February 4, 2026

How 2026 Rate Forecasts Could Make Refinancing a Smart Move for Toronto First-Time Buyers

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

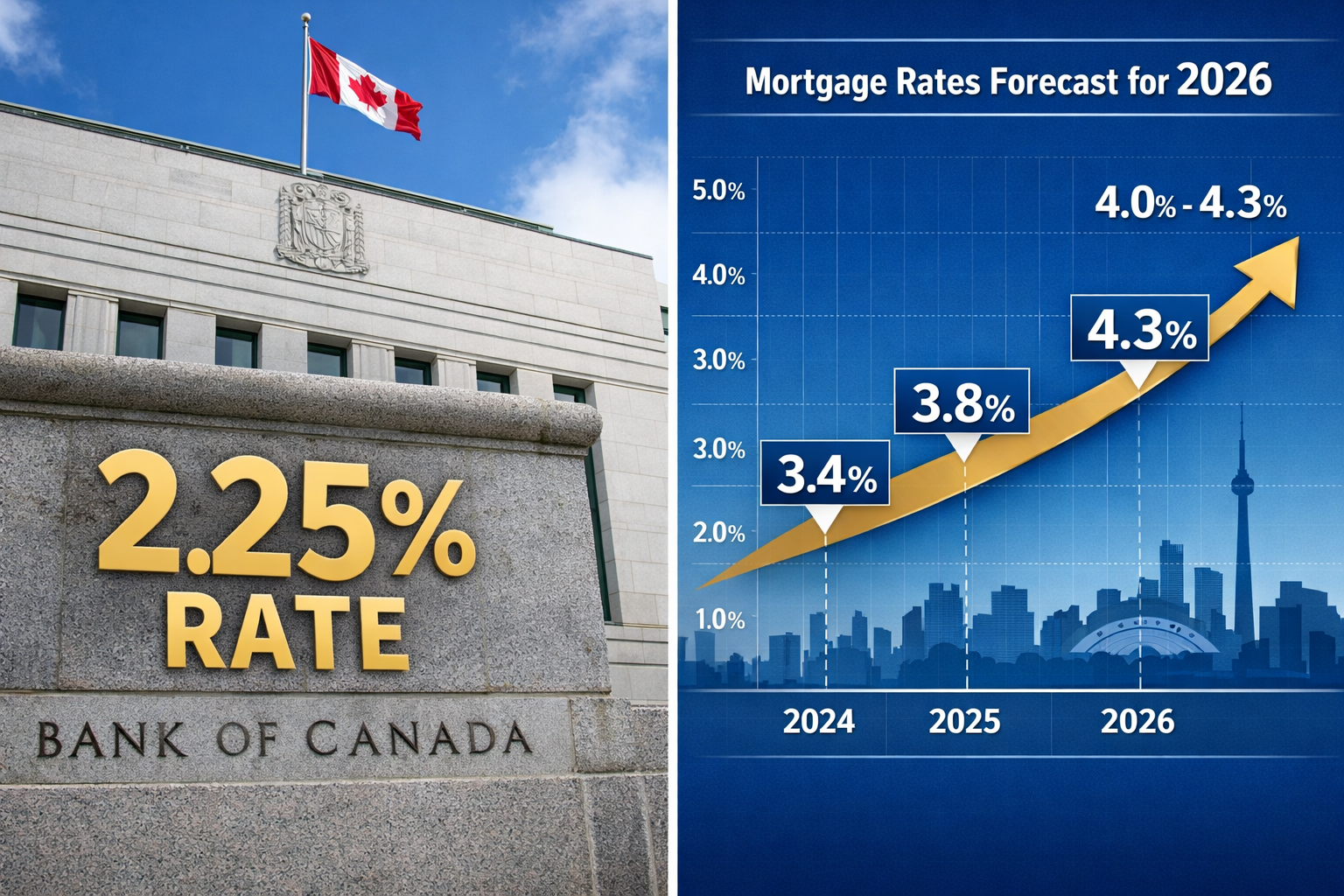

The mortgage landscape in Toronto is shifting, and first-time homebuyers who purchased in recent years may have a unique opportunity on their hands. With the Bank of Canada holding its overnight rate steady at 2.25% and forecasts suggesting relatively stable conditions throughout 2026, understanding how 2026 rate forecasts could make refinancing a smart move for Toronto first-time buyers has never been more important. Whether you’re looking to reduce monthly payments, consolidate high-interest debt, or access your home’s equity, the current rate environment presents strategic opportunities that savvy homeowners shouldn’t overlook.

