March 19, 2026

Self-Employed Variable Rate Lock-In Strategy: Should You Switch to 3.45%-3.95% Fixed Before Mid-2026 Rate Hikes?

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

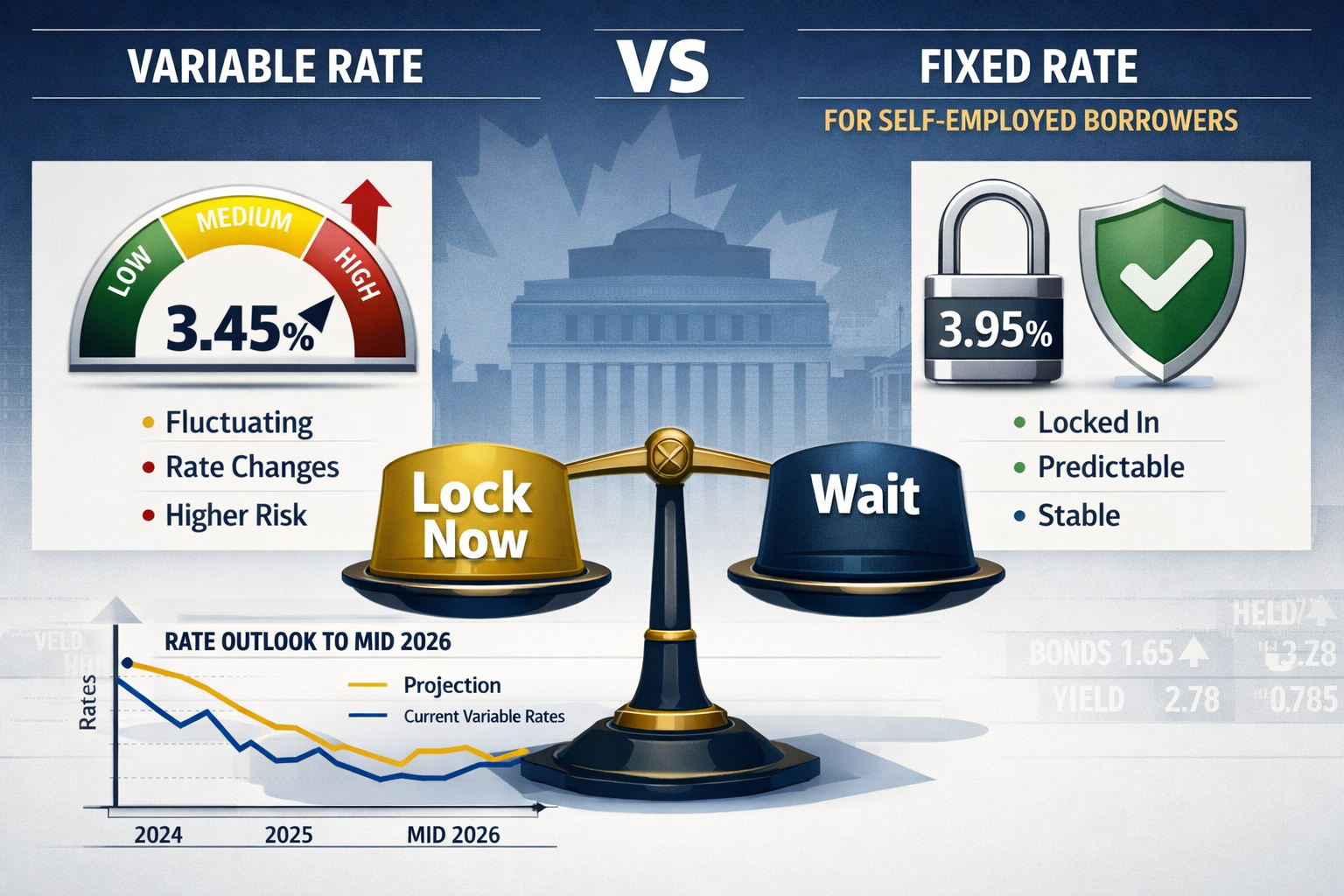

The Bank of Canada has held its policy rate steady at 2.25% through the first quarter of 2026, providing temporary relief to variable-rate mortgage holders. However, bond markets are telling a different story—they’re pricing in potential rate hikes later this year. For Self-Employed Canadians currently enjoying variable rates between 3.45% and 3.95%, a critical question emerges: Should you lock in now, or wait and risk higher rates?

This decision carries extra weight for self-employed borrowers. Unlike traditional employees, self-employed Canadians face unique mortgage qualification challenges that make refinancing more complex and costly. Understanding the Self-Employed Variable Rate Lock-In Strategy: Should You Switch to 3.45%-3.95% Fixed Before Mid-2026 Rate Hikes? requires analyzing current market conditions, your personal financial situation, and the hidden costs that many borrowers overlook.

Key Takeaways

✅ Bond markets are pricing in potential rate hikes for late 2026, despite the Bank of Canada’s current 2.25% hold—creating a narrow window for advantageous rate locks

💰 Current fixed rates (3.95%-4.25%) represent a premium of approximately 0.50%-0.80% over variable rates, but this gap may close rapidly if predicted hikes materialize

📊 Self-employed borrowers face higher switching costs due to income verification requirements, making the lock-in decision more consequential than for traditional employees

⚖️ Break-even analysis is critical—calculate how long it takes for interest savings to offset refinancing costs, with a target break-even of 24 months or less[2]

🎯 Your risk tolerance and cash flow stability should drive the decision more than rate predictions alone, especially given the income variability inherent in self-employment

Understanding the Current Rate Environment and Mid-2026 Outlook

The mortgage rate landscape in 2026 presents a complex picture for borrowers trying to time their lock-in decisions. While the Bank of Canada maintains its benchmark rate at 2.25%, several economic indicators suggest this stability may be temporary.

What’s Driving Rate Expectations?

Current market positioning shows variable mortgage rates ranging from 3.45% to 3.75% for well-qualified borrowers, while 5-year fixed rates sit between 3.95% and 4.25%. This spread of approximately 0.50%-0.80% represents the “insurance premium” borrowers pay for rate certainty[3].

Bond markets—often considered leading indicators of future rate movements—are pricing in potential increases for the second half of 2026. This forward-looking behavior suggests that institutional investors anticipate either:

- 📈 Persistent inflation requiring monetary policy tightening

- 💼 Stronger-than-expected economic growth

- 🌍 International rate pressures from other central banks

- 🏦 Credit market conditions demanding higher yields

According to industry forecasts, if rates do rise, mortgage rates could move into the 5.9% to 6.3% range by late 2026 or early 2027, though this represents a different market context than current Canadian conditions[5].

The Self-Employed Factor

For self-employed borrowers, understanding mortgage qualification requirements adds another layer to the timing decision. Unlike traditional employees who can quickly provide T4 slips and employment letters, self-employed individuals typically need:

- Two years of Notice of Assessments (NOAs) from the Canada Revenue Agency

- Business financial statements and tax returns

- Proof of business continuity and stable income streams

- Higher credit scores (often 680+ for best rates)

- Larger down payments in some cases

This documentation burden means switching from variable to fixed isn’t a quick process—it can take 4-8 weeks to gather documentation, get approval, and complete the switch. This timeline matters when rates are moving.

Rate Lock Windows: When Should You Act?

The timing of your rate lock decision depends heavily on how close you are to needing the funds or completing your switch. According to mortgage timing guidelines:

0-30 days until closing: Locking is strongly recommended because you have insufficient time to recover from sudden rate jumps[4]. For self-employed borrowers already in the approval process, this is non-negotiable.

31-60 days until closing: You have some flexibility, but should monitor major economic releases and Bank of Canada announcements closely[4]. This window requires active management and a backup plan.

61-90 days until closing: Floating can be reasonable only if you can afford potential rate increases and are prepared to lock quickly if conditions change[4]. Self-employed borrowers should factor in their longer documentation timelines.

The Self-Employed Variable Rate Lock-In Strategy: Unique Considerations

Self-employed Canadians face distinct challenges when evaluating whether to lock in variable rates. These considerations go beyond simple rate comparisons and touch on the fundamental differences in how lenders assess self-employed income.

Income Verification Complexity

When you’re self-employed, your stated income and your qualifying income are often very different. Lenders typically use one of two methods:

Traditional Income Verification requires averaging your net business income (after expenses) over two years. If your income has been growing, this method might understate your current earning capacity. Conversely, if you’ve had a strong year followed by a weaker one, your average could still look favorable.

Stated Income Programs are available through some lenders for self-employed borrowers with strong credit (720+) and larger down payments (35%+), but these programs typically come with rate premiums of 0.50%-1.25% above standard rates.

This complexity means that switching from variable to fixed might trigger a full re-qualification, potentially at a different rate than initially quoted if your income documentation doesn’t support the original approval amount.

The Break Fee Trap for Self-Employed Borrowers

One of the most overlooked aspects of the Self-Employed Variable Rate Lock-In Strategy: Should You Switch to 3.45%-3.95% Fixed Before Mid-2026 Rate Hikes? is the penalty for breaking a fixed-rate mortgage early.

Variable-rate mortgages typically charge three months’ interest as a penalty for early termination. On a $500,000 mortgage at 3.50%, that’s approximately $4,375.

Fixed-rate mortgages use the Interest Rate Differential (IRD) calculation, which can be substantially higher. If you lock in at 4.00% today and rates drop to 3.00% next year, your penalty on that same $500,000 mortgage could exceed $15,000-$20,000 depending on the term remaining.

As one mortgage expert notes: “Losing your financial agility can cost you thousands of dollars, completely wiping out any interest savings you engineered by fixing”[1]. This is particularly relevant for self-employed individuals whose business needs may require accessing home equity or refinancing on shorter notice than traditional employees.

Cash Flow Stability Assessment

Self-employed income often fluctuates more than traditional employment income. Before locking into a higher fixed rate, honestly assess:

- Seasonal income patterns in your business

- Contract renewal certainty for consultants and freelancers

- Economic sensitivity of your industry

- Emergency fund adequacy (self-employed individuals should maintain 6-12 months of expenses)

If your business faces potential disruption or you’re planning major changes, the flexibility of a variable rate might outweigh the security of a fixed rate, even if rates rise moderately. The ability to break a variable mortgage with only three months’ interest penalty provides valuable optionality.

Alternative Lender Considerations

Many self-employed borrowers work with alternative lenders who specialize in self-employed mortgages. These lenders often have different rate structures and lock-in options than traditional banks.

B-lenders and private lenders may offer:

- More flexible income verification

- Faster approval processes

- Different penalty structures

- Potentially higher rates but easier qualification

Understanding your lender’s specific policies on converting from variable to fixed is essential. Some lenders allow seamless conversions; others require full re-qualification or charge conversion fees.

Calculating Your Personal Break-Even Point

The mathematical foundation of your lock-in decision rests on calculating when the costs of switching are recovered through interest savings (or avoided costs). This break-even analysis is particularly important for self-employed borrowers who face higher transaction costs.

The Break-Even Formula

Your break-even point answers this question: How many months until my costs are recovered?

The basic calculation:

Break-Even Period = Total Switching Costs ÷ Monthly Payment Difference

For refinancing borrowers specifically, industry guidance suggests you should “calculate your break-even point—how many months until your interest savings offset your refinance closing costs—and lock when rates drop enough that your break-even occurs within 24 months”[2].

Real-World Example: The Lock-In Decision

Let’s examine a typical self-employed borrower scenario:

Current Situation:

- Mortgage balance: $600,000

- Current variable rate: 3.50%

- Current monthly payment: $2,694

- Years remaining: 20 years

Fixed Rate Option:

- Fixed rate offered: 4.10%

- New monthly payment: $2,833

- Monthly payment increase: $139

Switching Costs:

- Legal fees: $800

- Appraisal: $400

- Lender administration: $350

- Total costs: $1,550

Break-Even Calculation:

If rates stay the same: $1,550 ÷ $139 = 11.2 months to break even on the switch costs alone.

But the real question is: What if rates rise?

If the Bank of Canada raises rates by 0.50% in late 2026 (bringing your variable rate to 4.00%), your variable payment would become $2,788—nearly matching the fixed rate payment. In this scenario, locking in at 4.10% would have cost you only the switching fees and a small premium for peace of mind.

If rates rise by 1.00% (variable rate becomes 4.50%), your payment jumps to $2,942—$109 more per month than the fixed option. Over the remaining term, this represents substantial savings for having locked in.

Scenario Planning Table

| Rate Change | Variable Payment | Fixed Payment | Monthly Difference | 5-Year Impact |

|---|---|---|---|---|

| No change (3.50%) | $2,694 | $2,833 | -$139 (lose) | -$8,340 |

| +0.25% (3.75%) | $2,741 | $2,833 | -$92 (lose) | -$5,520 |

| +0.50% (4.00%) | $2,788 | $2,833 | -$45 (lose) | -$2,700 |

| +0.75% (4.25%) | $2,836 | $2,833 | +$3 (win) | +$180 |

| +1.00% (4.50%) | $2,883 | $2,833 | +$50 (win) | +$3,000 |

| +1.50% (5.00%) | $2,979 | $2,833 | +$146 (win) | +$8,760 |

This table illustrates that you need rates to rise by approximately 0.75% before the fixed-rate lock-in becomes financially advantageous over five years.

Factors That Change Your Break-Even

Several variables can significantly impact your break-even calculation:

Loan Amount Changes 🏠 Increasing your loan amount or changing your down payment percentage directly affects your locked rate. Reducing a down payment from 20% to 15% typically carries a 0.125% to 0.25% higher rate[2], which changes the entire calculation.

Lock Period Extensions ⏰ Secure a lock period that provides “adequate buffer beyond your expected closing date—adding 10 to 15 days of cushion to your expected timeline often prevents expensive last-minute extensions”[2]. For self-employed borrowers whose documentation gathering can be unpredictable, this buffer is essential.

Income Documentation Delays 📄 If your accountant is delayed in preparing financial statements or your Notice of Assessment is held up, you might need to extend your rate lock, which typically costs 0.125%-0.25% per 30-day extension.

Property Appraisal Results 📊 If your property appraises lower than expected, you might need to increase your down payment or accept a higher rate, both of which affect your break-even timeline.

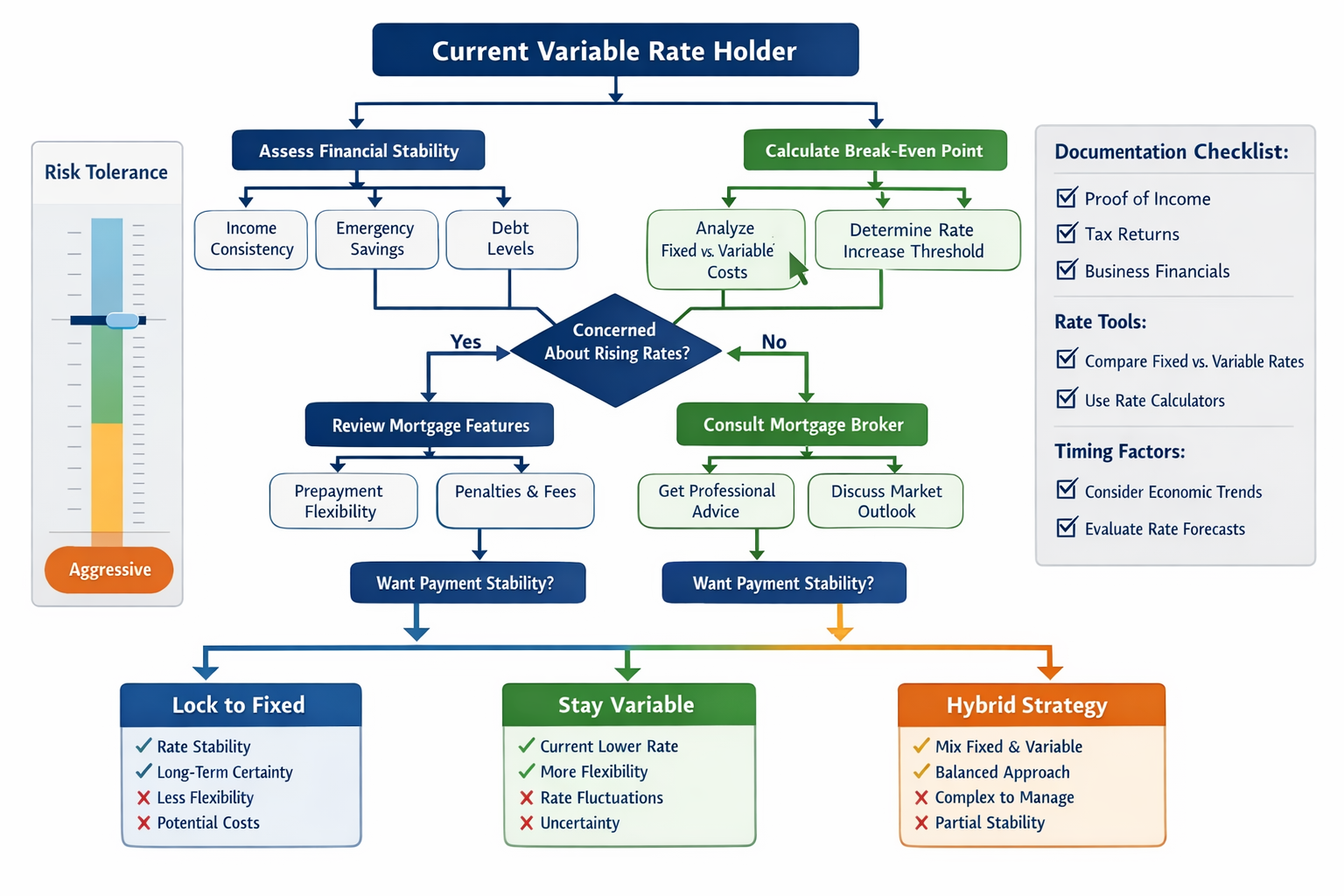

Making Your Decision: A Framework for Self-Employed Borrowers

Armed with market analysis and break-even calculations, you need a structured decision framework. The Self-Employed Variable Rate Lock-In Strategy: Should You Switch to 3.45%-3.95% Fixed Before Mid-2026 Rate Hikes? ultimately depends on your unique circumstances, risk tolerance, and business outlook.

The Risk Tolerance Assessment

Your decision should start with an honest evaluation of your financial resilience:

Lock in now if you:

- ✅ Operate in an economically sensitive industry with uncertain income

- ✅ Have limited emergency reserves (less than 6 months of expenses)

- ✅ Carry other variable-rate debt that would compound rate-increase impacts

- ✅ Value payment certainty and budgeting predictability highly

- ✅ Are approaching retirement or planning to reduce work hours

- ✅ Have a history of stress when markets are volatile

Stay variable if you:

- ✅ Maintain 12+ months of emergency reserves

- ✅ Have stable, diversified income streams

- ✅ Can absorb payment increases of 20-30% without lifestyle changes

- ✅ Believe rates will remain stable or decline

- ✅ Want to preserve financial flexibility for business opportunities

- ✅ Have a high risk tolerance and can handle market uncertainty

The Hybrid Strategy: Best of Both Worlds?

Some lenders offer split mortgages that divide your principal between fixed and variable portions. This approach provides:

- 🔒 Partial protection against rate increases

- 📈 Partial benefit if rates decline or stay low

- ⚖️ Balanced risk exposure that suits moderate risk tolerance

For example, you might lock in 60% of your mortgage at 4.00% fixed and keep 40% at 3.50% variable. If rates rise to 4.50%, your blended rate becomes approximately 4.20%—better than full variable but worse than full fixed. If rates fall to 3.00%, your blended rate drops to 3.60%—better than full fixed but worse than full variable.

This strategy particularly suits self-employed borrowers who want some certainty for budgeting while maintaining flexibility for business opportunities.

Timing Your Lock-In Decision

Based on current market conditions in early 2026, consider these timing strategies:

Immediate Lock (Next 30 Days) is appropriate if:

- Bond yields are rising sharply

- Bank of Canada rhetoric shifts toward tightening

- Your business income is declining or uncertain

- You’re within 60 days of mortgage renewal

- Fixed-variable spread narrows to 0.40% or less

Strategic Wait (60-90 Days) makes sense if:

- Economic data shows cooling inflation

- Bank of Canada maintains dovish language

- Your business is growing and cash flow is strong

- Fixed-variable spread exceeds 0.80%

- You have rate lock flexibility with your lender

Active Monitoring (Ongoing) requires:

- Setting rate alerts with your mortgage broker

- Reviewing Bank of Canada announcements

- Tracking bond market movements

- Maintaining pre-approval readiness

- Having documentation prepared for quick action

Questions to Ask Your Mortgage Professional

Before making your final decision, ensure you have clear answers to:

- What is the exact all-in cost to switch from variable to fixed, including any hidden fees?

- What documentation do you need from me, and how long will gathering it take?

- What is the Interest Rate Differential calculation your lender uses for break penalties?

- Can I lock in a portion of my mortgage while keeping the rest variable?

- What rate lock period do you recommend given my documentation timeline?

- Are there any rate-drop provisions if rates fall after I lock but before closing?

- What happens if my income documentation doesn’t support the full amount?

Understanding how to choose the right mortgage lender is particularly important for self-employed borrowers who need specialists familiar with alternative income verification methods.

The Cost of Inaction

While deciding whether to lock in, remember that not deciding is itself a decision. Staying on your current variable rate is an active choice to:

- Accept potential payment increases

- Bet on stable or declining rates

- Prioritize flexibility over certainty

- Maintain lower break penalties

This choice can be perfectly rational if it aligns with your risk assessment and financial capacity. The danger lies in passive indecision—failing to actively choose either path and being caught off-guard by rate movements.

Special Considerations for Different Self-Employment Types

Your specific type of self-employment affects your lock-in strategy:

Incorporated Business Owners 🏢

- May have more income documentation complexity

- Can potentially adjust salary/dividend mix for qualification

- Should consider business cash flow needs before committing to higher payments

- May benefit from corporate-held mortgages with different rate structures

Freelancers and Consultants 💼

- Often face the most income volatility

- Should prioritize emergency fund adequacy before locking in

- May benefit from variable rates if contract income is trending upward

- Need to consider contract renewal timing in lock-in decisions

Commission-Based Professionals 📊

- Income averaging can help or hurt depending on recent performance

- Should lock in during strong income years to maximize qualification

- May face seasonal considerations in timing applications

- Benefit from working with specialized mortgage professionals

Conclusion

The Self-Employed Variable Rate Lock-In Strategy: Should You Switch to 3.45%-3.95% Fixed Before Mid-2026 Rate Hikes? is not a one-size-fits-all decision. While bond markets are pricing in potential rate increases for late 2026, the right choice depends on your unique financial situation, risk tolerance, and business outlook.

For self-employed Canadians, the decision carries additional weight due to more complex qualification requirements, higher switching costs, and the need to balance business flexibility with personal financial security. The current environment—with variable rates at 3.45%-3.75% and fixed rates at 3.95%-4.25%—presents a relatively narrow spread that could close quickly if predicted rate hikes materialize.

Your Action Plan

Within the next 7 days:

- 📞 Contact a mortgage broker specializing in self-employed borrowers

- 📊 Gather your last two years of tax returns and NOAs

- 🧮 Calculate your personal break-even point using current rate quotes

- 💰 Assess your emergency fund and cash flow stability

Within the next 30 days:

- 📈 Get pre-qualified for fixed-rate options to understand your true rate

- ⚖️ Compare total costs of switching versus staying variable

- 🎯 Determine your risk tolerance and payment flexibility

- 📝 Make an informed decision or set triggers for future action

Ongoing monitoring:

- 📰 Track Bank of Canada announcements and economic indicators

- 💹 Monitor bond yields and rate forecasts

- 🔄 Review your decision quarterly or when major economic shifts occur

- 📞 Maintain communication with your mortgage professional

Remember, the goal isn’t to perfectly time the market—it’s to make a decision that aligns with your financial capacity, business needs, and peace of mind. Whether you choose to lock in now, wait strategically, or adopt a hybrid approach, make it an active, informed choice rather than a passive default.

The mortgage market in 2026 offers both opportunities and risks. By understanding your unique position as a self-employed borrower and following a structured decision framework, you can navigate these waters with confidence. For personalized guidance tailored to your specific situation, consult with a mortgage professional who understands the nuances of self-employed mortgage qualification and can help you make the choice that’s right for you.

References

[1] Watch – https://www.youtube.com/watch?v=T2jIiwv-DHA

[2] Mortgage Rate Locks In Your Complete Guide To Timing Costs And Protection Strategies – https://www.amerisave.com/learn/mortgage-rate-locks-in-your-complete-guide-to-timing-costs-and-protection-strategies

[3] Should You Choose A Variable Or Fixed Rate – https://www.truenorthmortgage.ca/blog/should-you-choose-a-variable-or-fixed-rate

[4] March 2026 Fed Meeting Mortgage Rate Lock Guide – https://www.bartonhillsmortgage.com/index.php/blog/post/221/march-2026-fed-meeting-mortgage-rate-lock-guide

[5] Mortgage Rate Trends 2026 – https://trussfinancialgroup.com/blog/mortgage-rate-trends-2026