March 15, 2026

Private Mortgages for Toronto’s 450% Delinquency Surge: Early Intervention Strategies in Q2 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

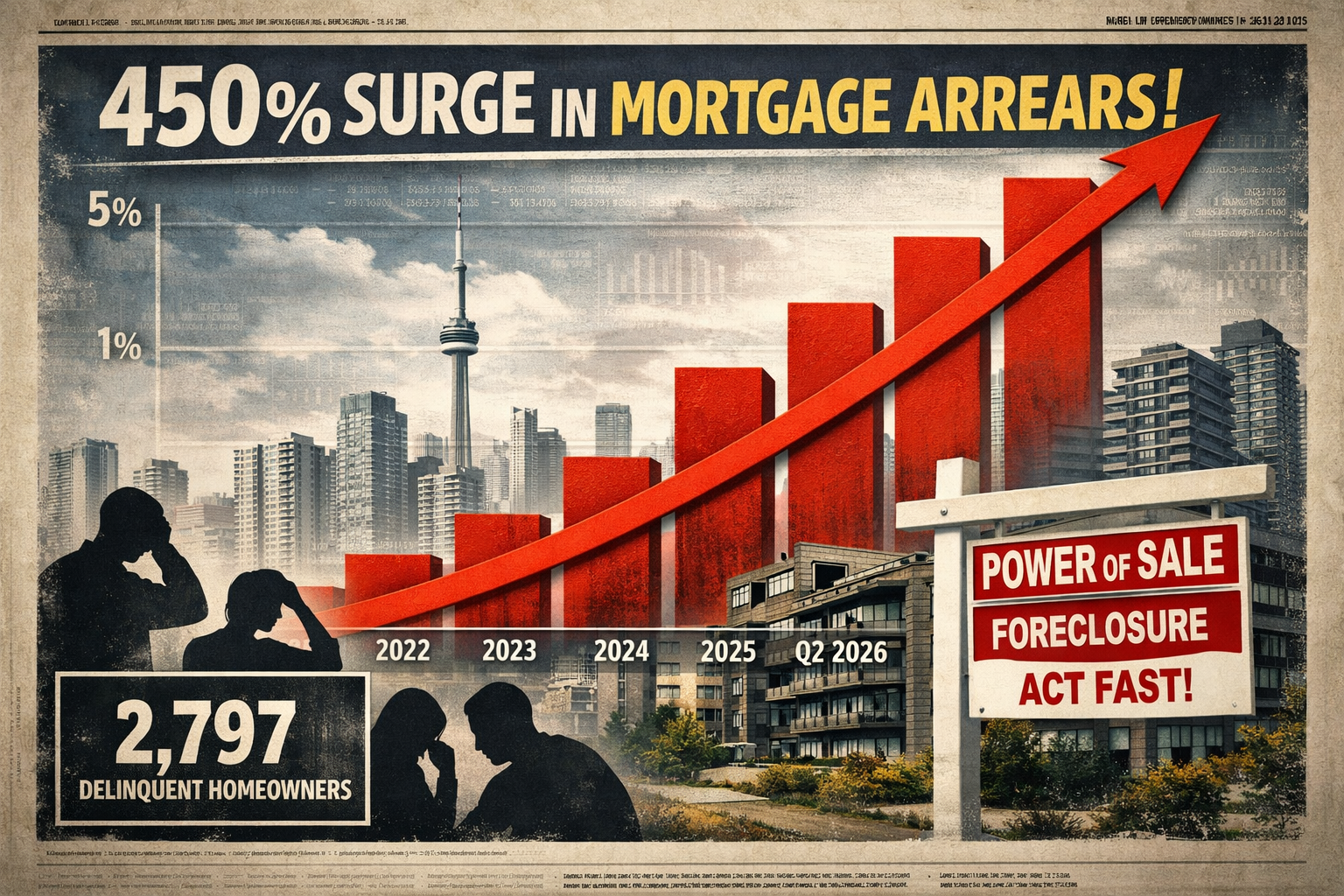

Toronto homeowners are facing a financial storm unlike anything seen in decades. Mortgage delinquencies have surged by 450% since Q3 2022, with 2,797 households already in arrears by late 2025 — and Q2 2026 data suggests the number is still climbing [1][7]. For equity-rich homeowners caught in this wave, private mortgages for Toronto’s 450% delinquency surge represent a critical early intervention tool — but only when used strategically and at the right time.

This guide explains how to spot the early warning signs, qualify through home equity, and use short-term private lending to stop a Power of Sale before it starts.

Key Takeaways

- 🚨 Toronto mortgage arrears have surged 450% since Q3 2022, with projections pointing to 3,500+ affected families soon

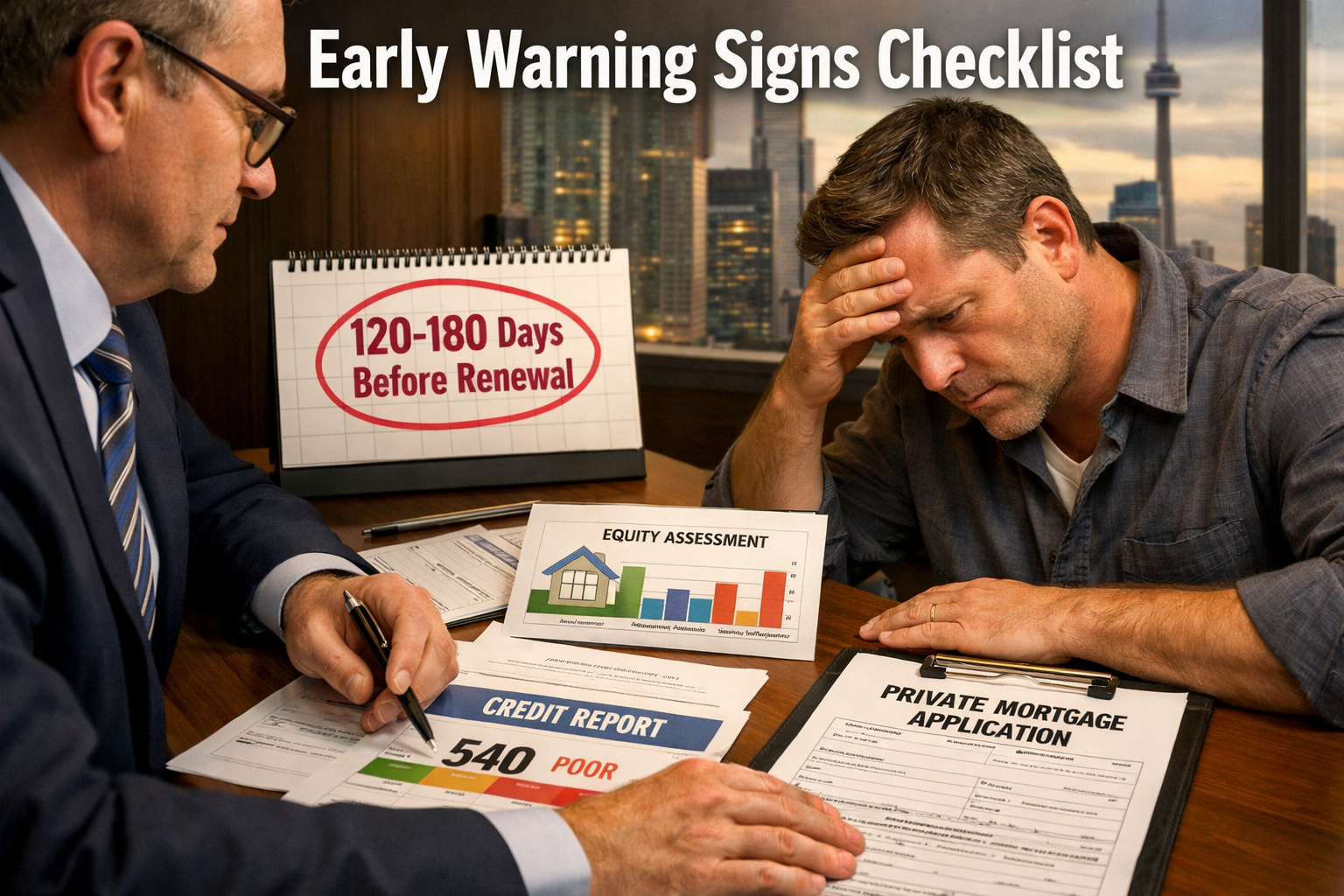

- ⏰ The ideal window to act is 120–180 days before renewal — waiting causes credit damage that locks out better lending options

- 🏠 Home equity is the primary qualification tool for private mortgages, making them accessible even with bruised credit

- 🔄 Private mortgages work best as 6–36 month bridges, not long-term solutions — the exit strategy matters

- 📋 Early warning signs like missed credit card payments can appear 1–2 years before full mortgage delinquency

Understanding Toronto’s 450% Delinquency Crisis

Toronto has become Canada’s undisputed hotspot for mortgage arrears [8]. The numbers are stark:

| Metric | Data Point |

|---|---|

| Arrears as of Q3 2025 | 2,797 homeowners |

| Surge since Q3 2022 | ~322–450% |

| Power of Sale listings since 2022 | Up 543% |

| Projected delinquencies (near-term) | 3,500+ families [7] |

| National arrears rate (context) | Still under 0.5% [5] |

The root causes are layered. CMHC analysts point to high household debt loads, cash-flow problems among “mom-and-pop” investors, and falling condo prices that have eroded equity buffers [4]. Compounding this is the 2020–2022 mortgage renewal cliff — thousands of homeowners who locked in at ultra-low pandemic rates are now renewing at rates 2–3% higher, creating immediate payment shock.

💬 “Delinquency lags renewals by 6–12 months — meaning the worst of Toronto’s arrears crisis may not appear until late 2026.” — CMHC analysts [4]

The GTA job market weakness and global tariff/inflation pressures are accelerating the timeline. A March 2026 market analysis warned of a “Toronto Mortgage Bloodbath” scenario if conditions don’t stabilize [7].

Understanding what private mortgage options exist in Ontario is the first step for homeowners who feel the pressure building.

Early Warning Signs: Spotting Trouble Before It Becomes a Crisis

The Bank of Canada has identified a clear pattern: credit card payment misses appear 1–2 years before mortgage delinquency, with the pace accelerating sharply in the final 6 months [5]. Catching these signals early is everything.

🔴 The Three-Stage Warning System

Stage 1 — 12–24 Months Before Delinquency:

- Missing or making minimum-only credit card payments

- Increasing reliance on lines of credit for daily expenses

- Skipping RRSP contributions to cover bills

Stage 2 — 6–12 Months Before Delinquency:

- Carrying credit card balances month-to-month consistently

- Deferring property tax or utility payments

- Receiving calls from lenders about overdue accounts

Stage 3 — Imminent Risk (Under 6 Months):

- A missed mortgage payment (triggers 90-day credit reporting)

- Receiving a demand letter or Power of Sale notice

- Inability to qualify for any renewal offer from current lender

⚠️ Critical fact: A single 90-day missed payment can push borrowers into B-lender territory where rates spike to 7–9%, making recovery even harder [1].

Homeowners approaching renewal should also review their fixed vs. variable mortgage options carefully — rate structure choices at renewal can mean the difference between manageable payments and default.

For those who’ve already received a consumer proposal or have credit challenges, understanding mortgage options after a consumer proposal can open unexpected doors.

Private Mortgages for Toronto’s 450% Delinquency Surge: The Early Intervention Playbook

This is where strategy becomes survival. Private mortgages for Toronto’s 450% delinquency surge are not a last resort — they are a precision tool when deployed at the right moment.

The 120–180 Day Rule

Mortgage expert Marcus Chen (CollectorHQ) is direct: start private mortgage conversations 120–180 days before renewal [1]. Here’s why the timeline matters:

- Before the 120-day mark: Credit is still intact, equity is the primary qualifier, rates are negotiable

- At 90 days past due: Credit score drops significantly, B-lender rates jump to 7–9%, options narrow fast

- After Power of Sale notice: Private options still exist but at premium rates; legal costs mount

Ron Butler of Butler Mortgage reinforces this with his advice to shop renewals 75–90 days early, emphasizing cash-flow stress testing over rate predictions in the current climate [3].

How Private Mortgage Qualification Works

Unlike banks, private lenders focus primarily on loan-to-value (LTV) ratios, not income documentation or credit scores. This is why equity-rich Toronto homeowners — even those with bruised credit — can often qualify.

Typical private mortgage parameters in 2026:

- LTV: Up to 75–80% of appraised value

- Rates: 8–12% (higher than banks, but lower than Power of Sale losses)

- Term: 6 months to 3 years (bridge financing)

- Approval timeline: 5–10 business days

Learn more about how easy it is to get a private mortgage and what lenders actually look for in the current market.

Private vs. Alternative Options: A Quick Comparison

| Option | Best For | Rate Range | Speed |

|---|---|---|---|

| B-Lender | Minor credit issues, stable income | 6–9% | 1–2 weeks |

| Private Mortgage | Equity-rich, credit-damaged | 8–12% | 5–10 days |

| HELOC | Existing equity, good credit | Prime +0.5–1% | 2–4 weeks |

| Debt Consolidation Mortgage | Multiple high-interest debts | 7–10% | 1–2 weeks |

For homeowners carrying significant consumer debt alongside mortgage stress, a debt consolidation mortgage may reduce total monthly obligations before pursuing a private route.

Perch Capital CEO Alex Leduc noted in February 2026 that brokers are increasingly prioritizing fast approvals and flexible policies in private lending — a direct response to the renewal wave pushing borrowers out of traditional bank channels [1].

What FCAC and OSFI Say About Alternatives

Regulators aren’t ignoring the crisis. The FCAC Mortgage Charter allows lenders to offer temporary amortization extensions beyond standard 25–30 year limits to reduce monthly payments — a preferred first step for lower-risk cases [3][6]. OSFI continues to promote early intervention through reserve buffers and stress-test compliance [6].

The takeaway: exhaust regulated options first, then move to private lending as a bridge — not a permanent solution.

Executing the Exit Strategy: Getting Back to Traditional Lending

A private mortgage without an exit plan is a trap. The goal is always to use the 6–36 month bridge period to rebuild the financial profile needed for a return to A or B lending.

The Private Mortgage Recovery Roadmap

Month 1–3: Stabilize

- Stop all missed payments immediately

- Consolidate high-interest consumer debt where possible

- Begin rebuilding credit with secured cards or small installment loans

Month 3–12: Rebuild

- Maintain a perfect payment record on the private mortgage

- Reduce total debt-to-income ratio

- Document all income sources (especially important for self-employed borrowers navigating the 2026 mortgage stress test)

Month 12–36: Transition

- Reassess credit score (target 620+ for B-lenders, 680+ for A-lenders)

- Obtain fresh property appraisal to confirm equity position

- Engage a broker to shop renewal options 90 days before private term expires

💡 Pro tip: Private mortgages work best when the homeowner has a specific, measurable trigger for the exit — a property sale, business income event, or credit score milestone.

Homeowners should also understand mortgage penalties and how to avoid them when breaking a private term early to move back to conventional lending.

For those considering using a second mortgage alongside their primary loan as a short-term solution, understanding how to get a second mortgage in Ontario provides important context on costs and risks.

A Note on Critics

Not everyone views private mortgages as a solution. Some analysts argue they create debt layering — adding high-rate debt on top of existing stress — without addressing the root affordability problem [1]. This criticism is valid when private mortgages are used reactively rather than proactively. The difference between a lifeline and a trap is timing and planning.

Conclusion: Act Early, Act Smart

Toronto’s delinquency surge is real, accelerating, and unlikely to reverse quickly before late 2026 [4][7]. For homeowners feeling the pressure of rising payments, falling property values, or credit stress, the message is clear: the window to act effectively is now.

Actionable next steps for Q2 2026:

- ✅ Audit your finances today — check for Stage 1 warning signs before they become Stage 2

- ✅ Get a property appraisal — know your current LTV before approaching any lender

- ✅ Contact a licensed mortgage broker 120+ days before renewal — not 30 days

- ✅ Explore all regulated options first — FCAC forbearance, B-lenders, HELOCs

- ✅ Build your exit strategy before signing any private mortgage — know your 12–36 month plan

Private mortgages for Toronto’s 450% delinquency surge are most powerful when used as a planned bridge, not an emergency escape hatch. Homeowners who move early keep their options open. Those who wait often find the door has closed.

Start a mortgage solution inquiry today to understand which path is right for your specific situation.

References

[1] Mortgage Delinquency Crisis In Toronto 2026 When Should Private Mortgages Replace Traditional Renewals – https://everythingmortgages.ca/blog/mortgage-delinquency-crisis-in-toronto-2026-when-should-private-mortgages-replace-traditional-renewals/

[2] Watch – https://www.youtube.com/watch?v=Cg4RXP-3Vq4

[3] Renewing Your Mortgage In 2026 Heres What To Expect – https://www.ratehub.ca/blog/renewing-your-mortgage-in-2026-heres-what-to-expect/

[4] Mortgage Renewal Wave Strains Some Regions Borrowers – https://www.cmhc-schl.gc.ca/observer/2026/mortgage-renewal-wave-strains-some-regions-borrowers

[5] The Bank Of Canada Says These Are The 3 Warning Signs For Mortgage Default – https://globalnews.ca/news/11715798/the-bank-of-canada-says-these-are-the-3-warning-signs-for-mortgage-default/

[6] Osfis Annual Risk Outlook Fiscal Year 2025 2026 – https://www.osfi-bsif.gc.ca/en/about-osfi/reports-publications/osfis-annual-risk-outlook-fiscal-year-2025-2026

[7] Watch – https://www.youtube.com/watch?v=PMEJjgmzh78

[9] Watch – https://www.youtube.com/watch?v=fhmdbl83A-c

[10] everythingmortgages.ca – https://everythingmortgages.ca/?post_type=post&p=8912