Key Takeaways

✅ Stable rates expected: The Bank of Canada overnight rate is projected to remain at 2.25% through most of 2026, with fixed rates ranging from 3.7% to 4.3% and variable rates between 3.4% and 4%[1][4]

✅ Refinancing window: First-time buyers who purchased at higher rates in 2022-2023 may save significantly by refinancing to today’s lower rates

✅ Debt consolidation benefits: Refinancing can help consolidate high-interest credit card debt (often 19-22%) into your lower-rate mortgage

✅ Renewal challenges ahead: Approximately 33% of Canadian mortgage holders face higher payments upon renewal in 2026, with fixed-rate renewals seeing increases averaging around 20%[4]

✅ Strategic timing matters: Acting before potential rate increases later in 2026 could lock in predictability and savings for years to come

Understanding the 2026 Interest Rate Landscape

Current Rate Environment in Toronto

As of 2026, Toronto’s mortgage market is experiencing a period of relative stability compared to the volatility of previous years. The Bank of Canada has maintained its overnight rate at 2.25%[4], providing a foundation for mortgage lenders to offer competitive rates to qualified borrowers.

For first-time buyers specifically, the current best rates available include:

| Mortgage Type | Current Rate | Rate Range Expected in 2026 |

|---|---|---|

| 5-Year Fixed (Insured) | 3.89% | 3.7% – 4.3% |

| 5-Year Variable (Insured) | 3.60% | 3.4% – 4.0% |

| 3-Year Fixed | 3.95% – 4.25% | Similar range expected |

These rates represent a significant improvement from the peak rates seen in 2023-2024, when many first-time buyers entered the market at rates exceeding 5-6%.

What the Forecasts Tell Us

Multiple financial institutions and mortgage experts have weighed in on where rates are headed throughout 2026. The consensus suggests modest stability with potential for slight increases toward year-end[1][4].

Key forecast highlights include:

- Fixed mortgage rates are expected to remain in the high-3% to mid-4% range for most of 2026[1]

- Variable rates are forecast to range from 3.4% to 4% throughout the year[1]

- The Bank of Canada rate is expected to hold at 2.25% through much of the year, with potential increases of 0.25% to 0.50% by year-end[1]

- Some major banks predict rates will end 2026 the same as they began, while others expect increases up to 50 basis points (reaching 2.75%)[4]

“The stability we’re seeing in 2026 creates a strategic window for homeowners who purchased at higher rates to reassess their mortgage strategy and potentially save thousands over the life of their loan.”

Factors Influencing Rate Stability

Several economic factors are contributing to the relatively stable rate environment in 2026:

📊 Inflation management: The Bank of Canada’s successful efforts to bring inflation closer to its 2% target have reduced pressure for aggressive rate hikes

🌐 Trade negotiations: Ongoing trade discussions with the United States and other partners are influencing economic policy decisions[1]

🏘️ Housing market dynamics: Toronto’s housing market has found more balance between supply and demand, reducing the urgency for dramatic policy interventions

💼 Employment trends: Stable employment numbers across the Greater Toronto Area are supporting consumer confidence without overheating the economy

Understanding these factors helps first-time buyers recognize that the current rate environment may represent a sweet spot for refinancing before potential increases materialize later in the year.

How 2026 Rate Forecasts Could Make Refinancing a Smart Move for Toronto First-Time Buyers: Key Opportunities

Opportunity #1: Locking in Lower Rates Before Potential Increases

For Toronto first-time buyers who purchased their homes between 2022 and 2024, there’s a strong possibility that your current mortgage rate exceeds what’s available today. If you’re carrying a mortgage at 5% or higher, refinancing your mortgage to a rate in the high-3% range could translate to substantial monthly savings.

Example scenario:

- Original mortgage: $500,000 at 5.5% (25-year amortization)

- Current monthly payment: $3,056

- Refinanced at 3.89%: $2,565 monthly

- Monthly savings: $491

- Annual savings: $5,892

These savings compound over time, and with forecasts suggesting potential rate increases of 0.25% to 0.50% by year-end[1], acting sooner rather than later could lock in these benefits for the duration of your term.

Opportunity #2: Consolidating High-Interest Debt

One of the most powerful applications of how 2026 rate forecasts could make refinancing a smart move for Toronto first-time buyers involves debt consolidation. Many first-time homeowners also carry other debts—credit cards, car loans, personal lines of credit—often at interest rates significantly higher than mortgage rates.

Consider this comparison:

| Debt Type | Typical Interest Rate | Monthly Payment on $20,000 |

|---|---|---|

| Credit Cards | 19.99% | $400+ (minimum payments) |

| Personal Loan | 8-12% | $450-500 |

| Car Loan | 6-8% | $390-420 |

| Mortgage Refinance | 3.89% | $105 (added to mortgage) |

By consolidating $20,000 in high-interest debt into your mortgage through refinancing, you could reduce your total monthly debt payments by $300-400 or more. This improved cash flow can be redirected toward savings, investments, or accelerated mortgage repayment strategies.

Opportunity #3: Accessing Home Equity for Strategic Purposes

Toronto’s real estate market has seen property values appreciate in many neighborhoods, even through recent market corrections. First-time buyers who purchased 2-3 years ago may have accumulated significant equity through:

- Principal paydown through regular mortgage payments

- Property appreciation in their neighborhood

- Home improvements that increased property value

Refinancing allows you to access up to 80% of your home’s current value (minus your outstanding mortgage balance) for purposes such as:

🏗️ Home renovations: Upgrading your property can further increase its value and improve your quality of life

💰 Investment opportunities: Some homeowners use equity to purchase investment properties or contribute to RRSPs

🎓 Education funding: Investing in education or professional development at mortgage rates rather than student loan rates

📈 Emergency fund building: Creating a financial safety net at historically low borrowing costs

The key is using accessed equity strategically rather than for consumable purchases that don’t build long-term value.

Opportunity #4: Switching from Variable to Fixed (or Vice Versa)

The 2026 rate environment presents an interesting dynamic: the spread between fixed and variable rates is relatively narrow, with variable rates currently around 3.60% and fixed rates at 3.89%[1]. This creates strategic options:

For those with variable-rate mortgages:

- If you value payment predictability and believe rates will rise later in 2026, switching to fixed now locks in certainty

- The small premium (approximately 0.29%) may be worth the peace of mind

For those with higher fixed-rate mortgages:

- If your fixed rate is significantly above current offerings, refinancing to a new fixed term makes sense

- Alternatively, switching to variable could provide immediate savings with manageable risk given stable forecasts

Understanding the differences between variable and fixed rates helps inform this decision based on your risk tolerance and financial goals.

Understanding the Refinancing Process for First-Time Buyers

What Refinancing Actually Means

Mortgage refinancing involves replacing your existing mortgage with a new one, potentially with different terms, a different lender, or a different loan amount. This differs from renewal, which simply continues your existing mortgage with the same lender at the end of your term.

When you refinance, you’re essentially:

- Breaking your current mortgage contract (which may involve penalties)

- Applying for a new mortgage with new terms

- Potentially accessing additional funds if you’re borrowing more than your current balance

- Resetting your amortization period (unless you specifically request otherwise)

Calculating the True Cost of Refinancing

Before jumping into refinancing, Toronto first-time buyers need to understand the associated costs:

💵 Prepayment penalties: If you break your mortgage before the term ends, you’ll typically pay the greater of:

- Three months’ interest, OR

- The Interest Rate Differential (IRD)—the difference between your current rate and the rate the lender can charge for the remaining term

📋 Legal fees: Refinancing requires legal documentation, typically costing $800-1,500

🏠 Appraisal fees: Lenders often require a current property appraisal ($300-500)

📄 Administration fees: Various lender fees may apply ($200-400)

Total estimated costs: $2,000-5,000+ depending on your situation

To determine if refinancing makes financial sense, calculate your break-even point:

Break-even months = Total refinancing costs ÷ Monthly savings

If you’re saving $400 per month and costs total $3,000, you’ll break even in 7.5 months. If you plan to stay in your home longer than that, refinancing likely makes sense.

Qualification Requirements in 2026

Even if you qualified for your original mortgage, refinancing requires re-qualifying under current lending standards. Toronto first-time buyers should be prepared to demonstrate:

✔️ Stable income: Employment verification and income documentation (pay stubs, tax returns, etc.)

✔️ Good credit score: Ideally 680+ for best rates; 600+ minimum for many lenders

✔️ Manageable debt ratios:

- Gross Debt Service (GDS) ratio under 39%

- Total Debt Service (TDS) ratio under 44%

✔️ Sufficient equity: At least 20% equity in your home to avoid CMHC insurance on the refinanced amount

✔️ Stress test compliance: You must qualify at either your contract rate plus 2% or 5.25%, whichever is higher

The mortgage stress test requirements ensure you can afford payments even if rates increase, protecting both you and the lender.

Working with the Right Mortgage Professional

Navigating how 2026 rate forecasts could make refinancing a smart move for Toronto first-time buyers is considerably easier with expert guidance. A qualified mortgage broker can:

- Compare rates from multiple lenders to find your best option

- Calculate break-even points and long-term savings scenarios

- Navigate qualification requirements and documentation

- Negotiate terms on your behalf with lenders

- Explain options for accessing equity or consolidating debt

Unlike going directly to a bank, mortgage brokers have access to numerous lenders and can often secure better rates and terms, especially for first-time buyers who may have unique circumstances.

Strategic Considerations: Is Refinancing Right for You?

When Refinancing Makes Strong Financial Sense

Refinancing is particularly advantageous for Toronto first-time buyers in these situations:

🎯 Scenario 1: Significant rate reduction available If you can reduce your rate by 0.75% or more, the savings typically outweigh the costs quickly, especially on larger mortgage balances.

🎯 Scenario 2: High-interest debt consolidation When you’re carrying credit card balances, personal loans, or other high-interest debt, consolidating into your mortgage can dramatically reduce your total interest costs and simplify your finances.

🎯 Scenario 3: Need to access equity If you have a legitimate need for funds (renovations, education, investment) and your home has appreciated, accessing equity at mortgage rates is typically cheaper than other borrowing options.

🎯 Scenario 4: Approaching renewal anyway If your mortgage term is ending within 3-6 months, you can often refinance without significant penalties, making this an ideal time to reassess your mortgage strategy.

🎯 Scenario 5: Income has increased If your financial situation has improved since your original purchase, you may qualify for better rates or more favorable terms than were available initially.

When to Think Twice About Refinancing

Conversely, refinancing may not be the best move if:

❌ You’re planning to sell soon: If you’ll sell within 1-2 years, you may not recoup refinancing costs

❌ Your penalty is prohibitive: Some mortgages have very high IRD penalties that make early refinancing uneconomical

❌ You have little equity: If you have less than 20% equity, refinancing may require additional CMHC insurance

❌ Your credit has deteriorated: If your credit score has dropped significantly, you may not qualify for better rates

❌ You’re close to mortgage-free: If you have only a few years remaining, refinancing could extend your debt unnecessarily

Alternative Options to Consider

Before committing to a full refinance, Toronto first-time buyers should also consider:

🏦 Home Equity Line of Credit (HELOC): A HELOC provides flexible access to equity without refinancing your entire mortgage. You only pay interest on what you borrow, and rates, while higher than mortgage rates, are lower than credit cards.

💳 Second mortgage: A second mortgage allows you to borrow against your equity while keeping your existing first mortgage intact, avoiding prepayment penalties.

🔄 Mortgage switch at renewal: If your term is ending soon, you can switch lenders at renewal without penalties and potentially negotiate better terms.

