February 4, 2026

Bank Statement Mortgages for Self-Employed Borrowers: Securing the Best Rates in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Self-employed professionals, freelancers, and business owners face unique challenges when applying for traditional mortgages. Tax deductions that reduce taxable income—while financially savvy—often make it difficult to demonstrate sufficient earnings on conventional loan applications. Enter Bank Statement Mortgages for Self-Employed Borrowers: Securing the Best Rates in 2026, a specialized lending solution that uses 12-24 months of deposit history to qualify borrowers, bypassing the limitations of tax return documentation. 💼

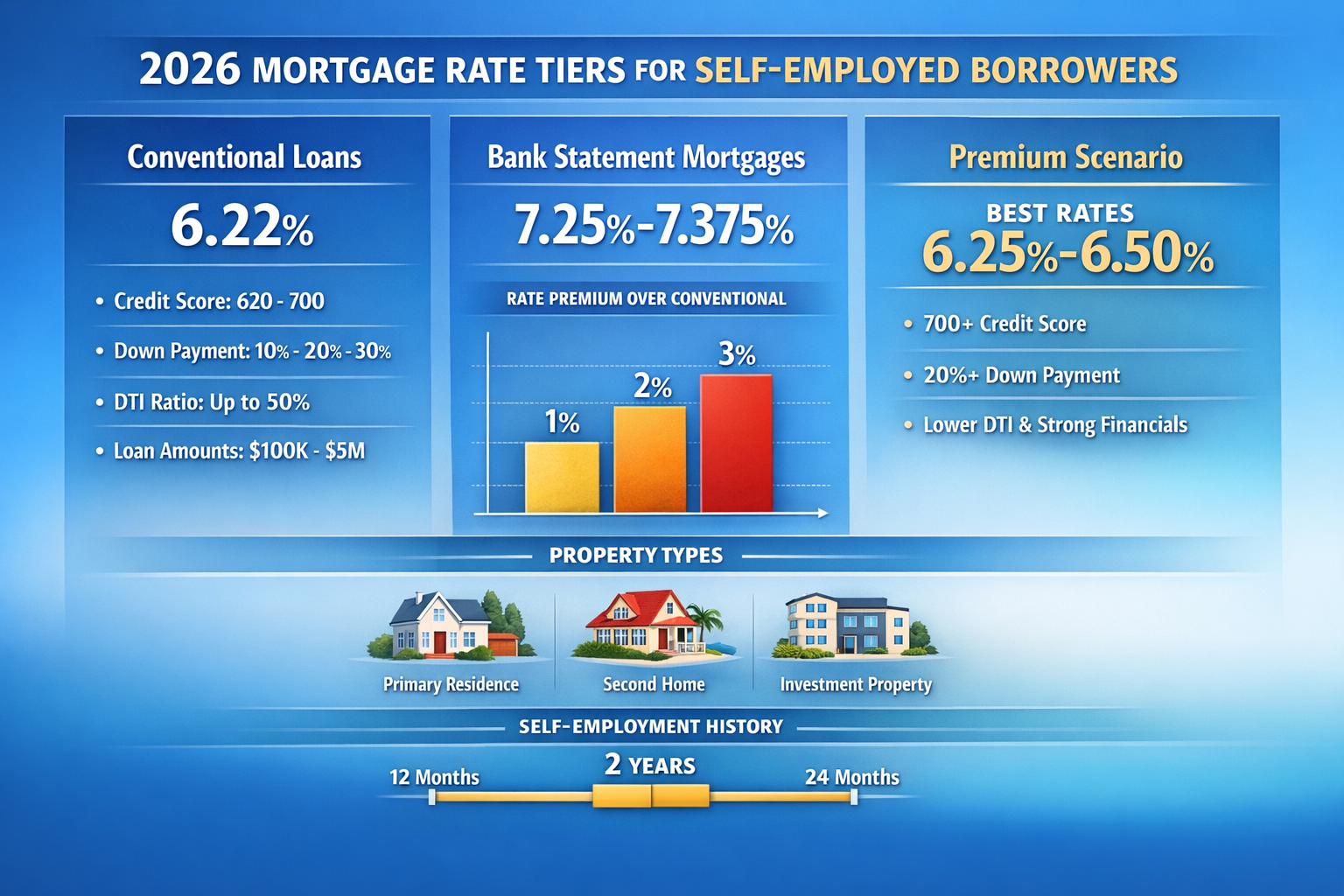

As mortgage rates continue to ease from their recent peaks, with conventional 30-year fixed rates averaging 6.22% as of December 2025[1], self-employed borrowers now have unprecedented opportunities to secure competitive financing. While bank statement loans typically carry a premium of 0.25-1% over conventional options, savvy borrowers can find rates around 7.25% in early 2026[8]—a significant improvement from previous years and a gateway to homeownership that traditional underwriting might deny.

Key Takeaways

- Alternative Documentation: Bank statement mortgages use 12-24 months of personal or business bank statements to calculate income, eliminating the need for tax returns that often understate self-employed earnings[1][2]

- Competitive 2026 Rates: Current bank statement loan rates range from 7.25-7.375%, representing a manageable premium over conventional mortgages while providing qualification flexibility[8]

- Flexible Qualification Standards: These programs accommodate higher debt-to-income ratios (up to 50%), lower credit scores (starting at 620), and diverse property types including investment properties[2][4]

- Substantial Loan Amounts: Bank statement mortgages support loan amounts from $100,000 to $5 million, with down payments as low as 10% for qualified borrowers[2]

- Strategic Rate Optimization: Borrowers with credit scores above 680, larger down payments (20%+), and clean 24-month bank statement histories secure the most competitive rates in 2026

Understanding Bank Statement Mortgages for Self-Employed Borrowers

What Are Bank Statement Mortgages?

