March 16, 2026

Navigating 26% Renewal Shocks for Self-Employed Toronto Entrepreneurs: Variable Rate Switches to Dodge $500+ Monthly Hits in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

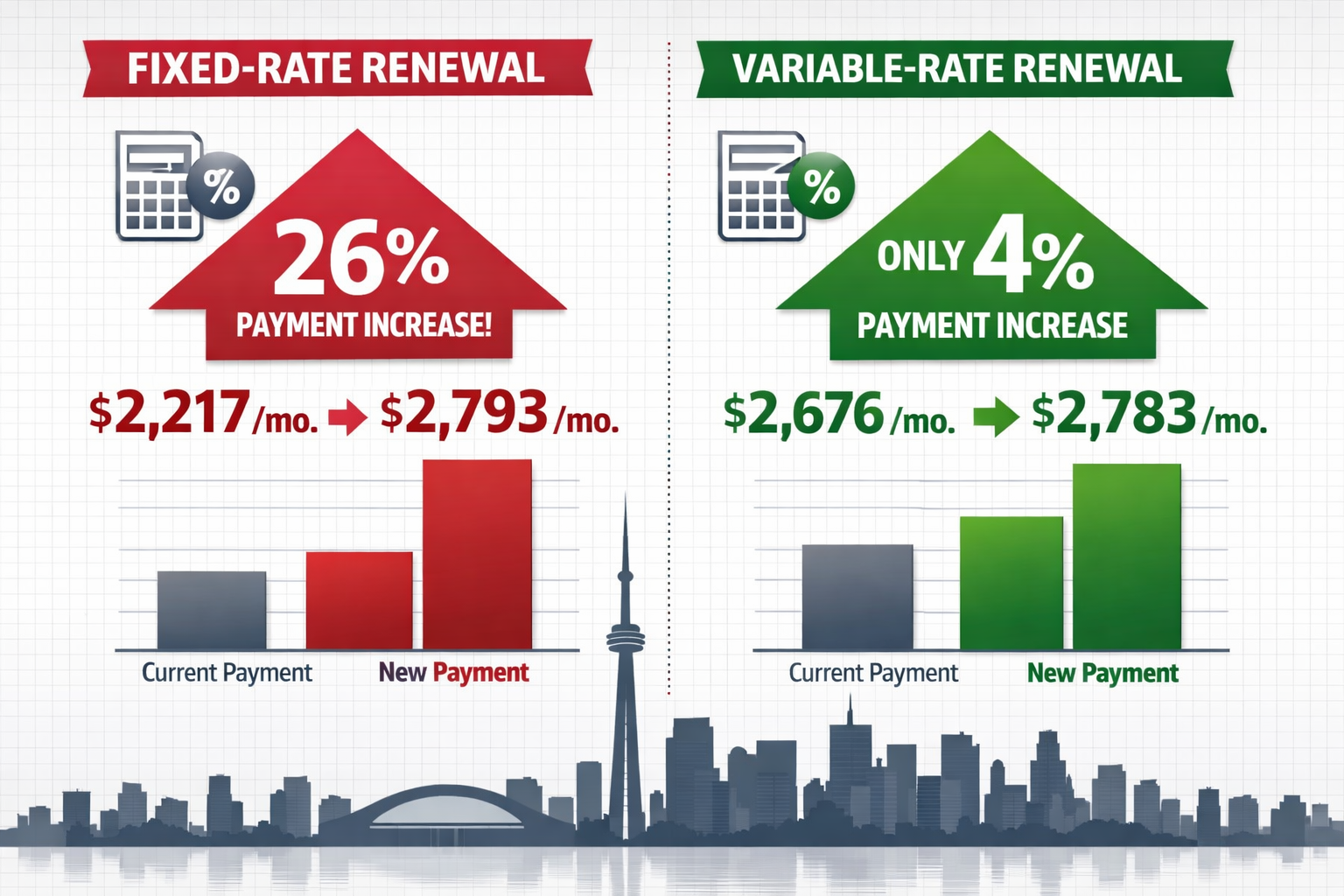

The mortgage renewal landscape in 2026 presents a stark reality for Toronto’s self-employed community: 1.15 million Canadian mortgage holders are facing renewal this year, and those locked into fixed rates from 2021’s historic lows are staring down payment increases of up to 26%. For self-employed entrepreneurs managing fluctuating incomes, this translates to an additional $576 per month or nearly $7,000 annually—a financial shock that could destabilize carefully balanced business budgets.

However, there’s a strategic lifeline that many self-employed borrowers are overlooking. While fixed-rate renewals are triggering these dramatic payment jumps, navigating 26% renewal shocks for self-employed Toronto entrepreneurs through variable rate switches to dodge $500+ monthly hits in 2026 has become not just viable, but potentially the smartest financial move available. Variable-rate borrowers renewing this year face only a 4% payment increase—a mere $107 monthly difference compared to their fixed-rate counterparts.

This comprehensive guide reveals how Toronto’s self-employed professionals—from contractors and freelancers to doctors and business owners—can strategically pivot to variable rates, leverage their unique financial profiles, and potentially save thousands while maintaining payment predictability.

Key Takeaways

- 💰 Fixed-rate renewals in 2026 trigger 26% payment increases ($576/month more), while variable rates show only 4% increases ($107/month)

- 📊 Variable rates currently sit at 3.60% for insured mortgages, significantly below fixed rates and expected to remain competitive throughout 2026

- 🏢 Self-employed borrowers have unique advantages when switching lenders at renewal, including access to specialized programs and alternative documentation methods

- ⏰ The 120-day advance renewal window provides critical time for self-employed entrepreneurs to shop rates and prepare documentation

- 🎯 Strategic timing and lender selection can help self-employed borrowers secure variable rates that minimize payment shock while maintaining financial flexibility

Understanding the 2026 Renewal Crisis: Why Self-Employed Borrowers Face Unique Challenges

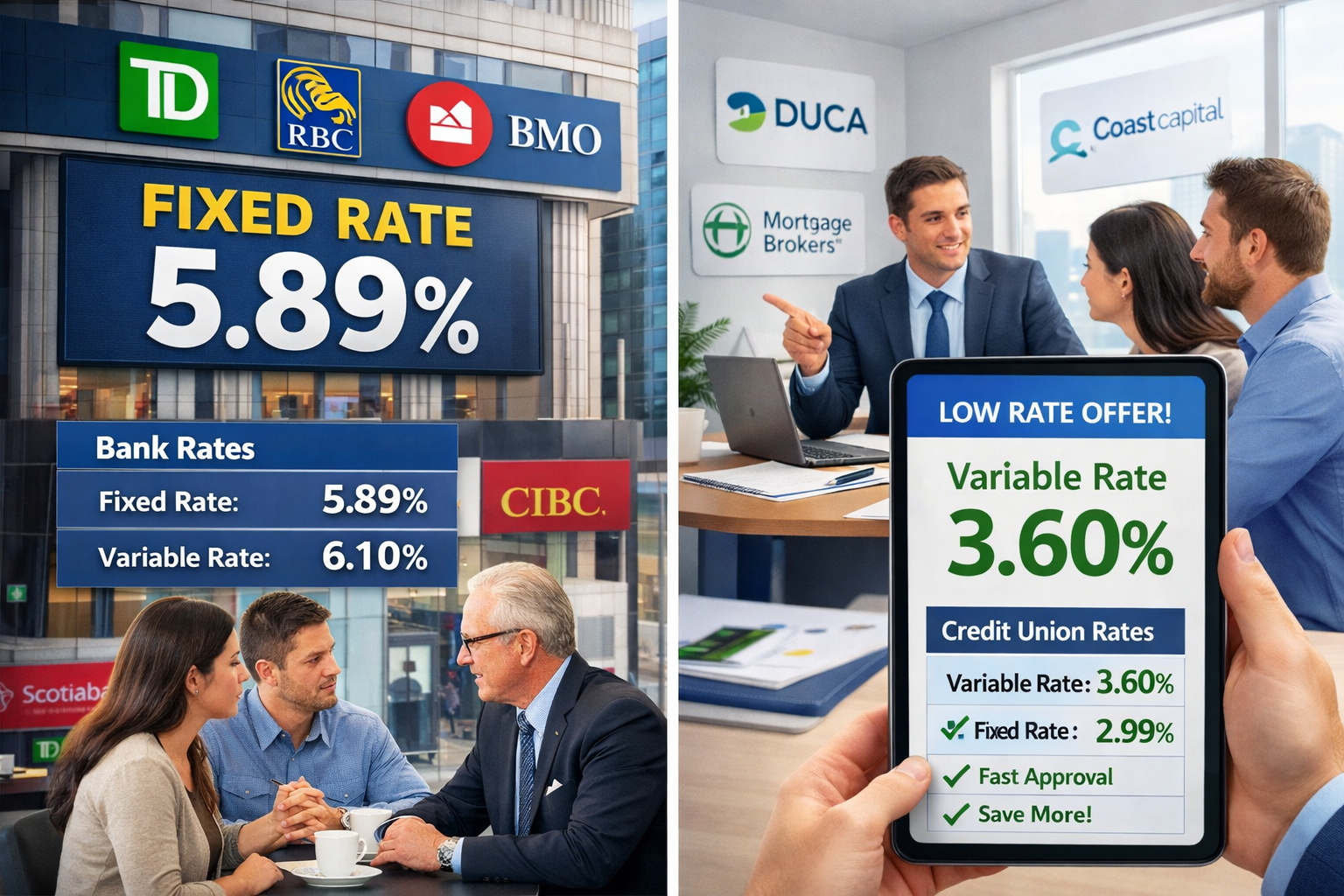

The mortgage renewal crisis of 2026 stems from a perfect storm of circumstances. Between 2020 and 2021, hundreds of thousands of Canadians locked into five-year fixed mortgages at rates between 1.39% and 2.19%—the lowest in Canadian history. Now, as these terms expire, borrowers are confronting renewal rates between 4.89% and 5.89% for fixed products.

The Mathematics of Payment Shock

For a typical Toronto home purchase of $607,280 with 10% down (creating a mortgage of approximately $546,552), the numbers are sobering:

| Scenario | Original Rate | Renewal Rate | Original Payment | New Payment | Monthly Increase | Annual Impact |

|---|---|---|---|---|---|---|

| Fixed-to-Fixed | 1.89% | 5.89% | $2,217 | $2,793 | +$576 | +$6,912 |

| Variable-to-Variable | 4.25% | 4.45% | $2,676 | $2,783 | +$107 | +$1,284 |

This $469 monthly difference between renewal strategies represents the core opportunity for self-employed entrepreneurs navigating 26% renewal shocks for self-employed Toronto entrepreneurs through variable rate switches to dodge $500+ monthly hits in 2026.

Why Self-Employed Borrowers Face Additional Hurdles

Self-employed individuals encounter compounded challenges during renewal:

- Income verification complexity: Traditional lenders require two years of Notice of Assessments (NOAs) and may average income, potentially understating current earning capacity

- Business write-offs impact: Legitimate tax deductions that reduce taxable income also reduce qualifying income for mortgage purposes

- Debt service ratio scrutiny: Lenders apply stricter Total Debt Service (TDS) and Gross Debt Service (GDS) calculations for self-employed applicants

- Documentation burden: Renewal switches to new lenders require full re-qualification, unlike simple renewals with existing lenders

Understanding these unique obstacles is the first step toward developing a strategic approach to mortgage refinancing and switching lenders at renewal.

The Variable Rate Advantage in 2026

The Bank of Canada’s current overnight rate sits at 2.25%, down from the peak of 5.00% in 2023. Economists project this rate will hold steady throughout most of 2026, with inflation expected to remain near the target 2% level. This stability creates an unprecedented opportunity for variable-rate mortgages.

Current best variable mortgage rates for self-employed borrowers in Toronto include:

- Insured mortgages: 3.60% (prime minus 1.15%)

- Conventional mortgages: 3.85% to 4.10%

- Alternative lender programs: 4.25% to 4.75%

These rates remain substantially below fixed alternatives, and with the Bank of Canada unlikely to raise rates significantly until early 2027 at the earliest, the risk-reward calculation favors variable products for strategic borrowers.

Strategic Documentation: Preparing Your Self-Employed Profile for Variable Rate Approval

Successfully navigating 26% renewal shocks for self-employed Toronto entrepreneurs through variable rate switches requires meticulous preparation. Unlike salaried employees who can provide simple pay stubs and T4s, self-employed borrowers must construct a comprehensive financial narrative.

Essential Documentation Package

Core Income Verification:

- ✅ Two years of complete T1 Generals (personal tax returns with all schedules)

- ✅ Two years of Notice of Assessments (NOAs) from CRA

- ✅ Business financial statements (if incorporated: T2 returns, corporate NOAs)

- ✅ Year-to-date profit and loss statement (current year performance)

- ✅ Business bank statements (3-6 months demonstrating cash flow)

Supporting Documentation:

- ✅ Articles of incorporation or business registration

- ✅ GST/HST returns (demonstrates business legitimacy)

- ✅ Contracts or invoices (particularly for contractors showing ongoing work)

- ✅ Professional licenses (for doctors, lawyers, engineers, etc.)

- ✅ Credit bureau report (ensure accuracy before lender pulls)

Income Calculation Strategies for Self-Employed Borrowers

Traditional lenders typically use a two-year average of Line 150 (total income) from your T1 General. However, strategic approaches can maximize your qualifying income:

Add-Back Method: Some lenders allow adding back legitimate business expenses that don’t reflect actual cash outflow:

- Depreciation (CCA)

- Non-cash expenses

- One-time business investments

- Interest and financing charges

Stated Income Programs: For established businesses with strong credit (typically 680+ credit score), some alternative lenders offer stated income programs requiring:

- Minimum 2 years in business

- Down payment of 20%+ (no CMHC insurance)

- Higher interest rates (typically 0.50% to 1.00% premium)

Professional Programs: Self-employed doctors, dentists, and lawyers may access specialized programs through self-employed mortgage programs for professionals that recognize earning potential over tax returns.

Debt Service Ratio Optimization

Lenders assess two critical ratios:

Gross Debt Service (GDS): Should not exceed 39% of gross income

- Formula: (Mortgage payment + Property taxes + Heating + 50% of condo fees) ÷ Gross monthly income

Total Debt Service (TDS): Should not exceed 44% of gross income

- Formula: (GDS + All other debt payments) ÷ Gross monthly income

Strategic optimization tactics:

- 💳 Pay down high-interest revolving credit before renewal

- 🚗 Consider consolidating car loans or lines of credit

- 📱 Reduce monthly obligations (subscriptions, financing agreements)

- 💰 Increase down payment if accessing home equity

For self-employed borrowers, every percentage point improvement in these ratios can mean the difference between approval and denial, or between standard and premium pricing.

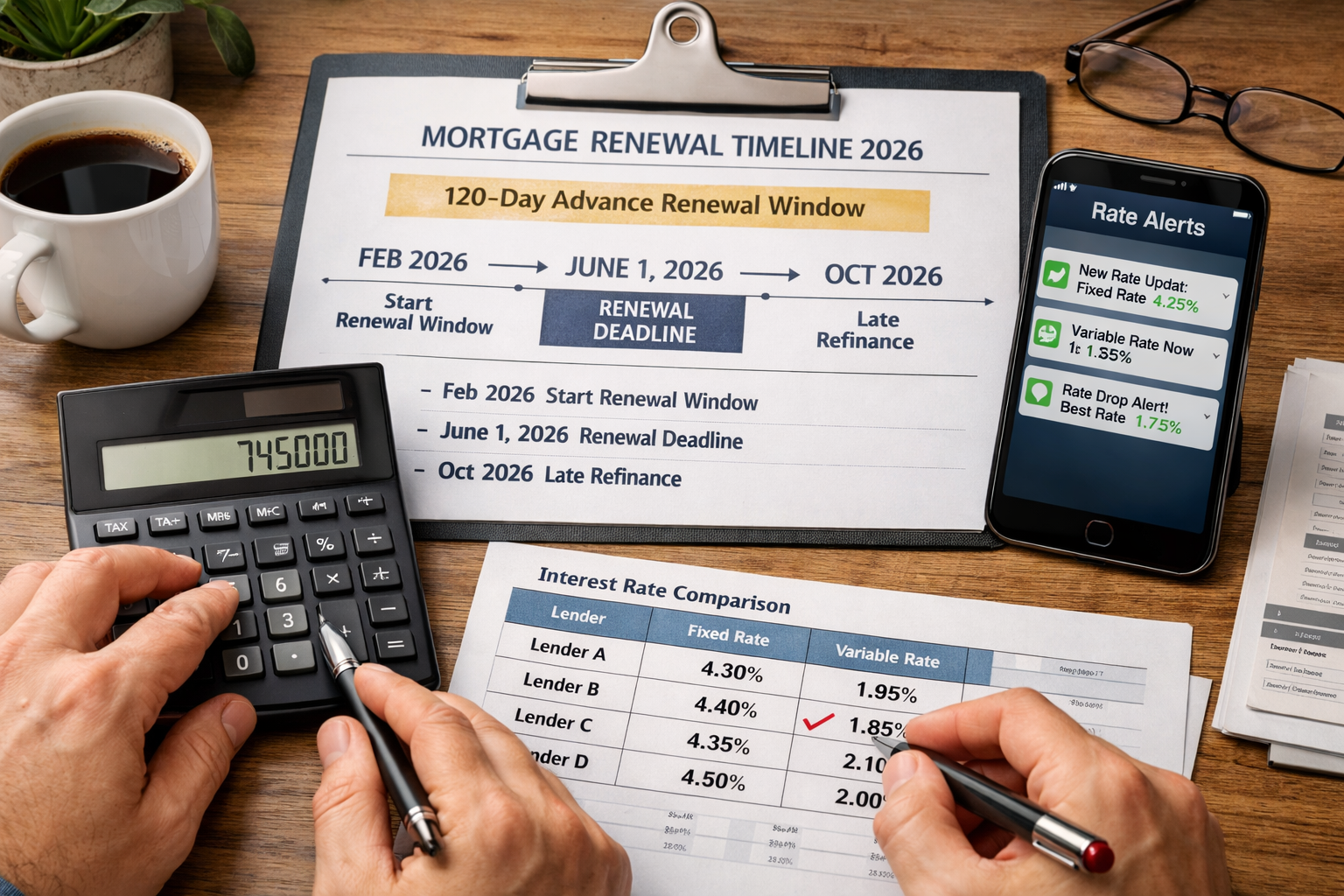

The 120-Day Advantage Window

Most lenders allow borrowers to lock in renewal rates 120 days before maturity. For self-employed entrepreneurs, this window is critical:

Months 4-3 before renewal:

- Gather all documentation

- Review credit reports and address any issues

- Calculate current debt service ratios

- Research current self-employed mortgage rates in Toronto

Months 2-1 before renewal:

- Consult with mortgage broker specializing in self-employed lending

- Submit applications to 2-3 lenders simultaneously

- Compare offers including rates, terms, and features

- Negotiate rate holds and terms

Final month:

- Finalize lender selection

- Complete underwriting requirements

- Arrange for discharge from current lender (if switching)

- Sign renewal documents

This structured approach ensures you’re not scrambling at the last minute, which often results in accepting unfavorable terms.

Lender Landscape: Where Self-Employed Toronto Entrepreneurs Find the Best Variable Rates

Not all lenders treat self-employed borrowers equally. Understanding the lending landscape is crucial for navigating 26% renewal shocks for self-employed Toronto entrepreneurs through variable rate switches to dodge $500+ monthly hits in 2026.

Big Five Banks: Traditional but Restrictive

Pros:

- Established relationships may facilitate renewals

- Competitive rates for straightforward applications

- Full-service banking integration

- Potential for rate negotiation with existing clients

Cons:

- Rigid income verification requirements

- Two-year income averaging without flexibility

- Limited add-back allowances

- Higher rejection rates for complex self-employed situations

Best for: Self-employed borrowers with consistent, well-documented income over 2+ years and minimal business write-offs.

Credit Unions: Relationship-Based Lending

Pros:

- More flexible underwriting approaches

- Relationship banking can influence decisions

- Competitive variable rates (often within 0.10% of big banks)

- Local decision-making authority

Cons:

- Membership requirements

- Smaller lending limits in some cases

- Variable service quality across institutions

Best for: Self-employed borrowers with established local business presence and community ties.

Monoline Lenders: Specialized Mortgage Focus

Pros:

- Mortgage-only focus means specialized expertise

- Often most competitive rates (currently offering 3.60% variables)

- Flexible income calculation methods

- Streamlined approval processes

Cons:

- No banking relationship benefits

- May require mortgage broker access

- Limited branch network

Best for: Rate-sensitive self-employed borrowers with solid documentation seeking the best fixed and variable options.

Alternative Lenders: Solutions for Complex Situations

Pros:

- Stated income programs available

- Flexible documentation requirements

- Approval for situations big banks decline

- Fast turnaround times

Cons:

- Higher rates (typically 4.25% to 5.50% for variables)

- Additional fees may apply

- Shorter terms (often 1-2 years)

Best for: Self-employed borrowers with strong equity position but complex income documentation, or those needing B-lender mortgage solutions.

The Mortgage Broker Advantage

For self-employed borrowers, working with a specialized mortgage broker provides significant advantages:

🎯 Access to multiple lenders: Brokers submit to 10-20+ lenders simultaneously 📊 Program expertise: Knowledge of which lenders accept specific self-employed situations 💰 Rate negotiation: Leverage relationships to secure better pricing ⏱️ Time savings: One application instead of multiple bank visits 🔒 Confidentiality: Credit inquiries consolidated to minimize score impact

Mortgage brokers specializing in self-employed mortgages for contractors understand the nuances of income calculation and can position applications for optimal approval odds.

Rate Comparison Strategy

When evaluating variable rate offers, compare beyond the headline rate:

Total Cost Analysis:

- Posted variable rate

- Discount from prime (e.g., Prime – 1.15%)

- Lender fees and administration charges

- Appraisal and legal costs (if switching lenders)

- Prepayment privileges (annual lump sum, payment increase options)

- Portability features

- Conversion options (ability to lock into fixed)

Example Comparison:

| Lender Type | Variable Rate | Discount Structure | Annual Fees | Prepayment | Total 5-Year Cost* |

|---|---|---|---|---|---|

| Big Bank | 4.10% | Prime – 0.65% | $0 | 20/20 | $135,280 |

| Monoline | 3.60% | Prime – 1.15% | $0 | 20/20 | $121,450 |

| Credit Union | 3.85% | Prime – 0.90% | $150/year | 15/15 | $129,890 |

| Alternative | 4.45% | Prime – 0.30% | $495/year | 10/10 | $144,820 |

*Based on $500,000 mortgage, 25-year amortization, assuming prime remains at 4.75%

The monoline lender saves $13,830 over five years compared to the big bank, and $23,370 compared to the alternative lender—demonstrating why rate shopping is essential.

Execution Strategy: Making the Variable Rate Switch Work for Your Business Cash Flow

Successfully navigating 26% renewal shocks for self-employed Toronto entrepreneurs through variable rate switches requires more than just securing a good rate—it demands strategic execution aligned with your business cash flow patterns.

Timing Your Switch for Maximum Benefit

Seasonal Business Considerations:

For self-employed entrepreneurs with seasonal income patterns (contractors, landscapers, event planners, etc.), timing your renewal can optimize cash flow:

- 🌱 Spring/Summer earners: Renew in fall when cash reserves are highest

- ❄️ Winter earners: Renew in spring to align with peak earning season

- 📅 Year-round stability: Prioritize rate over timing

Tax Year Optimization:

If your most recent tax year shows significantly higher income than the previous year, consider:

- Waiting until after filing current year taxes (April deadline)

- Requesting lenders use most recent year if substantially higher

- Providing year-to-date financials demonstrating continued growth

Payment Structure Strategies

Variable rate mortgages offer flexibility that self-employed borrowers can leverage:

Accelerated Payment Options:

- Bi-weekly accelerated: Makes equivalent of one extra monthly payment annually

- Weekly accelerated: Further reduces interest, improves cash flow management

- Monthly: Simplest for business accounting integration

Strategic Prepayment Utilization:

Most variable mortgages allow 20% annual lump sum prepayments. Self-employed borrowers should:

✅ Make lump sum payments during high-revenue months ✅ Increase regular payments by 20% when business cash flow allows ✅ Use tax refunds or business windfalls for principal reduction ✅ Maintain emergency fund before aggressive prepayment

Example Cash Flow Strategy:

Scenario: Freelance consultant earning $180,000 annually with 60% revenue concentration in Q1-Q2

- January-June: Maintain minimum mortgage payments, accumulate reserves

- July: Make 10% lump sum payment ($50,000 mortgage = $5,000 prepayment)

- August-December: Increase regular payment by 10%

- December: Assess year-end cash position for additional prepayment

This approach reduces interest costs while maintaining flexibility during slower business periods.

Risk Management for Variable Rate Borrowers

While variable rates offer significant savings in 2026, prudent self-employed borrowers implement protective strategies:

Rate Increase Buffers:

🛡️ Qualify at higher rate: Ensure you can afford payments if rates increase by 1-2% 💰 Maintain payment cushion: Keep 3-6 months of mortgage payments in liquid reserves 📊 Monitor Bank of Canada: Stay informed about monetary policy signals 🔄 Conversion option: Understand terms for converting to fixed if rates rise

The Stress Test Reality:

Even for renewals, switching lenders requires qualifying at the greater of your contract rate + 2% or 5.25%. For a 3.60% variable rate, you must qualify at 5.60%.

Qualification Example:

$500,000 mortgage, 25-year amortization

- Contract rate (3.60%): $2,500/month payment

- Stress test rate (5.60%): $3,120/month payment

- Required qualifying income: $97,500 annually (at 38.5% GDS)

Self-employed borrowers must demonstrate income sufficient for the stress test payment, even though actual payments will be substantially lower.

When Variable Rates Don’t Make Sense

Despite the compelling 2026 case for variables, some self-employed situations favor fixed rates:

❌ Highly volatile income: If business revenue fluctuates dramatically year-to-year ❌ Low risk tolerance: If payment predictability is essential for business planning ❌ Near retirement: If business wind-down is planned within 5 years ❌ Maximum debt ratios: If you’re already at qualifying limits with minimal buffer ❌ Large upcoming expenses: If major business investments will strain cash flow

For these situations, exploring fixed vs variable rate options with a comprehensive comparison may reveal that accepting a higher fixed rate provides necessary stability.

The Hybrid Approach: Split Mortgages

Some lenders allow splitting your mortgage between fixed and variable portions:

Example Split Strategy:

- 60% variable (3.60%): Captures rate savings, maintains flexibility

- 40% fixed (5.29%): Provides payment stability, hedges rate risk

- Blended effective rate: 4.28%

This approach offers:

- ✅ Reduced payment shock versus 100% fixed

- ✅ Partial protection against rate increases

- ✅ Flexibility to prepay variable portion aggressively

- ✅ Psychological comfort of partial rate certainty

Monitoring and Adjustment Strategy

Variable rate mortgages require active management:

Quarterly Review Checklist:

- 📈 Review current prime rate and your effective rate

- 💵 Assess business cash flow trends

- 🎯 Evaluate prepayment opportunities

- 📊 Monitor Bank of Canada announcements

- 🔄 Consider conversion to fixed if rate environment shifts

Trigger Points for Action:

Set predetermined trigger points for decision-making:

- Prime rate reaches 5.50%: Review conversion to fixed

- Payment increases by 15%: Assess business impact and adjustment needs

- Business revenue drops 20%: Prioritize payment stability

- Prime rate drops below 4.00%: Consider increasing prepayments

This disciplined approach prevents emotional decision-making during rate volatility.

Long-Term Wealth Building Through Strategic Renewal

The savings from navigating 26% renewal shocks through variable rate switches compound significantly:

5-Year Savings Projection:

$500,000 mortgage, comparing 5.89% fixed vs 3.60% variable (assuming prime holds)

- Fixed rate total payments: $162,150

- Variable rate total payments: $135,280

- Total savings: $26,870

- Additional principal reduction: $18,450

These savings can be redirected toward:

- 🏢 Business reinvestment and growth

- 💼 Additional real estate investments

- 📈 Retirement account contributions

- 🎯 Accelerated mortgage payoff

For self-employed entrepreneurs, this capital efficiency can mean the difference between business stagnation and strategic expansion.

Conclusion: Taking Control of Your 2026 Mortgage Renewal

The 2026 mortgage renewal landscape presents both significant challenges and unprecedented opportunities for self-employed Toronto entrepreneurs. While fixed-rate borrowers face payment increases of 26% and monthly hits exceeding $500, strategic navigation through variable rate switches offers a clear path to minimize financial shock.

The data is compelling: variable-rate renewals in 2026 show only 4% payment increases—a difference of nearly $470 per month compared to fixed-rate alternatives. For self-employed borrowers managing business cash flows, this isn’t merely a cost savings—it’s a strategic advantage that preserves capital for business growth and investment.

Your Action Plan for Renewal Success

Immediate Actions (90-120 Days Before Renewal):

- ✅ Gather complete documentation (2 years NOAs, T1s, business financials)

- ✅ Review and optimize credit reports

- ✅ Calculate current debt service ratios

- ✅ Research current self-employed mortgage rates

- ✅ Consult with specialized mortgage broker

Strategic Decisions (60-90 Days Before Renewal):

- 📊 Compare offers from multiple lender types

- 🎯 Evaluate variable vs fixed based on your risk tolerance

- 💰 Consider split mortgage strategies for balanced approach

- 🔍 Review prepayment privileges and flexibility features

- ⚖️ Assess total cost beyond headline rates

Execution Phase (30-60 Days Before Renewal):

- 🤝 Finalize lender selection and lock rate

- 📝 Complete underwriting requirements promptly

- 🏦 Arrange discharge if switching lenders

- 📅 Confirm renewal timing aligns with business cash flow

- ✍️ Sign documents and implement payment strategy

Beyond 2026: Building Long-Term Mortgage Strategy

Successfully navigating the 2026 renewal crisis positions self-employed entrepreneurs for sustained financial success:

- Establish lender relationships that recognize your business model

- Maintain organized financial documentation year-round

- Monitor rate environments and adjust strategies proactively

- Leverage savings for business growth and wealth building

- Plan ahead for future renewals with 3-5 year strategic outlook

The mortgage renewal shock of 2026 doesn’t have to derail your entrepreneurial journey. With strategic planning, proper documentation, and informed decision-making, self-employed Toronto entrepreneurs can not only survive this renewal cycle but emerge with stronger financial positions and optimized mortgage structures.

The difference between a $576 monthly increase and a $107 monthly increase isn’t just about rates—it’s about understanding your options, leveraging your unique position, and taking control of your financial future. The variable rate opportunity of 2026 may not last indefinitely, making now the critical time to act.

Don’t let renewal shock become a business crisis. Start your renewal preparation today, and transform what could be a $500+ monthly hit into a strategic advantage that fuels your entrepreneurial success for years to come.