⚡ Accelerated payments: Instead of refinancing, you might achieve similar long-term savings by increasing your payment frequency or making lump-sum prepayments within your existing mortgage’s allowances.

Each option has distinct advantages depending on your specific situation and goals.

Preparing for Renewal: What Toronto First-Time Buyers Need to Know

The 2026 Renewal Wave

One of the most significant factors making 2026 a critical year for mortgage strategy is the renewal wave hitting Canadian homeowners. Approximately 33% of Canadian mortgage holders are expected to face higher monthly payments upon renewal in 2026[4], with about 75% of those facing increases holding 5-year fixed-rate mortgages[4].

For Toronto first-time buyers who purchased in 2021 with 5-year fixed terms, 2026 represents your renewal year. The challenge? Many of these mortgages were secured at rates between 1.5% and 2.5%—significantly lower than today’s rates.

Expected Payment Increases at Renewal

The data is sobering: fixed-rate mortgage renewals are expected to see payment increases averaging around 20%[4]. For a first-time buyer with a $500,000 mortgage, this could mean:

- Original payment at 2% rate: $2,118/month

- Renewal payment at 4% rate: $2,541/month

- Increase: $423/month or $5,076/year

This represents a significant hit to household budgets, particularly for first-time buyers who may already be stretched thin.

Proactive Refinancing vs. Reactive Renewal

This is where understanding how 2026 rate forecasts could make refinancing a smart move for Toronto first-time buyers becomes crucial. Rather than waiting for renewal and accepting whatever rate your lender offers, proactive refinancing allows you to:

✅ Shop the market for the best available rates across all lenders

✅ Lock in rates early before potential increases later in 2026

✅ Restructure your mortgage to better suit your current financial situation

✅ Negotiate from a position of strength rather than necessity

✅ Access equity if needed while refinancing anyway

The best time to address your mortgage renewal is typically 4-6 months before your term ends, giving you time to explore options without pressure.

Strategies to Manage Renewal Payment Shock

If you’re facing renewal in 2026 and concerned about payment increases, consider these strategies:

📅 Extend your amortization: If you have more than 25 years remaining, extending to 30 years (for those who qualify under new amortization rules) can reduce monthly payments, though you’ll pay more interest long-term.

🔀 Switch to variable: If forecasts suggest stable or declining rates, variable-rate mortgages currently offer lower rates than fixed, potentially softening the renewal shock.

💰 Make lump-sum payments: If you have savings, making a significant principal payment before renewal reduces your balance and therefore your new payment amount.

🏠 Refinance before renewal: As discussed, refinancing 3-6 months before renewal lets you avoid penalties while securing competitive rates.

📊 Budget adjustments: Start adjusting your budget now to accommodate higher payments, building the difference into savings so the transition is less jarring.

Taking Action: Your Refinancing Roadmap

Step 1: Assess Your Current Mortgage Situation

Begin by gathering complete information about your existing mortgage:

- Current interest rate and type (fixed/variable)

- Remaining balance and amortization period

- Renewal date and remaining term

- Prepayment penalty calculation

- Prepayment privileges (lump sum allowances, payment increase options)

Your lender can provide a mortgage statement with most of this information. Understanding your starting point is essential for evaluating refinancing options.

Step 2: Calculate Your Home’s Current Value and Equity

Toronto’s real estate market has experienced fluctuations, so your home’s current value may differ from your purchase price. Research:

- Recent comparable sales in your neighborhood

- Current market conditions in your area

- Any improvements you’ve made that add value

Your equity equals your home’s current value minus your outstanding mortgage balance. Remember, you can typically access up to 80% of your home’s value through refinancing.

Step 3: Review Your Financial Goals and Needs

Clarify what you want to achieve through refinancing:

- Lower monthly payments?

- Debt consolidation?

- Access to equity for specific purposes?

- Rate type change (fixed to variable or vice versa)?

- Payment predictability?

Having clear objectives helps you evaluate whether refinancing aligns with your broader financial strategy.

Step 4: Shop Rates and Compare Options

Don’t accept the first offer you receive. Compare rates from:

- Your current lender

- Major banks

- Credit unions

- Alternative lenders

- Mortgage brokers (who can access multiple lenders)

Even a 0.1% difference in rate can mean thousands of dollars over your mortgage term. Use a mortgage rates calculator to compare scenarios.