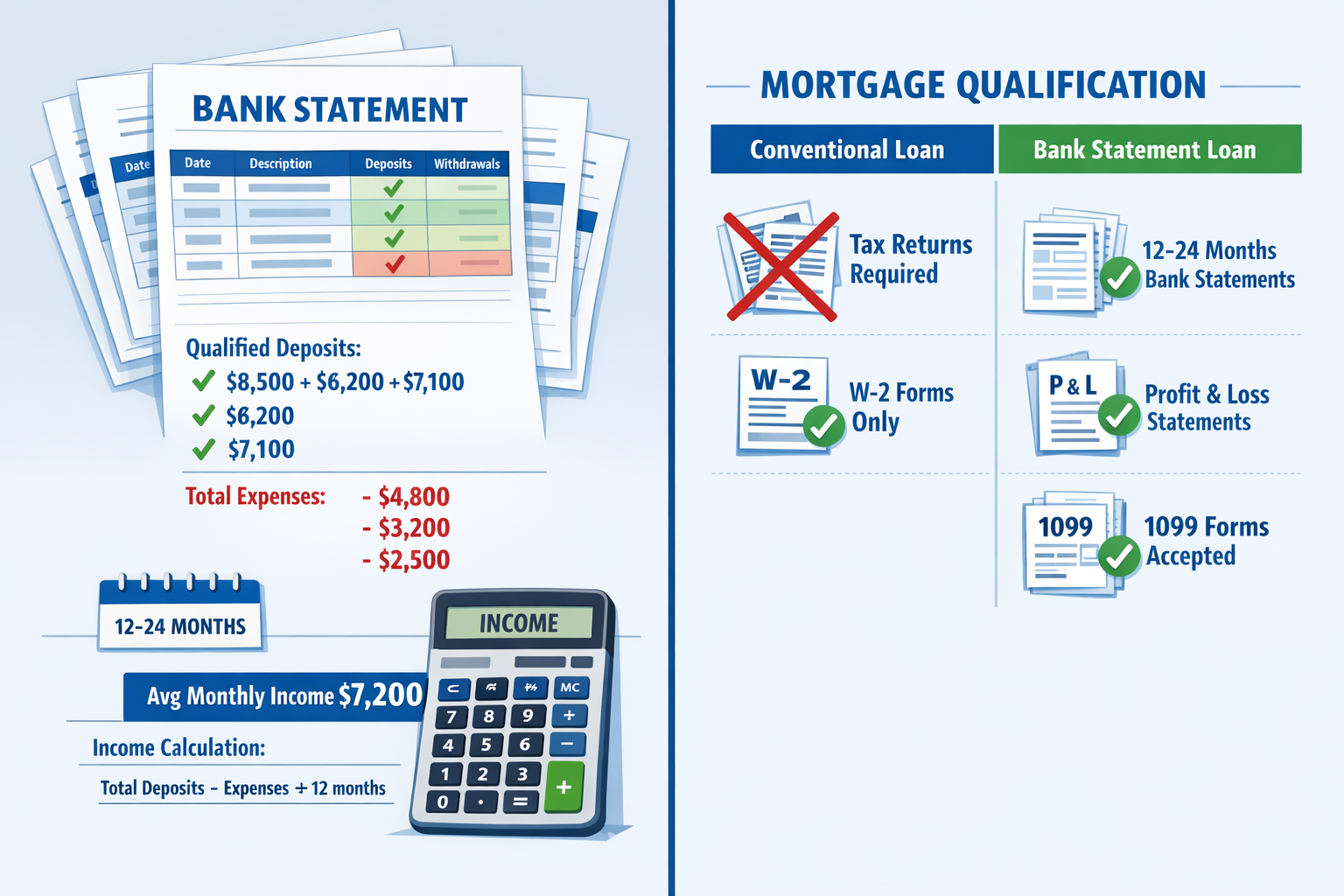

Bank statement mortgages represent a category of non-qualified mortgage (non-QM) loans specifically designed for self-employed individuals whose income documentation doesn’t fit conventional lending guidelines. Unlike traditional mortgages that require W-2 forms and tax returns, these programs analyze actual cash flow through bank deposits to determine borrowing capacity[1][4].

For self-employed borrowers who maximize business deductions, this approach reveals true earning potential. A contractor who shows $60,000 in taxable income after deductions might actually deposit $120,000 annually into business accounts—bank statement loans capture this reality.

How Income Calculation Works

Lenders typically use one of several methods to calculate qualifying income from bank statements:

Personal Bank Statements: Lenders review 12-24 months of personal account deposits, identifying qualified income sources while excluding non-recurring deposits like transfers between accounts or loan proceeds[2].

Business Bank Statements: For business owners, lenders analyze business account deposits and apply an expense factor (typically 25-50%) to account for operating costs, calculating net income available for mortgage qualification[1][4].

Hybrid Approach: Some borrowers provide both personal and business statements, allowing lenders to capture the full picture of financial capacity.

The calculation methodology varies by lender, but most apply conservative expense ratios to ensure sustainable income projections. This approach provides a more accurate assessment than tax returns for many self-employed professionals.

Who Benefits Most from Bank Statement Loans?

These specialized mortgage products serve various self-employed professionals:

- Independent Contractors: Those who receive 1099 income and take substantial business deductions

- Small Business Owners: Entrepreneurs who reinvest profits back into their companies

- Freelancers and Gig Workers: Professionals with multiple income streams that don’t fit traditional employment models

- Real Estate Investors: Property owners whose rental income appears reduced after depreciation and expenses

- Commissioned Sales Professionals: Those with variable income that fluctuates significantly year-to-year

For contractors seeking mortgage solutions, bank statement programs offer a practical alternative to conventional underwriting that may not recognize their full earning potential.

Bank Statement Mortgages for Self-Employed Borrowers: Securing the Best Rates in 2026 – Current Rate Environment

2026 Rate Landscape

The mortgage rate environment in 2026 presents favorable conditions for self-employed borrowers considering bank statement loans. According to recent data, conventional 30-year fixed mortgage rates averaged 6.22% as of December 11, 2025—down from 6.60% a year earlier, representing a meaningful 38 basis point decline[1].

For bank statement mortgages specifically, rates in late January 2026 were observed in the 7.25-7.375% range[8], reflecting the typical premium these alternative documentation loans carry over conventional products.

Understanding Rate Premiums

Bank statement loans generally carry rates 1-3% higher than conventional mortgages[4], though the actual premium depends on several factors:

| Factor | Impact on Rate | Optimization Strategy |

|---|---|---|

| Credit Score | 680+ qualifies for best pricing | Improve score before applying |

| Down Payment | 20%+ reduces rate premium | Larger down payment = lower rate |

| Bank Statement History | 24 months better than 12 | Provide longer history when possible |

| Property Type | Primary residence gets best rates | Consider property use carefully |

| Loan Amount | Conforming limits may offer better pricing | Structure loan strategically |

| Debt-to-Income Ratio | Lower DTI = better rates | Pay down existing debts |

The premium reflects the increased risk assessment lenders undertake when using alternative documentation. However, for self-employed borrowers who cannot qualify conventionally, this premium represents access to homeownership rather than an unnecessary cost.

Comparing Loan Options

When evaluating Bank Statement Mortgages for Self-Employed Borrowers: Securing the Best Rates in 2026, it’s essential to understand how these products compare to other alternatives:

Conventional Mortgages: Require tax returns showing sufficient income, typically favor DTI ratios below 43%, and offer the lowest rates (currently around 6.22%)[1]. Best for self-employed borrowers who show strong income on tax documents.

Bank Statement Mortgages: Use 12-24 months of deposits for qualification, allow DTI up to 50%, and carry rates of 7.25-7.375%[2][8]. Ideal for those with tax write-offs that reduce documented income.

Profit & Loss Statement Loans: Accept CPA-prepared P&L statements instead of tax returns, offering middle-ground qualification between conventional and bank statement programs[1].

1099 Loans: Specifically designed for independent contractors receiving 1099 income, using these forms as primary documentation[1].

For IT consultants and self-employed professionals in specialized fields, understanding these distinctions helps identify the optimal financing path.

Qualification Requirements for Bank Statement Mortgages

Credit Score Minimums

Credit score requirements for bank statement mortgages vary by lender, with most programs requiring a minimum score between 620-700[2][3][5]. However, the specific threshold significantly impacts both approval odds and interest rates:

- 680+ Credit Score: Qualifies for best available rates and down payment options as low as 10%[3]

- 660-679 Credit Score: Moderate pricing with 15-20% down payment typically required

- 620-659 Credit Score: Higher rates and down payments (20-30%) expected[5]

Borrowers with recent credit events—bankruptcies, foreclosures, or significant delinquencies—may face additional waiting periods or higher down payment requirements even if their credit score meets minimum thresholds.

Improving your credit score before applying can save thousands over the loan’s lifetime. Understanding the role of credit scores in mortgage approval provides valuable context for preparation strategies.

Down Payment Requirements

Down payment expectations for bank statement mortgages typically range from 10-20%, though specific requirements depend on multiple factors[3][5]:

Standard Requirements:

- 10% minimum with credit score 680+ and mortgage insurance[3]

- 15-20% for most borrowers with solid credit and income documentation

- 25-30% for borrowers with recent credit issues or complex income situations[5]

Loan-to-Value (LTV) Ratios:

- Purchase and rate-and-term refinances: Up to 90% LTV[2]

- Cash-out refinances: Typically capped at 80% LTV[2]

- Investment properties: Often require 20-25% down minimum

Higher down payments not only improve approval odds but also reduce interest rates and eliminate mortgage insurance requirements at 20%+ equity.

Income Documentation Standards

The cornerstone of bank statement mortgage qualification is comprehensive income documentation. Lenders typically require:

Bank Statement Requirements:

- 12-24 months of consecutive personal or business bank statements[1][2]

- All pages must be included (no gaps or missing months)

- Statements must show consistent deposit patterns

- Large, non-recurring deposits may be excluded from income calculations

Supporting Documentation:

- Business license or proof of self-employment (2+ years required)[1][4]

- CPA letter verifying business operation and income stability

- Profit & Loss statements for additional income verification

- 1099 forms when available to supplement bank statement analysis[1]

Income Calculation Methods: Lenders analyze qualified deposits and apply expense factors ranging from 0% (personal accounts) to 50% (business accounts) depending on the documentation type[4]. This conservative approach ensures borrowers can sustain mortgage payments alongside business operations.

Debt-to-Income Ratio Flexibility

One significant advantage of bank statement mortgages is their accommodation of higher debt-to-income ratios. While conventional mortgages typically favor DTI ratios below 43%, bank statement programs allow up to 50% DTI[4], providing crucial qualification flexibility for self-employed borrowers with:

- Existing business debts or equipment financing

- Student loans or personal debt obligations

- Multiple investment properties with mortgage payments

- High-income profiles that can support elevated debt levels

This flexibility recognizes that self-employed individuals often carry business-related debts that don’t impact personal cash flow as severely as traditional underwriting suggests.

Property Types and Loan Structures

Eligible Property Types

Bank statement mortgage programs offer remarkable flexibility in property type eligibility, supporting diverse real estate investment strategies:

✅ Primary Residences: Best rates and terms available, down payments as low as 10%[4]

✅ Second Homes: Slightly higher rates than primary residences, typically 15-20% down

✅ Investment Properties: Competitive programs available, usually requiring 20-25% down[4]

✅ Non-Warrantable Condominiums: Properties that don’t meet conventional lending guidelines due to investor concentration, pending litigation, or other factors[4]

✅ Multi-Unit Properties: 2-4 unit properties where borrower occupies one unit

This versatility makes bank statement loans particularly attractive for self-employed individuals investing in rental properties, as the same qualification method can support both personal residence and investment property purchases.

Loan Amount Ranges

Bank statement mortgage programs accommodate a wide spectrum of loan amounts, from modest purchases to luxury properties:

Typical Loan Amount Range: $100,000 to $5,000,000[2]

This broad range ensures accessibility for:

- First-time homebuyers in affordable markets

- Move-up buyers purchasing larger primary residences

- High-net-worth individuals seeking jumbo financing

- Real estate investors building property portfolios

Jumbo loan amounts (exceeding conforming loan limits) may carry slightly higher rates but remain accessible to qualified self-employed borrowers with strong bank statement histories.

Available Loan Terms

Bank statement mortgages offer various term structures to match borrower preferences and financial strategies:

Standard Fixed-Rate Terms:

- 30-Year Fixed: Most popular option, providing payment stability and lower monthly obligations[1]

- 15-Year Fixed: Higher payments but significant interest savings over loan lifetime[1]

Alternative Structures:

- 40-Year Fixed: Extended amortization reducing monthly payments, available through select portfolio lenders[2]

- Interest-Only Options: Initial period with interest-only payments, then converting to fully amortizing[2]

- Adjustable-Rate Mortgages (ARMs): Initial fixed period (5, 7, or 10 years) followed by rate adjustments

The availability of these diverse structures depends on the specific lender and program. Borrowers should carefully evaluate fixed versus variable mortgage options based on their financial situation and market outlook.

Strategies for Securing the Best Rates in 2026

Optimize Your Bank Statement History

The quality and consistency of your bank statement history directly impacts both approval odds and interest rates. Implement these strategies 12-24 months before applying:

📊 Maintain Consistent Deposits: Regular, predictable income patterns demonstrate stability. Avoid dramatic month-to-month fluctuations when possible.

🏦 Use Dedicated Accounts: Separate business and personal finances clearly. Commingled accounts complicate income calculations and may result in conservative underwriting.

💰 Minimize Non-Sufficient Funds (NSF): Overdrafts and bounced checks signal financial instability. Maintain adequate account balances consistently.

📝 Document Large Deposits: Be prepared to explain any unusual or one-time deposits with supporting documentation showing they’re income rather than loans or transfers.

⏰ Provide 24 Months When Possible: While 12-month programs exist, 24-month bank statement histories typically qualify for better rates and terms[1].

Strengthen Your Credit Profile

Credit score optimization can reduce your interest rate by 0.5-1% or more, translating to substantial savings:

Immediate Actions (30-90 days):

- Pay down credit card balances below 30% utilization

- Dispute any errors on credit reports

- Become an authorized user on accounts with perfect payment history

- Avoid new credit applications during the mortgage process

Medium-Term Strategies (3-12 months):

- Establish payment reminders to ensure on-time payments

- Diversify credit mix if you only have one type of credit

- Keep old accounts open to maintain credit history length

- Consider credit-builder loans if your score is below 680

For detailed guidance, review these tips to rapidly improve your credit score before applying.

Maximize Your Down Payment

Every additional percentage point in down payment can improve your rate and terms:

10% Down: Minimum for well-qualified borrowers (680+ credit), requires mortgage insurance[3]

15% Down: Moderate improvement in rates, still requires mortgage insurance

20% Down: Eliminates mortgage insurance, qualifies for best available rates, reduces monthly payment

25%+ Down: Premium pricing tier, maximum lender confidence, lowest rates available[5]

Consider these down payment funding sources:

- Business savings and retained earnings

- Sale of investments or other real estate

- Gifts from family members (with proper documentation)

- Retirement account withdrawals (evaluate tax implications)

- Home equity from existing properties

Compare Multiple Lenders

Bank statement mortgage programs vary significantly between lenders in terms of rates, fees, and qualification criteria. Obtain quotes from at least 3-5 lenders including:

Portfolio Lenders: Banks and credit unions that keep loans on their own books, offering flexibility in underwriting

Non-QM Specialists: Lenders focusing specifically on alternative documentation mortgages with competitive bank statement programs

Mortgage Brokers: Professionals with access to multiple lenders who can shop your scenario for optimal pricing

Credit Unions: Member-owned institutions sometimes offering relationship-based pricing advantages

When comparing offers, evaluate the complete picture beyond just interest rates:

- Origination fees and lender charges

- Third-party closing costs

- Prepayment penalties (some bank statement loans include them)

- Rate lock periods and extension fees

- Underwriting timeline and closing speed

Consider Rate Buydown Options

Some lenders offer discount points—upfront fees paid to reduce your interest rate. Each point typically costs 1% of the loan amount and reduces the rate by approximately 0.25%.

Example Calculation:

- Loan Amount: $400,000

- One Point Cost: $4,000

- Rate Reduction: 0.25%

- Monthly Payment Savings: ~$60

- Break-Even Period: 67 months

Buydowns make sense for borrowers who:

- Plan to keep the property and loan long-term (5+ years)

- Have excess cash available after down payment and reserves

- Want to maximize qualification by lowering monthly payments

- Expect rates to remain elevated or increase further

Timing Your Application

Strategic timing can influence both rate availability and qualification success:

Market Timing Considerations:

- Monitor interest rate trends and economic indicators

- Consider rate lock strategies when favorable rates appear

- Avoid peak season competition (spring/summer) when possible

Personal Timing Factors:

- Apply when your bank statements show strongest income patterns

- Avoid periods immediately after large business expenses or slow months

- Ensure 2+ years of self-employment history before applying[1][4]

- Time application after credit score improvements take effect

Common Mistakes to Avoid

Documentation Errors

❌ Incomplete Bank Statements: Missing pages or months create underwriting delays and may result in denial. Always provide complete, consecutive statements for the entire required period.

❌ Commingled Personal and Business Funds: Mixed-use accounts complicate income calculations. Maintain separate accounts for at least 12 months before applying.

❌ Unexplained Large Deposits: Lenders scrutinize unusual deposits carefully. Be prepared to document the source of any deposits exceeding 25% of monthly income.

❌ Last-Minute Account Changes: Opening new accounts or moving money between accounts immediately before applying raises red flags. Maintain stable banking patterns.

Financial Missteps

❌ Depleting Cash Reserves: Lenders require 6-12 months of reserves (mortgage payments) after closing. Don’t exhaust all savings for down payment and closing costs.

❌ Taking on New Debt: Avoid new car loans, credit cards, or business financing during the application process. New debts increase your DTI ratio and may disqualify you.

❌ Making Large Purchases: Major purchases before closing can impact cash reserves and debt ratios. Wait until after closing to buy furniture, vehicles, or equipment.

❌ Ignoring Tax Implications: Consult with a tax professional about the implications of business structure and income reporting strategies on mortgage qualification.

Application Strategy Errors

❌ Applying to Too Many Lenders: Multiple hard credit inquiries can temporarily lower your score. Work with a mortgage broker or limit applications to 2-3 lenders within a 14-day window.

❌ Providing Inconsistent Information: Ensure all application details match supporting documentation exactly. Discrepancies trigger additional verification and delays.

❌ Failing to Disclose All Income Sources: Include all qualifying income sources in your application. Additional income streams strengthen your profile.

❌ Rushing the Process: Bank statement mortgages require thorough documentation review. Allow 30-45 days for underwriting and closing rather than conventional 21-30 day timelines.

For comprehensive guidance on application best practices, review these common mistakes to avoid when applying for a mortgage.

Alternative Documentation Options

While bank statement mortgages offer excellent solutions for many self-employed borrowers, alternative documentation programs may better suit specific situations:

Profit & Loss Statement Programs

CPA-prepared profit and loss statements can qualify borrowers without providing tax returns or bank statements[1]. These programs typically require:

- Current year-to-date P&L statement

- Previous 1-2 years of P&L statements

- CPA certification letter

- Business license and proof of operation

Best for: Established businesses with clean accounting records and CPA relationships.

1099 Income Programs

Lenders specializing in 1099 documentation accept these tax forms as primary income verification[1]. Requirements include:

- 2 years of 1099 forms from clients

- Proof of continued business relationships

- Minimal expense deductions claimed

- Consistent or increasing income trends

Best for: Independent contractors with straightforward 1099 income and minimal business expenses.

Asset-Based Qualification

High-net-worth borrowers with substantial assets but complex income may qualify using asset depletion methods:

- Investment accounts, stocks, bonds, and retirement funds

- Real estate equity and rental property values

- Business valuations and ownership interests

Lenders calculate qualifying income by dividing total assets by the loan term (e.g., 360 months for a 30-year mortgage).

Best for: Wealthy self-employed individuals with significant assets but irregular income documentation.

Hybrid Documentation Approaches

Some lenders accept combinations of documentation types:

- 1 year tax returns + 12 months bank statements

- P&L statements + bank statements

- 1099 forms + bank statements

These hybrid approaches may qualify for better rates than pure bank statement programs while maintaining qualification flexibility.

Working with Mortgage Professionals

The Value of Specialized Expertise

Bank statement mortgages require specialized knowledge that general loan officers may lack. Working with professionals experienced in self-employed lending provides:

🎯 Program Knowledge: Understanding which lenders offer the most competitive bank statement programs for your specific situation

📊 Income Calculation Expertise: Maximizing qualifying income through optimal documentation strategies and expense factor applications

⚡ Efficiency: Streamlined processes that avoid common pitfalls and documentation issues that delay closings

💰 Rate Shopping: Access to multiple lenders and programs, ensuring competitive pricing

🛡️ Problem-Solving: Creative solutions when challenges arise during underwriting

Questions to Ask Potential Lenders

When interviewing mortgage professionals about Bank Statement Mortgages for Self-Employed Borrowers: Securing the Best Rates in 2026, ask:

- How many bank statement loans have you closed in the past year?

- What credit score and down payment would qualify me for your best rates?

- Do you use 12-month or 24-month bank statements, and how does this impact pricing?

- What expense factors do you apply to business bank statements?

- Are there prepayment penalties on your bank statement loan programs?

- What reserves do you require after closing?

- How long does your typical bank statement loan take from application to closing?

- What alternative documentation programs do you offer if bank statements don’t work?

Preparing for the Application Process

Successful bank statement mortgage applications require thorough preparation:

Documentation Checklist:

- ✅ 12-24 months of personal and/or business bank statements

- ✅ Business license and formation documents

- ✅ 2 years of business history verification

- ✅ Current profit & loss statement (if available)

- ✅ Credit reports from all three bureaus

- ✅ Asset statements (investment accounts, retirement funds)

- ✅ Property information and purchase contract (if applicable)

- ✅ Explanation letters for any credit issues or unusual deposits

Timeline Expectations:

- Pre-qualification: 1-3 days

- Full application and documentation submission: 3-7 days

- Underwriting review: 7-14 days

- Conditional approval and clearing conditions: 7-14 days

- Final approval and closing: 3-7 days

Total Timeline: 30-45 days from application to closing (longer than conventional mortgages)

Future Outlook for Self-Employed Mortgage Options

Market Trends in 2026

The self-employed mortgage market continues evolving with several positive trends:

Expanding Lender Participation: More traditional banks and credit unions are adding bank statement programs to compete with non-QM specialists, increasing competition and improving rates.

Technology Integration: Automated bank statement analysis tools are streamlining income calculation and reducing underwriting timelines.

Product Innovation: New hybrid documentation programs are emerging that combine the best aspects of various qualification methods.

Regulatory Clarity: Continued refinement of non-QM lending standards is providing greater consistency and borrower protections.

Rate Projections

While predicting exact future rates remains challenging, several factors suggest continued opportunity for self-employed borrowers in 2026:

- Conventional mortgage rates stabilizing in the 6-7% range creates a favorable baseline

- Bank statement loan premiums compressing as lender competition increases

- Economic conditions supporting moderate rate environments

- Increased acceptance of alternative documentation reducing perceived risk premiums

Self-employed borrowers monitoring current interest rate trends can time applications strategically to capture favorable market conditions.

Preparing for Future Applications

Self-employed professionals planning to apply for mortgages in the coming years should:

Establish Clean Banking Patterns Now: Begin using dedicated business accounts and maintaining consistent deposit patterns 24 months before anticipated application dates.

Build Credit Strategically: Work toward credit scores above 700 to qualify for optimal pricing and terms.

Document Business Continuity: Maintain comprehensive records proving 2+ years of self-employment and ongoing business viability.

Accumulate Reserves: Build savings to support 20%+ down payments and 6-12 months of reserve requirements.

Consult Tax Professionals: Balance tax minimization strategies with mortgage qualification considerations, especially in the 1-2 years before home purchase.

Conclusion

Bank Statement Mortgages for Self-Employed Borrowers: Securing the Best Rates in 2026 represents a powerful financing solution for entrepreneurs, freelancers, and business owners who struggle with traditional mortgage qualification. By using 12-24 months of deposit history rather than tax returns, these programs recognize the true earning capacity of self-employed professionals who maximize business deductions.

With current rates in the 7.25-7.375% range[8]—representing manageable premiums over conventional mortgages—and flexible qualification standards accommodating credit scores as low as 620, DTI ratios up to 50%, and diverse property types, bank statement loans open homeownership doors that conventional lending keeps closed.

Success in securing the best rates requires strategic preparation: maintaining clean, consistent bank statement histories; optimizing credit scores above 680; maximizing down payments to 20% or more; and working with experienced mortgage professionals who specialize in self-employed lending. Avoiding common mistakes—incomplete documentation, last-minute financial changes, and inadequate reserves—ensures smooth processing and timely closings.

As the mortgage market continues evolving in 2026, self-employed borrowers have unprecedented access to competitive financing options. Whether you’re a contractor, medical professional, or any other self-employed individual, bank statement mortgages provide a viable path to homeownership and real estate investment.

Next Steps

Ready to explore bank statement mortgage options? Take these actionable steps:

- Review Your Bank Statements: Gather 12-24 months of personal and business bank statements to assess your qualifying income potential

- Check Your Credit: Obtain free credit reports and identify opportunities to improve your score before applying

- Calculate Your Down Payment: Determine how much you can comfortably put down while maintaining adequate reserves

- Research Lenders: Identify 3-5 lenders or mortgage brokers specializing in bank statement programs

- Get Pre-Qualified: Submit preliminary information to assess your qualification and rate expectations

- Prepare Documentation: Organize all required documents to streamline the application process

- Monitor Rate Trends: Stay informed about market conditions to time your application optimally

The path to homeownership as a self-employed borrower may require alternative documentation, but with bank statement mortgages offering competitive rates and flexible qualification in 2026, your entrepreneurial success can translate into real estate ownership. Start preparing today to position yourself for the best possible terms when you’re ready to apply.

References

[1] Bank Statement Loans More Mortgage Options For Self Employed Buyers And Homeowners As Rates Ease – https://www.homelifemtg.com/articles/bank-statement-loans-more-mortgage-options-for-self-employed-buyers-and-homeowners-as-rates-ease

[2] Self Employed Home Loans – https://newfi.com/self-employed-home-loans/

[3] Bank Statement Loan – https://www.nasb.com/lending/solutions/home-loans/bank-statement-loan

[4] Bank Statement Loans – https://crosscountrymortgage.com/mortgage/loans/non-qm/bank-statement-loans/

[5] Bank Statement Loans – https://griffinfunding.com/non-qm-mortgages/bank-statement-loans/

[8] Bank Statement Mortgage – https://www.fidelityhomegroup.com/bank-statement-mortgage/