April 9, 2026

Newcomer Mortgage Canada: How to Buy a Home as a New Immigrant in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

More than 400,000 new permanent residents arrive in Canada every year — and a growing number of them want to own a home within their first few years of landing. If you’re one of them, here’s the good news: getting a newcomer mortgage in Canada is absolutely possible, even without years of Canadian credit history or a long employment record. This guide to Newcomer Mortgage Canada: How to Buy a Home as a New Immigrant in 2026 walks you through every step, from CMHC programs to down payment rules to what documents you’ll actually need.

Key Takeaways 🏡

- You can qualify for a mortgage within your first 5 years in Canada, even with little or no Canadian credit history.

- CMHC and major banks offer specialized newcomer programs with flexible income and credit requirements.

- Permanent residents and work permit holders both qualify — but with different rules.

- Down payments can come from gifts from immediate family members, even if the funds are from outside Canada.

- A mortgage broker can match you with the right lender faster than going to a single bank alone.

Who Qualifies for a Newcomer Mortgage in Canada?

Not everyone who recently arrived in Canada qualifies under newcomer mortgage programs. Here’s the general rule: you must have immigrated within the last 60 months (5 years) to access these specialized products.

There are two main categories of newcomer borrowers:

🟢 Permanent Residents (PR)

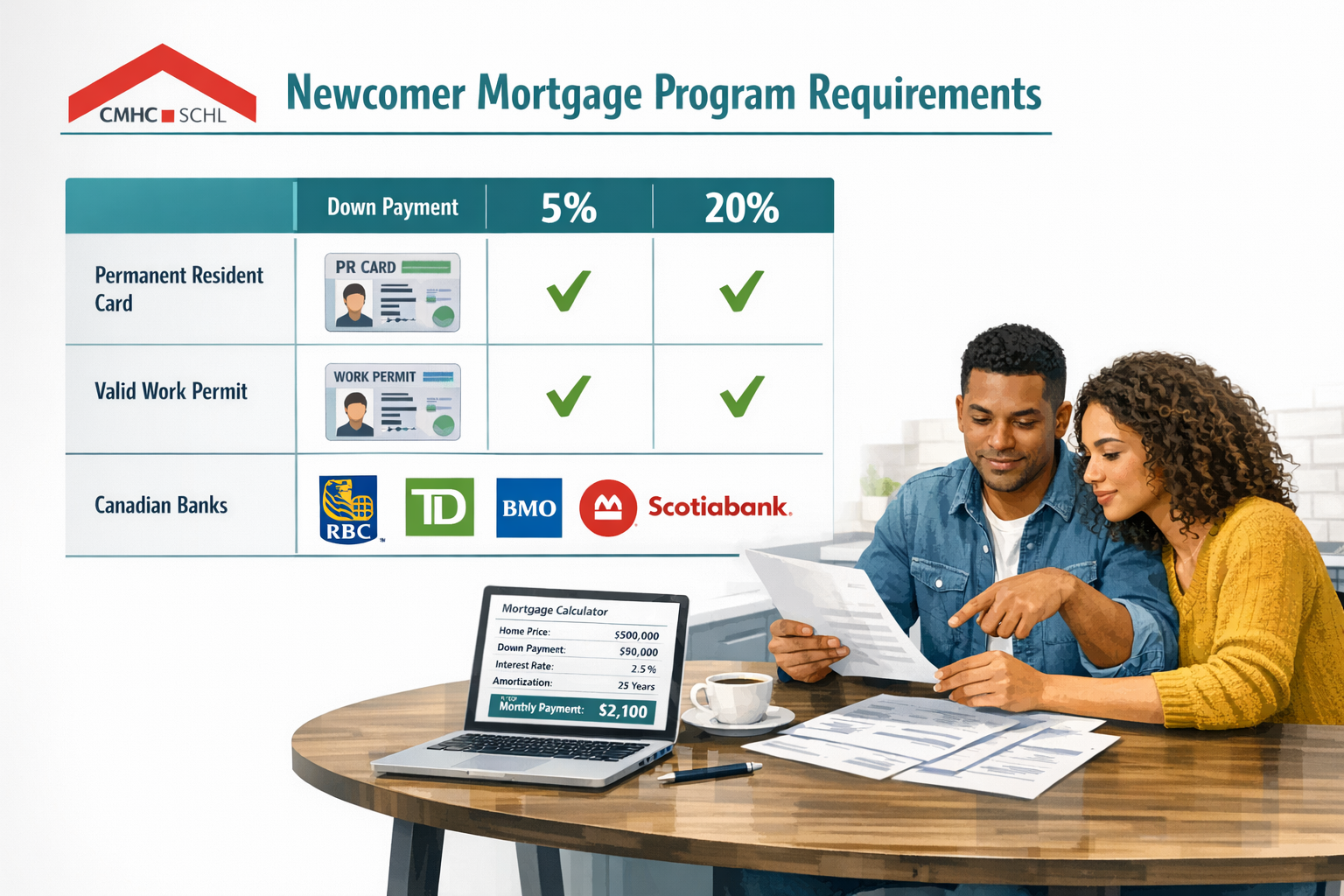

If you hold a Permanent Resident card, you have the strongest mortgage options available. Most lenders treat PRs almost identically to Canadian citizens. You can access CMHC-insured mortgages with as little as 5% down, and you’re eligible for all standard mortgage products.

🟡 Non-Permanent Residents (Work Permit Holders)

If you’re on a valid work permit and are legally authorized to work in Canada, you can still qualify — but lenders will want to see stronger compensating factors, like a larger down payment or documented job stability. You’ll typically need at least 10% down, and some lenders may require proof that your permit is renewable or that you have applied for PR status.

💡 Pro tip: Even if you’re on a work permit, don’t assume homeownership is out of reach. Many lenders — especially through a mortgage broker — have flexible programs designed exactly for your situation.

Understanding the CMHC Newcomer Mortgage Program

The CMHC Newcomer Mortgage Program is one of the most important tools available to new immigrants in Canada. CMHC (Canada Mortgage and Housing Corporation) provides mortgage loan insurance that protects lenders — which means lenders are more willing to approve borrowers who don’t yet have a long Canadian financial track record.

Here’s what you need to know about the CMHC newcomer mortgage program:

| Feature | Details |

|---|---|

| Property types covered | 1-to-4 unit properties (at least one owner-occupied unit) |

| Who qualifies | Permanent residents AND non-permanent residents with valid work authorization |

| Minimum down payment (PR) | 5% on homes up to $500,000 |

| Minimum down payment (non-PR) | Typically 10% |

| Credit history required | Flexible — alternative credit references accepted |

| Other insurers | Sagen (formerly Genworth) and Canada Guaranty also offer newcomer options |

It’s not just CMHC either. Sagen and Canada Guaranty — Canada’s two other mortgage insurers — also offer insured options for newcomers with less than 20% down. This gives you more flexibility when shopping for the right mortgage.

Down Payment Rules for New Immigrants 💰

One of the biggest questions newcomers ask is: “Where does my down payment need to come from?”

The good news is that the rules are more flexible than many people think.

Accepted Down Payment Sources:

- ✅ Your own savings — confirmed via 90-day bank statements

- ✅ Gifts from immediate family — parents, siblings, grandparents, legal guardians, or a spouse

- ✅ Funds from outside Canada — as long as they are converted to Canadian dollars and held in a Canadian account in liquid, accessible form

The key requirement: funds must be in Canada, in cash, and accessible at the time of the mortgage application. A 90-day bank statement showing the funds have been sitting in your Canadian account is the standard way to prove this.

Down Payment Breakdown by Purchase Price:

| Purchase Price | Minimum Down (PR) | Minimum Down (Non-PR) |

|---|---|---|

| Up to $500,000 | 5% | 10% |

| $500,001 – $999,999 | 5% on first $500K + 10% on remainder | 10% full amount |

| $1,000,000+ | 20% | 20% |

If you’re buying in Toronto, Mississauga, or Brampton — where average home prices often exceed $700,000 — understanding this tiered structure is critical for planning your savings.

For first-time buyers, our guide on the First Home Savings Account (FHSA) explains a powerful tax-free savings tool that newcomers who qualify as first-time buyers can use to grow their down payment faster.

What If You Have No Canadian Credit History?

This is the #1 concern for most newcomers — and it’s completely understandable. You may have had an excellent credit score in your home country, but that history doesn’t automatically transfer to Canada.

Here’s how lenders work around it:

Alternative Credit References Accepted:

- 📄 Rental payment history (landlord letters or bank statements)

- 📄 International credit report (some lenders accept Equifax or Experian reports from the US)

- 📄 Utility payment history

- 📄 Cell phone payment records

- 📄 Bank account statements showing consistent savings behaviour

The longer you’ve been in Canada, the more Canadian credit data you’ll have. Even one or two years of responsible credit card use in Canada can significantly strengthen your application.

To understand how credit scores affect your mortgage approval and what score you should aim for, check out our article on understanding credit scores in the mortgage approval process.

If you’re actively building your score right now, our guide on how to improve your credit score in Canada is a great place to start.

Income Documentation: What New Canadians Need to Provide

Proving your income is another area where newcomers sometimes face extra scrutiny. Here’s what lenders typically ask for:

If You’re Employed in Canada:

- Letter of employment (on company letterhead)

- Two most recent pay stubs

- T4 slips (if you’ve been employed for at least one tax year)

- Notice of Assessment from CRA (if available)

If You Just Started a New Job:

Starting a new job doesn’t disqualify you. Many newcomers land their first Canadian role shortly before applying for a mortgage. Our article on getting a mortgage in Canada with a new job covers exactly what to expect in this scenario.

Important Rule on Foreign Income:

⚠️ All debts held outside of Canada must be included in your Total Debt Service (TDS) ratio. However, rental income earned outside Canada is excluded from GDS/TDS calculations. This means foreign debt can hurt your qualification, but foreign rental income won’t help it.

Special Programs for Newcomers with Significant Assets

If you’re arriving in Canada with substantial savings or assets, there are two programs worth knowing about:

🏦 Equity Offset Program

If you can put 35% or more down, you may qualify for the Equity Offset Program. This program allows you to qualify for a larger mortgage amount by showing a minimum of 12 months’ worth of Principal, Interest, Taxes, and Heating (PITH) in liquid assets. This is especially useful if you’re retraining, completing education, or between jobs.

💎 High Net Worth Program

For newcomers with significant wealth, the High Net Worth program requires a minimum of $250,000 in liquid assets on deposit in Canada (on top of your down payment). It allows qualification based on asset holdings equivalent to the mortgage amount — not just income. This is a powerful option for business immigrants or investors.

Which Banks Offer Newcomer Mortgage Programs in 2026?

You’re not limited to one or two options. As of 2026, RBC, TD, BMO, Scotiabank, and CIBC all offer specialized newcomer mortgage programs with reduced credit history requirements and flexible down payment sourcing rules.

Each bank has slightly different criteria, rate structures, and qualifying thresholds. This is exactly why working with a mortgage broker is so valuable — instead of applying to one bank and hoping for the best, a broker can compare multiple lenders and find the one that fits your specific profile.

To understand how the mortgage stress test applies to your situation (yes, newcomers must pass it too!), read our breakdown of the mortgage stress test for home buyers in Canada.

Also, if you’re considering having a family member co-sign to strengthen your application, our guide on co-signing a mortgage in Canada explains the pros, cons, and responsibilities involved.

2026 Mortgage Rate Environment: What Newcomers Should Know 📊

The Bank of Canada held its policy rate at 2.25% in early 2026, keeping variable mortgage rates relatively stable. However, fixed mortgage rate forecasts suggest the 5-year fixed rate could climb toward 5% by the end of 2026.

For newcomers, this means:

- Variable rates offer lower payments now but carry some risk if rates rise

- Fixed rates provide payment certainty — helpful when you’re still establishing yourself financially

- Shorter terms (1-3 years) may give you flexibility to renegotiate as your credit profile strengthens

For a deeper look at how rates affect your purchasing power, explore our 2026 mortgage rate forecast resource.

Common Mistakes Newcomers Make When Applying for a Mortgage

Avoid these pitfalls before you apply:

- ❌ Not opening a Canadian bank account early enough — lenders want 90 days of statements

- ❌ Forgetting to declare foreign debts — these affect your TDS ratio

- ❌ Assuming your foreign credit score transfers — it doesn’t automatically

- ❌ Skipping mortgage pre-approval — it shows sellers you’re serious

- ❌ Going to only one bank — a broker gives you access to dozens of lenders

For a full list of pitfalls to avoid, see our article on common mistakes to avoid when applying for a mortgage in Canada.

Conclusion: Your Path to Homeownership Starts Now

Buying a home as a new immigrant in Canada in 2026 is not just a dream — it’s a realistic, achievable goal with the right preparation and guidance. The newcomer mortgage programs offered through CMHC, major banks, and alternative lenders are specifically designed to help people in your situation get into the market, even without years of Canadian credit history or a long employment record.

Here are your actionable next steps:

- ✅ Open a Canadian bank account and start building a 90-day paper trail

- ✅ Apply for a Canadian credit card and use it responsibly every month

- ✅ Gather your income documents — employment letters, pay stubs, foreign bank statements

- ✅ Calculate your down payment and confirm the funds are in a Canadian account

- ✅ Contact a mortgage broker who specializes in newcomer mortgages in the GTA

At Everything Mortgages, we work with new immigrants and permanent residents across Toronto, Brampton, Mississauga, and Markham every day. We understand the unique challenges you face — and we know exactly which lenders offer the best programs for your situation.

👉 Ready to take the first step? Explore all our newcomer mortgage resources or contact our team today — your Canadian home is closer than you think.