Step 5: Calculate Total Costs and Break-Even Point

Once you have rate quotes, calculate:

- Prepayment penalty on your current mortgage

- All refinancing fees (legal, appraisal, administration)

- Monthly savings with the new mortgage

- Break-even timeline (costs ÷ monthly savings)

- Long-term savings over the full term

This analysis reveals whether refinancing makes financial sense for your situation.

Step 6: Get Pre-Approved for Refinancing

Just as with your original purchase, getting pre-approved for refinancing:

- Confirms you qualify at desired rates

- Locks in rates for 90-120 days

- Strengthens your negotiating position

- Identifies any qualification issues early

Gather required documentation: recent pay stubs, tax returns, credit reports, and property tax statements.

Step 7: Time Your Refinance Strategically

Given the 2026 rate forecasts suggesting stability through mid-year with potential increases later[1][4], timing matters:

🌅 Early to mid-2026: Optimal window to lock in current rates before potential year-end increases

🍂 Late 2026: May face higher rates if Bank of Canada increases as some forecasts suggest

📅 4-6 months before renewal: Ideal timing to avoid penalties while securing new rates

Monitor current mortgage news and forecasts to stay informed about market conditions.

Step 8: Complete the Refinancing Process

Once you’ve decided to proceed:

- Submit your application with all required documentation

- Complete the appraisal when scheduled by your lender

- Review and sign all legal documents with your lawyer

- Pay closing costs (often deducted from refinanced funds)

- Confirm your new payment schedule and terms

The entire process typically takes 2-4 weeks from application to completion.

Common Mistakes to Avoid When Refinancing

Mistake #1: Focusing Only on Rate

While rate is important, it’s not the only factor. Consider:

- Prepayment privileges: Can you make extra payments without penalty?

- Portability: Can you transfer the mortgage if you move?

- Terms and conditions: Are there restrictions that limit flexibility?

- Lender reputation: Will you receive good service throughout your term?

A slightly higher rate with excellent prepayment privileges might save you more long-term than the lowest rate with restrictive terms.

Mistake #2: Extending Amortization Without Purpose

Refinancing often resets your amortization to 25 or 30 years. While this lowers payments, it dramatically increases total interest paid. If you’ve already paid down your mortgage for several years, extending amortization means:

- More years in debt

- Significantly more interest paid over the life of the mortgage

- Slower equity building

Unless you specifically need lower payments, maintain or reduce your remaining amortization period.

Mistake #3: Using Equity for Consumable Purchases

Accessing equity is a powerful tool, but using it for vacations, vehicles that depreciate, or everyday expenses is financially dangerous. These purchases don’t build wealth and you’ll be paying them off for decades at mortgage rates.

Appropriate uses for accessed equity include:

- Home improvements that increase property value

- Education that increases earning potential

- Investment opportunities with returns exceeding mortgage costs

- Consolidating high-interest debt (with a plan to avoid re-accumulating it)

Mistake #4: Ignoring the Penalty Calculation

Many homeowners are shocked by prepayment penalties, particularly IRD calculations on fixed-rate mortgages. Before committing to refinance:

- Request a penalty quote in writing from your current lender

- Understand whether you’ll pay three months’ interest or IRD

- Factor this cost into your break-even calculation

- Consider whether waiting until closer to renewal might be wiser

Mistake #5: Not Considering Alternative Solutions

Refinancing isn’t always the best answer. Before proceeding, explore whether:

- A HELOC might serve your needs with more flexibility

- Switching lenders at renewal would achieve similar results without penalties

- Accelerated payments within your current mortgage could accomplish your goals

- Debt consolidation through other means might be more cost-effective

Each situation is unique, and a comprehensive analysis reveals the truly optimal path forward.

The Bigger Picture: Building Long-Term Wealth Through Smart Mortgage Management

Refinancing as Part of Your Overall Financial Strategy

Understanding how 2026 rate forecasts could make refinancing a smart move for Toronto first-time buyers is just one piece of a comprehensive financial plan. Your mortgage should align with broader goals:

🏡 Home equity building: Your home is likely your largest asset; strategic mortgage management accelerates equity growth

💼 Cash flow optimization: Lower mortgage payments free up cash for investments, retirement savings, or emergency funds

📈 Debt reduction: Consolidating high-interest debt into your mortgage is only valuable if you avoid accumulating new high-interest debt

🎯 Financial flexibility: The right mortgage structure provides options when life circumstances change

🛡️ Risk management: Balancing rate savings with payment predictability protects against future financial stress

Beyond Refinancing: Other Wealth-Building Strategies

Once you’ve optimized your mortgage through refinancing, consider these complementary strategies:

⚡ Accelerated payment schedules: Switching from monthly to bi-weekly payments or increasing payment amounts can save tens of thousands in interest

💰 Lump-sum contributions: Using bonuses, tax refunds, or windfalls to make annual lump-sum payments dramatically reduces amortization

🏠 Strategic renovations: Investing in high-ROI improvements (kitchens, bathrooms, energy efficiency) builds equity faster than market appreciation alone

📊 Investment diversification: Once high-interest debt is eliminated and mortgage is optimized, building investment portfolios creates additional wealth streams

🎓 Continuous financial education: Staying informed about market trends and opportunities positions you to make smart decisions

Monitoring Market Conditions Throughout 2026

The mortgage market is dynamic, and conditions can shift. Throughout 2026, stay informed by:

- Following Bank of Canada announcements about overnight rate decisions

- Monitoring economic indicators like inflation, employment, and GDP growth

- Reading market forecasts from reputable sources and mortgage professionals

- Reviewing your mortgage at least annually to ensure it still serves your goals

- Maintaining relationships with mortgage professionals who can alert you to opportunities

The homeowners who build the most wealth are those who actively manage their mortgages rather than “set and forget” them.

Conclusion: Making Your Move in 2026

The convergence of stable Bank of Canada rates at 2.25%, competitive mortgage rates in the high-3% to mid-4% range, and forecasts suggesting potential increases later in the year creates a strategic window for Toronto first-time buyers to reassess their mortgage situation. Understanding how 2026 rate forecasts could make refinancing a smart move for Toronto first-time buyers empowers you to take control of your financial future.

Whether your goal is to reduce monthly payments, consolidate expensive debt, access equity for strategic purposes, or simply lock in predictability before potential rate increases, refinancing may offer significant benefits—if the numbers work for your specific situation.

Your Next Steps

Ready to explore whether refinancing makes sense for you? Take these concrete actions:

1. Request a penalty quote from your current lender to understand break costs

2. Calculate your home equity by researching current property values in your neighborhood

3. Gather financial documentation including recent pay stubs, tax returns, and credit reports

4. Compare current rates from multiple lenders or work with a mortgage broker to access the best options

5. Run the numbers using mortgage calculators to determine monthly savings and break-even points

6. Consult with a mortgage professional to discuss your specific situation and explore customized solutions

7. Make an informed decision based on comprehensive analysis rather than emotion or assumptions

The mortgage market in 2026 offers opportunities, but only for those who take proactive steps to evaluate their options. Don’t wait until renewal forces your hand—explore whether refinancing could save you thousands and position you for greater financial success.

Your home is more than just a place to live; it’s a cornerstone of your financial foundation. By strategically managing your mortgage through refinancing when conditions favor it, you’re not just reducing payments—you’re building wealth, creating flexibility, and securing your financial future.

The question isn’t whether refinancing is universally good or bad; it’s whether refinancing is right for your unique situation in 2026. Armed with the insights in this guide, you’re now equipped to make that determination and take action accordingly.

References

[1] Mortgage Rate Forecast For 2026 – https://www.frankmortgage.com/mortgage-rate-forecast-for-2026

[2] Mortgage Report – https://rates.ca/mortgage-report

[3] Mortgage Interest Rate Forecast – https://www.mortgagesandbox.com/mortgage-interest-rate-forecast

[4] Mortgage Rates Forecast Canada – https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/

[5] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast

[6] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast