February 9, 2026

Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

For self-employed professionals, securing a mortgage has traditionally felt like navigating a maze blindfolded. Despite earning substantial income, many entrepreneurs, freelancers, and business owners face rejection from traditional lenders simply because their tax returns don’t reflect their actual earning power. In 2026, bank statement loans are revolutionizing the mortgage landscape, offering a practical solution that recognizes the reality of self-employed income. This comprehensive guide explores how Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer is transforming homeownership opportunities for millions of independent workers.

Key Takeaways

✅ Bank statement loans qualify borrowers based on actual deposits rather than tax returns, making them ideal for self-employed individuals who write off business expenses

✅ Income calculation uses 12-24 months of bank statements, with lenders counting 80-100% of deposits from personal accounts and 50-75% from business accounts[1][2]

✅ Borrowers can qualify for 2-3 times more mortgage compared to conventional loans, despite higher interest rates (7-10%) and larger down payments (10-20%)[1]

✅ Minimum credit scores range from 620-680, with funds requiring 60-day seasoning to verify genuine assets[1][4]

✅ The 2026 competitive landscape promises better rates and terms as more lenders enter this growing market segment[9]

Understanding Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer

What Are Bank Statement Loans?

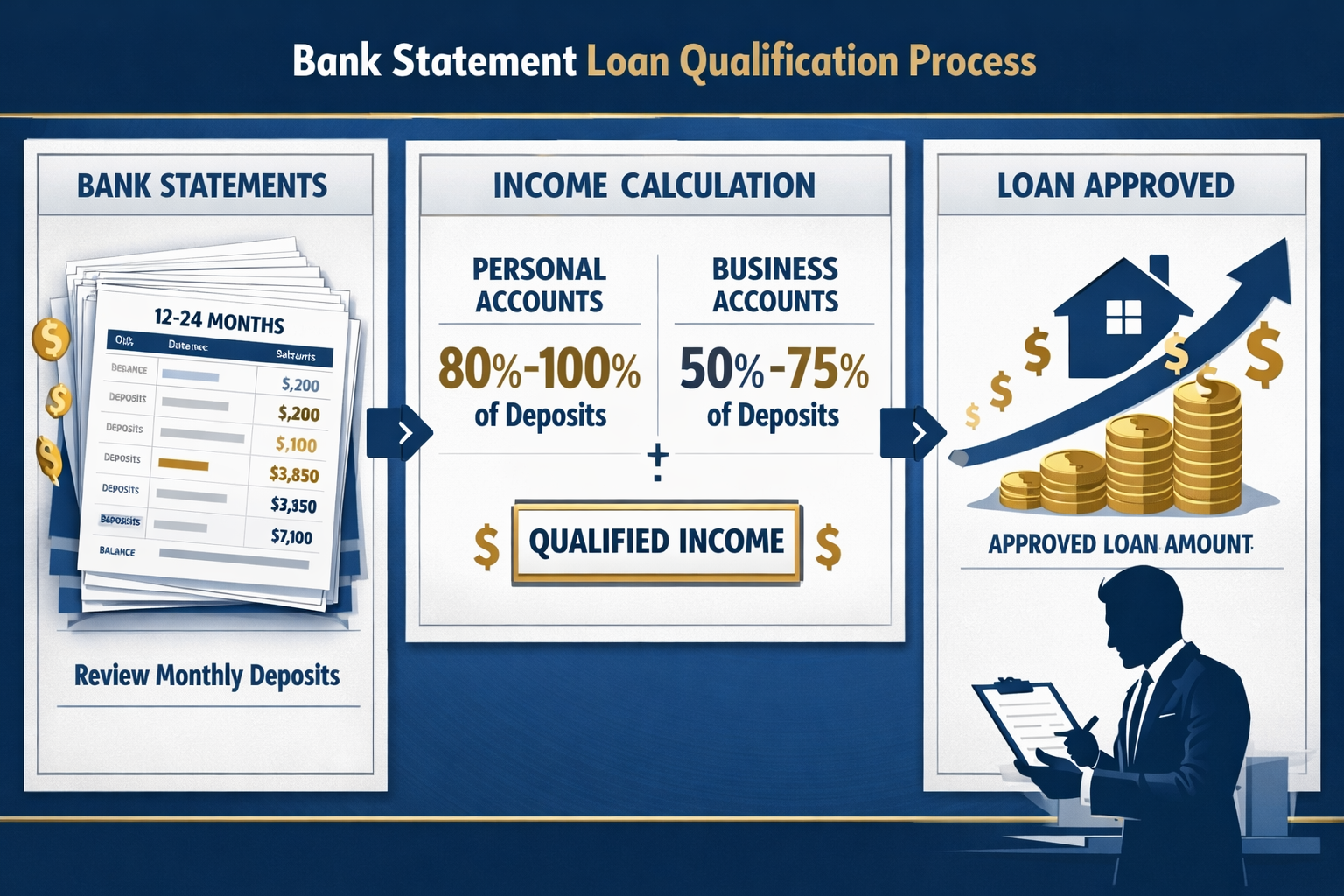

Bank statement loans represent a specialized mortgage product designed specifically for self-employed borrowers whose tax returns don’t accurately reflect their true income capacity. Unlike conventional mortgages that rely heavily on W-2 forms and tax returns, these loans use actual bank deposits to verify income and determine qualification amounts[1].

This approach makes perfect sense for business owners who legitimately reduce their taxable income through business deductions, depreciation, and other tax optimization strategies. While these practices are financially smart for tax purposes, they create a significant barrier when applying for traditional mortgages.

Why Bank Statement Loans Matter in 2026

The self-employed workforce continues to expand rapidly, with millions of Americans now working as independent contractors, business owners, or freelancers. According to research from the Urban Institute, self-employed borrowers are 40% less likely to receive conventional loan approval[1], creating a massive gap in the housing market.

In 2026, bank statement loans have emerged as the primary solution to this challenge. Lenders have refined their underwriting processes, expanded their programs, and increased competition for this valuable market segment. For self-employed borrowers seeking easier qualification, these loans offer a genuine pathway to homeownership.

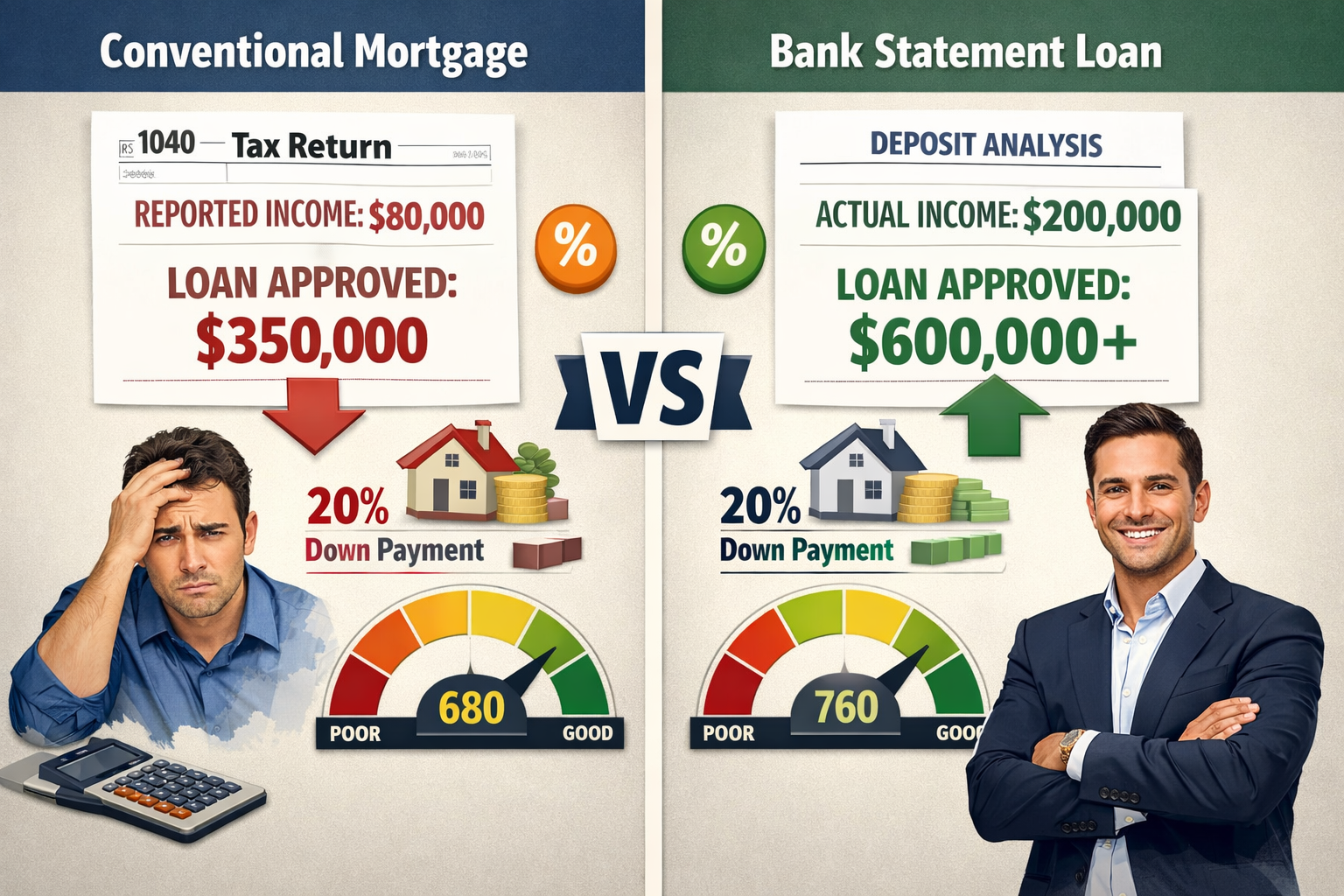

The Income Documentation Gap

Consider this real-world scenario: A successful freelance consultant earns $200,000 annually in gross income. After legitimate business deductions for home office expenses, equipment, travel, and other costs, their tax return shows only $80,000 in net income[1].

With a conventional mortgage:

- Lenders qualify based on the $80,000 reported income

- Maximum loan approval: approximately $350,000

- Many homes remain out of reach

With a bank statement loan:

- Lenders analyze actual deposits showing $200,000 income

- Maximum loan approval: $600,000 or more[1]

- Significantly expanded purchasing power

This dramatic difference explains why Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer has become such a critical topic in the mortgage industry.

How Bank Statement Loans Work: The Complete Process

Income Calculation Methodology

Understanding how lenders calculate qualifying income is essential for self-employed borrowers. The methodology differs based on account type:

Personal Bank Accounts:

- Lenders count 80-100% of total deposits as qualifying income[1][2]

- Higher percentage for borrowers with strong credit profiles

- Excludes transfers between accounts and one-time deposits

Business Bank Accounts:

- Lenders count 50-75% of total deposits[1][2]

- Accounts for business expenses (typically 50% expense factor)

- More conservative approach recognizes operational costs

Required Documentation Period

Most lenders require either 12 or 24 months of bank statements, depending on the specific program and lender requirements[1]. The longer documentation period provides:

- More comprehensive income verification

- Better understanding of seasonal fluctuations

- Reduced risk for lenders

- Potentially better rates for borrowers

Some programs accept 12-month statements for borrowers with exceptional credit scores and substantial down payments, while others mandate 24 months for all applicants.

The 60-Day Seasoning Requirement

A critical but often overlooked requirement is the 60-day fund seasoning rule[4]. This means all funds used for down payment and closing costs must have been in your accounts for at least 60 days before application.

This requirement prevents borrowers from:

- Using borrowed money for down payments

- Inflating account balances temporarily

- Misrepresenting their true financial position

Planning ahead is essential. Don’t wait until you’ve found your dream home to start organizing your finances. For more details on common mistakes self-employed homebuyers make, review comprehensive preparation strategies.

Qualification Requirements

Beyond income verification, bank statement loans require:

Credit Score:

- Minimum: 620-680 depending on lender[1][2]

- Higher scores unlock better rates

- 680+ considered strong position

Down Payment:

- Typically 10-20% or more[1]

- Higher than conventional mortgages

- Larger down payments may reduce interest rates

Debt-to-Income Ratio:

- Generally 43-50% maximum

- Calculated using bank statement income

- Varies by lender and program

Property Requirements:

- Primary residences, second homes, investment properties

- Standard appraisal requirements

- Property type restrictions may apply

Interest Rates and Costs: What to Expect in 2026

Current Rate Environment

Bank statement loans currently carry interest rates in the 7-10% range, approximately 1-3 percentage points above conventional mortgages[1]. While this premium might seem significant, it’s important to consider the context.

The rate premium reflects:

- Higher perceived risk for lenders

- Specialized underwriting requirements

- Smaller market segment compared to conventional loans

- Alternative documentation processing costs

Is the Rate Premium Worth It?

For most self-employed borrowers, the answer is a resounding yes. Consider the value proposition:

Scenario Analysis:

Conventional Loan (if approved):

- Loan amount: $350,000

- Interest rate: 6.5%

- Monthly payment: $2,212

- Limited home options

Bank Statement Loan:

- Loan amount: $600,000

- Interest rate: 8.5%

- Monthly payment: $4,615

- Access to desired properties

The higher payment reflects a significantly larger loan amount that enables purchase of the actual home you want, rather than settling for something smaller. Many self-employed borrowers find this trade-off worthwhile, especially when they can refinance to conventional terms once they have two years of tax returns showing higher income.

2026 Competitive Landscape Improvements

Exciting developments are emerging in 2026. As competition increases among lenders for market share in the self-employed segment, borrowers can expect[9]:

- More competitive interest rates as lenders vie for business

- Higher loan-to-value ratios reducing down payment requirements

- Streamlined application processes with faster approvals

- Expanded program options for various borrower profiles

These improvements make Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer an increasingly attractive option. Understanding mortgages for self-employed borrowers in the current market helps position you for success.

Comparing Bank Statement Loans to Alternative Options

Traditional Mortgages

Advantages:

- Lower interest rates (typically 1-3% less)

- Smaller down payment requirements

- Broader lender availability

- Established processes

Disadvantages:

- Requires tax returns showing sufficient income

- Difficult for self-employed with write-offs

- Lengthy documentation requirements

- Often results in lower approval amounts

Stated Income Mortgages

Before the 2008 financial crisis, stated income or “no-doc” loans were common. These allowed borrowers to simply state their income without verification. While similar in concept to bank statement loans, modern programs are fundamentally different:

Bank Statement Loans (2026):

- ✅ Require actual documentation (bank statements)

- ✅ Verify income through deposits

- ✅ Follow responsible lending standards

- ✅ Available from reputable lenders

Old Stated Income Loans:

- ❌ No income verification

- ❌ High fraud potential

- ❌ Contributed to financial crisis

- ❌ No longer available

For borrowers seeking alternative income verification methods, bank statement loans provide a legitimate, well-regulated option.

Asset-Based Mortgages

Another alternative for high-net-worth self-employed borrowers is asset-based lending, which qualifies borrowers based on investment portfolios rather than income. This works well for:

- Retired entrepreneurs with substantial assets

- Real estate investors with multiple properties

- Borrowers with significant investment accounts

However, most self-employed professionals seeking primary residence financing find bank statement loans more accessible and practical.

Navigating the Application Process

Preparation Steps

Success with bank statement loans begins long before application. Follow these preparation steps:

1. Organize Your Bank Statements

- Gather 12-24 months of statements

- Include all accounts showing deposits

- Ensure statements are complete and legible

- Separate personal and business accounts clearly

2. Review for Red Flags

- Identify and explain large one-time deposits

- Document transfers between accounts

- Remove or explain unusual transactions

- Ensure consistent deposit patterns

3. Calculate Your Qualifying Income

- Total deposits over the required period

- Subtract transfers and one-time items

- Apply the appropriate percentage (80-100% personal, 50-75% business)

- Compare to your housing budget

4. Verify Fund Seasoning

- Ensure down payment funds have 60-day history[4]

- Document source of all recent large deposits

- Avoid moving money between accounts unnecessarily

- Maintain stable balances

Working with the Right Lender

Not all lenders offer bank statement loans, and those that do may have vastly different programs. Consider:

Lender Selection Criteria:

- Experience with self-employed borrowers

- Competitive rates and terms

- Transparent fee structure

- Responsive communication

- Positive reviews from similar borrowers

Questions to Ask Potential Lenders:

- What percentage of deposits do you count as income?

- Do you require 12 or 24 months of statements?

- What are your minimum credit score requirements?

- What down payment percentages do you offer?

- Are there prepayment penalties?

- What property types do you finance?

Given the stricter lending standards and higher scrutiny for self-employed clients, finding an experienced lender makes a substantial difference.

Common Application Challenges

Even with proper preparation, self-employed borrowers may encounter challenges:

Irregular Income Patterns:

- Solution: Provide context for seasonal fluctuations

- Example: Tax professionals earn more during tax season

- Approach: Average income over full 12-24 month period

Multiple Income Streams:

- Solution: Document each income source separately

- Example: Consulting fees, rental income, investment returns

- Approach: Provide clear categorization and documentation

Recent Business Start:

- Solution: May need to wait for sufficient bank statement history

- Example: Business operating less than 12 months

- Approach: Consider alternative programs or wait for documentation period

Co-Mingled Funds:

- Solution: Separate personal and business finances going forward

- Example: Using one account for all transactions

- Approach: Provide detailed transaction categorization

Real-World Success Stories and Use Cases

Case Study 1: The Freelance IT Consultant

Profile:

- Freelance IT consultant

- Annual gross income: $180,000

- Tax return net income: $75,000 (after home office, equipment, vehicle deductions)

- Credit score: 720

- Down payment: 15% ($90,000)

Conventional Mortgage Attempt:

- Qualified for: $325,000

- Insufficient for desired property in target area

Bank Statement Loan Solution:

- Analyzed 24 months of business account statements

- Calculated qualifying income: $135,000 (75% of deposits)

- Approved for: $540,000

- Interest rate: 8.25%

- Successfully purchased desired home

For similar scenarios, review this IT consultant self-employed mortgage case for additional insights.

Case Study 2: The E-Commerce Entrepreneur

Profile:

- Online retail business owner

- Annual gross income: $250,000

- Tax return net income: $60,000 (significant inventory and advertising expenses)

- Credit score: 680

- Down payment: 20% ($120,000)

Bank Statement Loan Solution:

- Used 12 months of business bank statements

- Demonstrated consistent deposit patterns

- Qualifying income calculated: $175,000 (70% of deposits)

- Approved for: $600,000

- Interest rate: 8.75%

- Purchased commercial property with residential component

Case Study 3: The Multi-Stream Income Professional

Profile:

- Combination of consulting, rental properties, and investment income

- Total annual income: $220,000

- Tax return shows: $95,000 (after depreciation on rentals)

- Credit score: 740

- Down payment: 20% ($150,000)

Bank Statement Loan Solution:

- Combined personal and business account analysis

- Documented all income streams clearly

- Qualifying income: $198,000 (90% of personal deposits)

- Approved for: $750,000

- Interest rate: 7.75%

- Secured luxury primary residence

These examples demonstrate how Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer opens doors that conventional financing keeps closed.

Strategic Considerations for 2026 and Beyond

Timing Your Application

Strategic timing can significantly impact your bank statement loan success:

Ideal Timing Scenarios:

- After strong income year: If you’ve had 12-24 months of excellent deposits

- Before major business changes: Apply before restructuring that might affect income visibility

- When rates are favorable: Monitor market conditions and apply during competitive periods

- After credit improvement: Wait if you’re close to a higher credit tier

Refinancing Strategies

Many borrowers use bank statement loans as a bridge strategy:

The Refinance Timeline:

Year 1-2: Purchase with bank statement loan

- Accept higher interest rate

- Build equity through payments and appreciation

- Establish property ownership

Year 3-4: Prepare tax returns showing higher income

- Reduce business deductions strategically

- Show qualifying income on tax returns

- Build refinancing documentation

Year 5+: Refinance to conventional mortgage

- Secure lower interest rate

- Reduce monthly payments

- Eliminate bank statement loan premium

This strategy allows you to purchase the home you want now while planning for lower costs later. Understanding self-employed mortgage approval processes helps optimize this timeline.

Tax Planning Considerations

Bank statement loans create an interesting dynamic for tax planning:

Before Bank Statement Loan:

- Maximize business deductions

- Minimize taxable income

- Optimize tax efficiency

During Bank Statement Loan Application:

- Maintain strong deposit patterns

- Document all income clearly

- Ensure consistent banking activity

After Securing Loan (if planning to refinance):

- Consider reducing some deductions

- Show higher net income on tax returns

- Build conventional refinancing eligibility

Consult with both your mortgage professional and tax advisor to develop a coordinated strategy that serves both objectives.

Market Trends to Watch

Several trends are shaping the bank statement loan landscape in 2026:

📈 Increased Lender Competition: More financial institutions are entering this space, driving better terms[9]

📈 Technology Integration: Automated bank statement analysis is streamlining approvals

📈 Expanded Eligibility: Some lenders are reducing minimum credit scores and down payments

📈 Product Innovation: New hybrid programs combining bank statements with other documentation

📈 Rate Compression: The gap between conventional and bank statement rates is narrowing

These trends suggest that Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer will become even more accessible and affordable in coming years.

Potential Pitfalls and How to Avoid Them

Red Flags in Bank Statements

Lenders scrutinize bank statements for concerning patterns. Avoid these red flags:

❌ Frequent Overdrafts:

- Indicates poor cash flow management

- Suggests financial instability

- Solution: Maintain positive balances for 6+ months before applying

❌ Unexplained Large Deposits:

- Raises questions about income source

- May indicate borrowed funds

- Solution: Document all large deposits with clear explanations

❌ Irregular Income Patterns:

- Makes income calculation difficult

- Increases perceived risk

- Solution: Provide context for seasonal businesses or project-based work

❌ Numerous NSF Fees:

- Demonstrates financial management issues

- Reduces lender confidence

- Solution: Clean up banking habits well before application

❌ Cash Deposits Without Documentation:

- Cannot be verified or counted

- Raises compliance concerns

- Solution: Deposit all income through verifiable channels (checks, wire transfers, electronic payments)

Documentation Mistakes

Common documentation errors that delay or derail applications:

Missing Statement Pages:

- Lenders need complete, consecutive statements

- Solution: Request full statement sets from your bank

Illegible Copies:

- Poor quality scans or photocopies

- Solution: Download clear PDF statements directly from online banking

Inconsistent Account Information:

- Name variations or address mismatches

- Solution: Ensure all accounts show current, accurate information

Unexplained Gaps:

- Missing months in the documentation period

- Solution: Provide complete timeline without gaps

Maximizing Your Approval Odds

Credit Score Optimization

While bank statement loans accept lower credit scores (620-680 minimum)[1][2], higher scores unlock better terms:

Score Range Benefits:

| Credit Score | Interest Rate Impact | Down Payment Options | Approval Likelihood |

|---|---|---|---|

| 620-659 | Highest rates | 20%+ required | Moderate |

| 660-699 | Mid-range rates | 15-20% | Good |

| 700-739 | Better rates | 10-15% | Very Good |

| 740+ | Best available rates | 10% possible | Excellent |

Quick Credit Improvements:

- Pay down credit card balances below 30% utilization

- Dispute any errors on credit reports

- Avoid new credit applications before mortgage

- Make all payments on time for 6+ months

Down Payment Strategies

Larger down payments improve approval odds and reduce rates:

10% Down Payment:

- Minimum for many programs

- Higher interest rates

- More stringent qualification

15% Down Payment:

- Better rate options

- Improved approval likelihood

- Reduced monthly payments

20% Down Payment:

- Best rates available

- Avoids mortgage insurance (if applicable)

- Strongest negotiating position

25%+ Down Payment:

- Maximum lender confidence

- Potential rate discounts

- Expanded property options

Income Presentation

How you present your income makes a difference:

Best Practices:

- Provide clear, organized statements

- Create a summary sheet calculating qualifying income

- Explain any unusual transactions proactively

- Document seasonal or cyclical income patterns

- Show consistent or growing income trends

The Future of Bank Statement Loans

Regulatory Environment

The bank statement loan market operates within a regulated framework that balances access with responsible lending. In 2026, regulations continue to evolve:

Current Regulatory Framework:

- Ability-to-Repay (ATR) requirements ensure borrowers can afford loans

- Documentation standards prevent return to pre-2008 practices

- Lender accountability maintains market integrity

Expected Developments:

- Potential standardization of income calculation methods

- Increased transparency requirements

- Enhanced consumer protections

- Possible expansion of qualifying documentation types

Technology and Innovation

Technology is transforming the bank statement loan process:

Current Innovations:

- Automated statement analysis reducing processing time

- Digital document submission and verification

- AI-powered income calculation

- Faster approval timelines (days instead of weeks)

Future Possibilities:

- Real-time bank account verification

- Blockchain-based income documentation

- Instant preliminary approvals

- Integration with accounting software

Market Growth Projections

The self-employed segment continues expanding, driving demand for bank statement loans:

Growth Drivers:

- Increasing gig economy participation

- More professionals choosing self-employment

- Remote work enabling entrepreneurship

- Generational shift toward independent work

Market Response:

- More lenders entering the space[9]

- Competitive pressure improving terms

- Product innovation and customization

- Better borrower education and resources

This growth trajectory reinforces why Bank Statement Loans for Self-Employed Borrowers: The 2026 Game-Changer represents a fundamental shift in mortgage lending.

Conclusion: Taking Action on Your Homeownership Goals

Bank statement loans have emerged as a genuine game-changer for self-employed borrowers in 2026, offering a practical pathway to homeownership that recognizes the reality of entrepreneurial income. While these loans carry higher interest rates and require larger down payments than conventional mortgages, they provide access to 2-3 times more purchasing power for borrowers whose tax returns don’t reflect their true earning capacity[1].

Key Success Factors

To maximize your success with bank statement loans:

✅ Prepare thoroughly: Organize 12-24 months of clean bank statements showing consistent deposits

✅ Understand the math: Calculate your qualifying income using lender formulas (80-100% personal, 50-75% business)[1][2]

✅ Season your funds: Ensure down payment money has 60-day account history[4]

✅ Optimize your credit: Target 680+ score for best rates and terms

✅ Work with specialists: Choose lenders experienced with self-employed borrowers

✅ Plan strategically: Consider bank statement loans as a bridge to eventual conventional refinancing

Next Steps

Ready to explore bank statement loan options? Take these immediate actions:

1. Assess Your Qualification

- Gather recent bank statements

- Calculate potential qualifying income

- Review your credit score

- Evaluate available down payment funds

2. Research Lenders

- Identify lenders offering bank statement programs

- Compare rates, terms, and requirements

- Read reviews from self-employed borrowers

- Schedule consultations with top candidates

3. Prepare Your Documentation

- Request complete bank statement sets

- Organize statements chronologically

- Document any unusual transactions

- Create income summary calculations

4. Address Weak Areas

- Improve credit score if below 680

- Build down payment savings if needed

- Clean up bank statement red flags

- Establish consistent deposit patterns

5. Get Pre-Qualified

- Submit preliminary application

- Receive initial assessment

- Understand your buying power

- Begin home search with confidence

For comprehensive guidance on navigating the self-employed mortgage landscape, explore additional resources on self-employed mortgages and connect with experienced mortgage professionals who understand your unique situation.

The 2026 lending environment offers unprecedented opportunities for self-employed borrowers. Bank statement loans provide the flexibility and recognition that entrepreneurial income deserves, transforming homeownership from an impossible dream into an achievable reality. Don’t let tax optimization strategies prevent you from purchasing the home you’ve earned—leverage bank statement loans to unlock your true purchasing power and achieve your homeownership goals.

References

[1] Bank Statement Loan Interest Rates – https://www.mcgowanmortgages.com/bank-statement-loan-interest-rates/

[2] Heloc Approval For Self Employed – https://themortgagereports.com/126395/heloc-approval-for-self-employed

[3] Bank Statement Loan Guide – https://www.nmhl.us/guides/bank-statement-loan-guide

[4] Bank Statements For Mortgages In Complete Guide To Requirements Red Flags And Approval Strategies – https://www.amerisave.com/learn/bank-statements-for-mortgages-in-complete-guide-to-requirements-red-flags-and-approval-strategies

[5] Bank Statement Loan Examples And Use Cases – https://griffinfunding.com/blog/bank-statement-loans/bank-statement-loan-examples-and-use-cases/

[6] Watch – https://www.youtube.com/watch?v=iDyOyvLtMWs

[7] Bank Statement Loans More Mortgage Options For Self Employed Buyers And Homeowners As Rates Ease – https://www.housingwire.com/articles/bank-statement-loans-more-mortgage-options-for-self-employed-buyers-and-homeowners-as-rates-ease/

[8] Bank Statement Loans – https://societymortgage.com/purchase/bank-statement-loans/

[9] Non Qm Lending Trends To Watch In 2026 What Brokers Need To Prepare For – https://www.nqmf.com/non-qm-lending-trends-to-watch-in-2026-what-brokers-need-to-prepare-for/