quality. Invest time in creating a comprehensive, organized package that tells your financial story clearly.

Professional Guidance: Working with mortgage professionals who specialize in self-employed borrowers dramatically improves your odds of securing optimal rates and terms.

Strategic Timing: While rates are expected to stabilize around 6%, waiting for the “perfect” rate can mean missing out on the right property or favorable market conditions.

Financial Optimization: Balance tax efficiency with mortgage qualification by planning 24 months ahead and working with professionals who understand both objectives.

Flexibility and Options: Explore multiple programs, lenders, and strategies. The right solution for your situation may not be the most obvious path.

Looking Ahead

The consensus among major forecasters suggests 2026 will be a year of stabilization rather than dramatic rate movements[1][2][5]. This creates a favorable environment for well-prepared self-employed borrowers to secure competitive financing without the pressure of rapidly changing conditions.

Whether you’re a first-time buyer, looking to upgrade, or considering refinancing, the strategies outlined in this guide provide a roadmap for success. Remember that while self-employed borrowers face additional scrutiny, thousands successfully secure mortgages every year by following proven preparation and application strategies.

The 2026 Mortgage Rate Forecast: Securing the Best Rates for Self-Employed Borrowers isn’t just about understanding numbers—it’s about positioning yourself strategically to capitalize on favorable market conditions while navigating the unique challenges of self-employment.

Take Action Today

Don’t wait for perfect conditions that may never materialize. Start your preparation now:

- Download your credit reports and review them carefully

- Organize your financial documentation into a comprehensive package

- Connect with a specialized mortgage broker who understands self-employed financing

- Calculate your realistic budget using stress-tested rates

- Monitor rate trends while maintaining focus on overall value

The opportunity to secure favorable mortgage rates in 2026 is real, but it requires proactive preparation and strategic execution. By implementing the strategies outlined in this guide, self-employed borrowers can confidently navigate the mortgage market and secure the financing needed to achieve their homeownership goals.

Your journey to homeownership as a self-employed Canadian may have unique challenges, but with proper preparation, professional guidance, and strategic timing, securing competitive rates in 2026 is absolutely achievable. Start your preparation today, and position yourself for success in the year ahead.

References

[1] Mortgage Rates February 4 2026 – https://www.bankrate.com/mortgages/analysis/mortgage-rates-february-4-2026/

[2] Will Mortgage Rates Drop Further In 2026 What Experts Predict – https://www.midflorida.com/resources/insights-and-blogs/insights/mortgage/will-mortgage-rates-drop-further-in-2026-what-experts-predict

[3] Display – https://www.fanniemae.com/media/56586/display

[4] 2026 Mortgage Rate Forecast – https://www.acrisure.com/blog/2026-mortgage-rate-forecast

[5] Mortgage Rates Forecast For 2026 Experts Predict Whether Rates Will Keep Dropping – https://www.firstcbt.bank/blog/post/mortgage-rates-forecast-for-2026-experts-predict-whether-rates-will-keep-dropping