March 10, 2026

Self-Employed Toronto Borrowers Facing 26% Fixed Renewal Shocks in 2026: Proven Strategies to Cut Payments by $500+ Monthly

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage renewal landscape in 2026 has become a financial minefield for Canadian homeowners, particularly self-employed Toronto borrowers facing 26% fixed renewal shocks in 2026. With 1.15 million mortgage holders across Canada set to renew their mortgages this year, those who locked in ultra-low rates during the pandemic are now confronting a harsh reality: monthly payments that could surge by hundreds—or even thousands—of dollars.

For self-employed professionals, freelancers, and business owners in Toronto, this challenge is amplified. Unlike salaried employees, self-employed borrowers face additional scrutiny during the renewal process, making it harder to negotiate better terms or switch lenders. However, with the right strategies, it’s entirely possible to reduce these payment shocks by $500 or more each month.

Key Takeaways

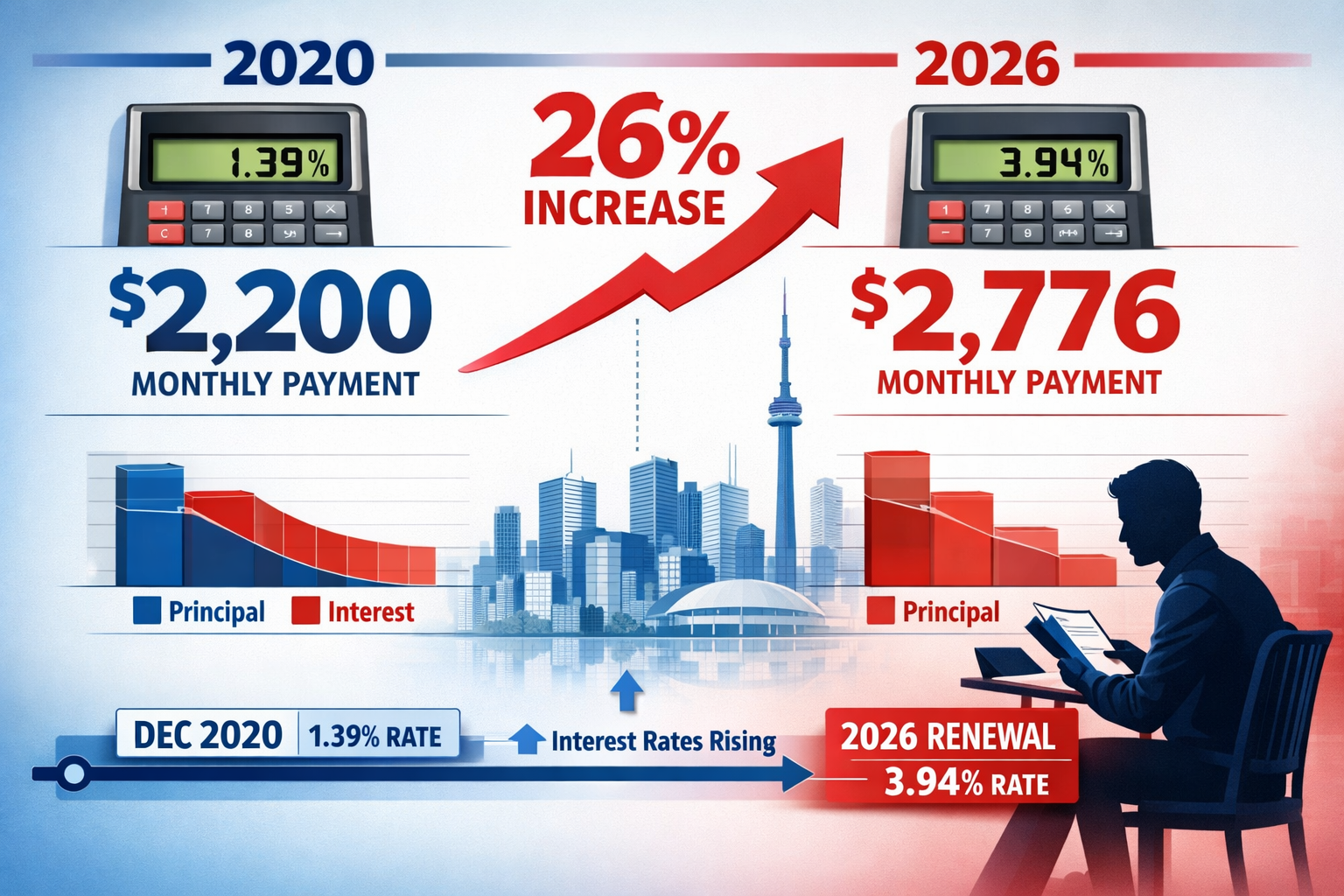

✅ Fixed-rate borrowers renewing in 2026 face an average 26% payment increase, jumping from approximately $2,200 to $2,776 monthly—an additional $576 per month or $6,912 annually.

✅ Self-employed borrowers encounter unique challenges during renewal, including stricter income verification and limited negotiating power without proper documentation.

✅ Strategic preparation 120 days before renewal can unlock better rates, alternative lender options, and payment reductions of $500+ monthly through refinancing or lender switching.

✅ Current Toronto rates in 2026 offer opportunities: best 5-year fixed at 3.74%, 3-year fixed at 3.69%, and variable rates at 3.45%—significantly better than renewal offers from some institutions.

✅ Specialized mortgage solutions like bank statement loans and alternative documentation programs can help self-employed borrowers qualify for competitive rates despite non-traditional income.

Understanding the 26% Renewal Shock: What Self-Employed Borrowers Face

The numbers tell a sobering story. According to recent mortgage industry analysis, borrowers who secured fixed-rate mortgages in December 2020 at the historic low of 1.39% are now facing renewal rates averaging 3.94%.[1] This seemingly modest rate increase translates to a 26% jump in monthly payments—from approximately $2,200 to $2,776 for a typical Toronto mortgage.

For self-employed professionals, this payment shock arrives with additional complications. Unlike traditional employees who can simply provide a T4 and employment letter, self-employed borrowers must navigate:

- Detailed income verification through two years of Notice of Assessment (NOA) documents

- Business financial statements that may show lower taxable income due to legitimate deductions

- Stricter debt service ratios that account for variable business income

- Limited access to insurable mortgage rates if equity has dropped below 20%

The Scale of the 2026 Renewal Crisis

The Canada Mortgage and Housing Corporation (CMHC) reports that 1.15 million mortgage holders will renew in 2026, with another 940,000 scheduled for 2027.[1] This creates unprecedented pressure on the mortgage market and significant challenges for borrowers unprepared for higher payments.

Interestingly, variable-rate borrowers face a much smaller adjustment. Since they’ve already absorbed rate increases over the past few years, their payment jump averages just 4%—rising from approximately $2,121 to $2,797 monthly.[1] This highlights the particular vulnerability of fixed-rate holders who deferred the pain until renewal.

For self-employed Toronto borrowers, understanding how self-employed borrowers in Toronto can navigate the 2026 mortgage stress test becomes critical to securing favorable renewal terms.

Why Self-Employed Borrowers Face Amplified Renewal Challenges

While all borrowers renewing in 2026 face higher rates, self-employed individuals encounter unique obstacles that can significantly limit their options and negotiating power.

Income Documentation Hurdles

Traditional lenders assess self-employed income differently than salaried employment. The key challenges include:

Tax Return Complexities: Lenders typically average the past two years of income reported on your Notice of Assessment. For many self-employed professionals who maximize deductions to minimize taxes, this reported income may be substantially lower than actual cash flow—creating qualification gaps.

Business Structure Impact: Whether you operate as a sole proprietor, partnership, or corporation affects how lenders calculate your qualifying income. Incorporated business owners may face additional scrutiny of retained earnings and dividend income.

Income Volatility: Fluctuating monthly or seasonal income patterns make it harder to demonstrate stable repayment capacity, even when annual totals are strong.

Limited Lender Mobility

One of the most powerful strategies for reducing renewal payment shocks is switching lenders to secure better rates. However, self-employed borrowers face barriers here:

- Full re-qualification required: Unlike simple renewals with your current lender, switching requires complete income verification as if applying for a new mortgage

- Higher documentation standards: Alternative lenders may require additional business financials, contracts, or client letters

- Timing constraints: Gathering proper documentation takes time that many borrowers don’t have as renewal deadlines approach

Understanding documentation requirements for self-employed mortgage approval in Toronto can help you prepare months in advance.

Equity Position Complications

Toronto’s real estate market has experienced volatility in recent years. Self-employed borrowers whose home values have declined may find themselves:

- Unable to access insurable rates if equity has fallen below 20%

- Facing higher uninsured mortgage rates that can add 0.20% to 0.40% to their renewal rate

- Limited in refinancing options to consolidate debt or access equity for payment relief

For those exploring alternatives, learning about obtaining a mortgage when you’re self-employed provides foundational strategies that apply to both purchases and renewals.

Proven Strategies to Cut Payments by $500+ Monthly for Self-Employed Toronto Borrowers

The good news? Self-employed Toronto borrowers have multiple proven strategies to significantly reduce renewal payment shocks. With proper preparation and expert guidance, cutting monthly payments by $500 or more is entirely achievable.

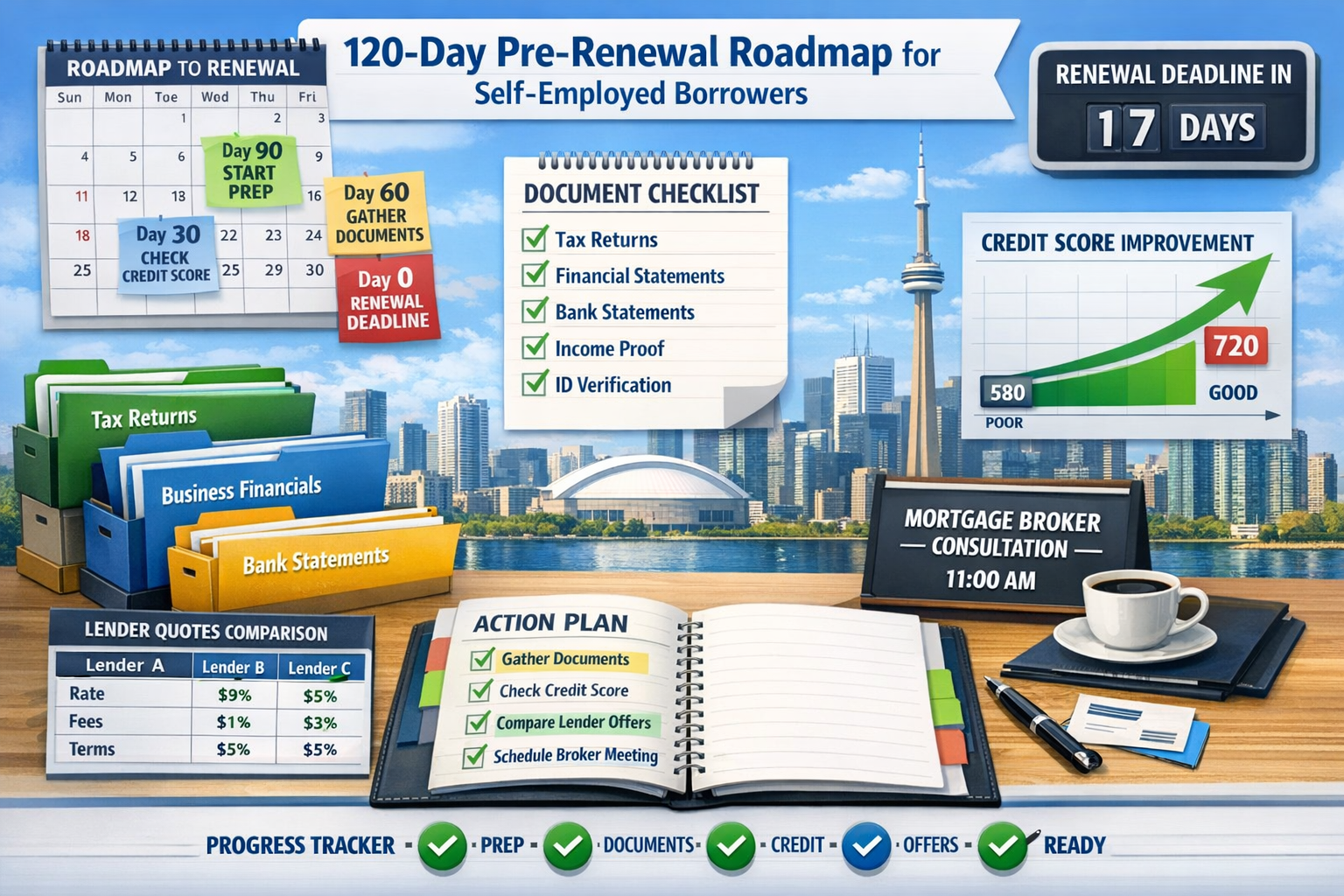

Strategy #1: Start the Renewal Process 120 Days Early

Timing is everything when it comes to mortgage renewals, especially for self-employed borrowers who need extra time to gather documentation.

Action Steps:

- Review your renewal notice immediately when it arrives (typically 120 days before maturity)

- Assess your current financial position, including updated credit score, home equity, and business income trends

- Gather documentation early: two years of NOAs, business financial statements, bank statements, and proof of business continuity

- Contact a mortgage broker who specializes in self-employed borrowers to explore all available options

Starting early gives you leverage. You’re not forced to accept your current lender’s initial offer, which is often higher than competitive market rates.

Strategy #2: Leverage Current Market Rates Through Lender Shopping

As of March 2026, the best available rates in Toronto are significantly better than many renewal offers:

| Term | Best Available Rate | Typical Renewal Offer | Potential Savings |

|---|---|---|---|

| 5-Year Fixed | 3.74% | 3.94%+ | 0.20%+ |

| 3-Year Fixed | 3.69% | 3.89%+ | 0.20%+ |

| Variable | 3.45% | 3.75%+ | 0.30%+ |

Source: Current best rates in Toronto, March 2026[2]

On a $500,000 mortgage with 20 years remaining, reducing your rate from 3.94% to 3.74% saves approximately $60 per month or $720 annually. Combined with other strategies, this contributes significantly to the $500+ monthly reduction target.

For the latest competitive rates, check current self-employed mortgage rates in Toronto for February 2026.

Strategy #3: Consider Alternative Documentation Programs

Traditional income verification doesn’t work for all self-employed borrowers. Fortunately, specialized programs exist:

Bank Statement Loans: These programs qualify you based on deposits into your business bank accounts rather than tax returns. This can be particularly beneficial if you:

- Write off significant business expenses that reduce taxable income

- Have strong cash flow but lower reported income

- Operate a cash-intensive business

Learn more about bank statement loans for self-employed borrowers as a 2026 game-changer.

Stated Income Programs: Available through select alternative lenders, these programs require less documentation but typically come with:

- Slightly higher interest rates (0.25% to 0.75% premium)

- Larger down payment or equity requirements (typically 20%+)

- Stronger credit score thresholds (680+)

DSCR Loans: For self-employed real estate investors, DSCR loans for self-employed real estate investors qualify you based on rental property income rather than personal income.

Strategy #4: Extend Amortization to Reduce Monthly Payments

If you’ve paid down your mortgage for several years, you may have the option to re-extend your amortization back to 25 or 30 years at renewal. While this increases total interest paid over the life of the mortgage, it can provide immediate payment relief.

Example Scenario:

- Original mortgage: $500,000 at 1.39% with 25-year amortization

- After 5 years: Balance of approximately $430,000 with 20 years remaining

- Renewal at 3.94% with 20 years remaining: $2,590/month

- Renewal at 3.94% re-extended to 25 years: $2,276/month

- Monthly savings: $314

Combined with rate shopping and other strategies, this helps reach the $500+ monthly reduction target.

Strategy #5: Refinance to Consolidate High-Interest Debt

Many self-employed borrowers carry business-related debt on credit cards or lines of credit at rates of 8% to 21%. Refinancing your mortgage to consolidate this debt can dramatically reduce total monthly obligations.

Example Calculation:

- Credit card debt: $30,000 at 19.99% = $600/month minimum payment

- Business line of credit: $20,000 at 7.5% = $250/month interest-only

- Total monthly debt payments: $850

By refinancing to access home equity and consolidate this $50,000 debt into your mortgage at 3.94%, you add approximately $240/month to your mortgage payment while eliminating $850 in other payments—a net monthly savings of $610.

Explore more about mortgage refinancing and switching lenders at renewal to understand the full advantages for self-employed borrowers.

Strategy #6: Work with a Specialized Mortgage Broker

Perhaps the most impactful strategy is partnering with a mortgage professional who understands the unique challenges self-employed borrowers face. A specialized broker can:

- Access multiple lenders including those not available to the public

- Structure your application to highlight strengths and minimize weaknesses

- Navigate alternative documentation requirements effectively

- Negotiate on your behalf for better rates and terms

- Identify programs specifically designed for self-employed professionals

For comprehensive guidance, review the ultimate guide to securing a mortgage for self-employed Canadians.

Preparing Your Financial Profile: Action Steps for Self-Employed Borrowers

Successfully navigating renewal as a self-employed borrower requires strategic preparation. Here’s your action plan:

6 Months Before Renewal

📋 Document Organization

- Gather the past two years of personal tax returns and Notices of Assessment

- Compile business financial statements (profit & loss, balance sheet)

- Collect 3-6 months of business bank statements

- Update your personal credit report and address any issues

💼 Business Income Optimization

- Work with your accountant to ensure income reporting supports mortgage qualification

- Consider timing of income draws or dividends if incorporated

- Document contracts or recurring revenue streams

🏠 Property Assessment

- Research current market value of your Toronto property

- Calculate your loan-to-value ratio

- Assess whether you have 20%+ equity for better rate access

120 Days Before Renewal

🔍 Market Research

- Review current mortgage rates from multiple sources

- Understand the difference between your lender’s renewal offer and market rates

- Consult with a mortgage broker to explore all options

📞 Lender Engagement

- Contact your current lender to discuss renewal options

- Request their best rate offer in writing

- Ask about alternative documentation programs if traditional income verification is challenging

90 Days Before Renewal

⚖️ Decision Making

- Compare your current lender’s offer against competitive market rates

- Evaluate the cost-benefit of switching lenders (considering any penalties or fees)

- Decide on your preferred term length and rate type (fixed vs. variable)

📄 Application Submission

- If switching lenders, submit your full application with all documentation

- Ensure all information is accurate and complete to avoid delays

- Maintain communication with your broker throughout the process

60 Days Before Renewal

✅ Final Steps

- Receive formal approval from new lender (if switching)

- Review all terms and conditions carefully

- Coordinate timing to ensure seamless transition at renewal date

- Confirm there are no gaps in coverage or payment schedules

Understanding Rate Forecasts: What to Expect in 2026 and Beyond

While renewal shocks are real, understanding the broader rate environment can help you make informed decisions about term length and rate type.

Current Rate Environment

As of March 2026, the Bank of Canada prime rate sits at 4.45%, with market expectations pricing the BoC rate at 2.25% through December 2026.[3] This suggests potential for further rate decreases, though the pace and magnitude remain uncertain.

TD Economics reports that the average payment increase in 2026 is running at approximately 6%, down from 10% in 2025, with a median mortgage payment change of -0.3%.[3] This more moderate average reflects the fact that many variable-rate holders have already absorbed increases, while some borrowers are actually seeing decreases as they renew from higher rates locked in during 2022-2023.

Strategic Term Selection

Given the rate environment, self-employed borrowers should consider:

Shorter Terms (1-3 Years): If you believe rates will continue declining, a shorter term allows you to renew again sooner at potentially lower rates. The 3-year fixed at 3.69% offers a middle ground.[2]

Variable Rates: At 3.45%, variable rates are currently the lowest option and could decrease further if the Bank of Canada continues cutting.[2] However, they carry payment uncertainty.

5-Year Fixed: At 3.74%, this provides payment certainty and protection against potential rate increases, though you sacrifice the potential benefit of future decreases.[2]

For detailed analysis, review how 2026 mortgage rate forecasts impact self-employed homebuyers and whether mortgage rates will drop further for self-employed in Toronto in 2026.

Common Mistakes Self-Employed Borrowers Make at Renewal

Avoiding these pitfalls can save thousands of dollars:

❌ Automatically accepting the renewal offer: Your current lender’s initial offer is rarely their best rate. Always negotiate or shop around.

❌ Waiting until the last minute: Self-employed documentation takes time to gather and review. Starting late eliminates your negotiating leverage.

❌ Failing to update financial documentation: Using outdated tax returns or financial statements can result in qualification based on lower income than your current reality.

❌ Ignoring credit score issues: Small credit problems can significantly impact your rate. Address them months before renewal.

❌ Not considering total debt picture: Focusing only on mortgage payments while carrying high-interest debt misses opportunities for overall financial improvement through refinancing.

For a comprehensive overview of common errors, see top 5 mistakes self-employed homebuyers make.

Real-World Success Stories: How Self-Employed Borrowers Cut Payments

Case Study #1: Freelance Consultant

- Situation: $600,000 mortgage renewing from 1.49% to 4.09% (lender’s offer)

- Challenge: Income fluctuates significantly month-to-month

- Solution: Used bank statement loan program showing strong deposit history

- Result: Secured 3.79% rate, extended amortization, reduced payment from $2,850 to $2,320

- Monthly savings: $530

Case Study #2: Incorporated Business Owner

- Situation: $450,000 mortgage renewing from 1.39% to 3.94%

- Challenge: Shows minimal personal income due to dividend strategy

- Solution: Refinanced to consolidate $35,000 in business debt, worked with specialized broker

- Result: 3.74% rate, eliminated $625 in separate debt payments, mortgage increased by only $180

- Net monthly savings: $445

Case Study #3: Real Estate Agent

- Situation: $550,000 mortgage renewing, commission-based income

- Challenge: 2024 was a slow year, lowering two-year income average

- Solution: Provided signed contracts and pipeline documentation, switched to lender with flexible income assessment

- Result: Qualified at 3.69% on 3-year term instead of 4.19% renewal offer

- Monthly savings: $150, plus positioned for lower rates at next renewal

Conclusion: Taking Control of Your 2026 Renewal

Self-employed Toronto borrowers facing 26% fixed renewal shocks in 2026 are navigating one of the most challenging mortgage environments in recent history. With 1.15 million Canadians renewing this year and payment increases averaging $576 monthly for fixed-rate holders, the financial pressure is real and significant.

However, this challenge is not insurmountable. By understanding the unique obstacles self-employed borrowers face—from stricter income verification to limited lender mobility—you can develop a strategic approach that turns potential crisis into opportunity.

Your Action Plan

Start today by taking these immediate steps:

- Calculate your renewal date and mark 120 days prior on your calendar

- Gather your financial documentation including tax returns, NOAs, and business statements

- Check your credit score and address any issues immediately

- Research current market rates to understand the competitive landscape

- Contact a mortgage broker who specializes in self-employed borrowers

Remember: The $500+ monthly savings target is achievable through a combination of strategies—better rates through shopping, amortization extension, debt consolidation, and alternative documentation programs. No single strategy needs to deliver all the savings; the cumulative effect of multiple approaches creates the breakthrough.

With the right preparation, expert guidance, and strategic timing, you can transform a potential 26% payment shock into a manageable transition—or even an opportunity to improve your overall financial position.

The mortgage renewal crisis of 2026 is real, but it doesn’t have to derail your financial goals. Take action now, and you’ll be positioned to weather this storm while setting yourself up for long-term success.

For personalized guidance on your specific situation, consider consulting with a mortgage professional who understands the nuances of how self-employed borrowers can secure insurable mortgage rates in Toronto under new 2026 rules.

References

[1] What Can Mortgage Borrowers Expect In 2026 – https://www.ratehub.ca/blog/what-can-mortgage-borrowers-expect-in-2026/

[2] Mortgage Rates In Toronto Your Complete 2026 Guide – https://bestrates.ca/mortgage-rates-in-toronto-your-complete-2026-guide

[3] Ca Mortgage Renewal Mission Possible – https://economics.td.com/ca-mortgage-renewal-mission-possible

[4] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast