March 18, 2026

Private Mortgages for Toronto Newcomers: Overcoming CMHC Barriers with Equity-Based Financing in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Every year, thousands of skilled, wealthy newcomers arrive in Toronto — professionals, entrepreneurs, and investors with significant overseas assets — only to be turned away by Canadian banks and CMHC-insured lenders because they lack a T4 slip or a local credit history. In 2026, Private Mortgages for Toronto Newcomers: Overcoming CMHC Barriers with Equity-Based Financing has emerged as the most viable solution to this frustrating gap — offering fast, asset-based approvals that bypass traditional income verification hurdles entirely.

Key Takeaways 📌

- CMHC’s February 2026 rule changes made it significantly harder for newcomers without Canadian income history to qualify for insured mortgages.

- Private lenders approve based on property equity (30–40%), not credit scores or employment records — making them ideal for asset-rich newcomers.

- Approval timelines are dramatically faster: 5–10 days with private lenders versus 3–6 months for CMHC MLI Select. [3]

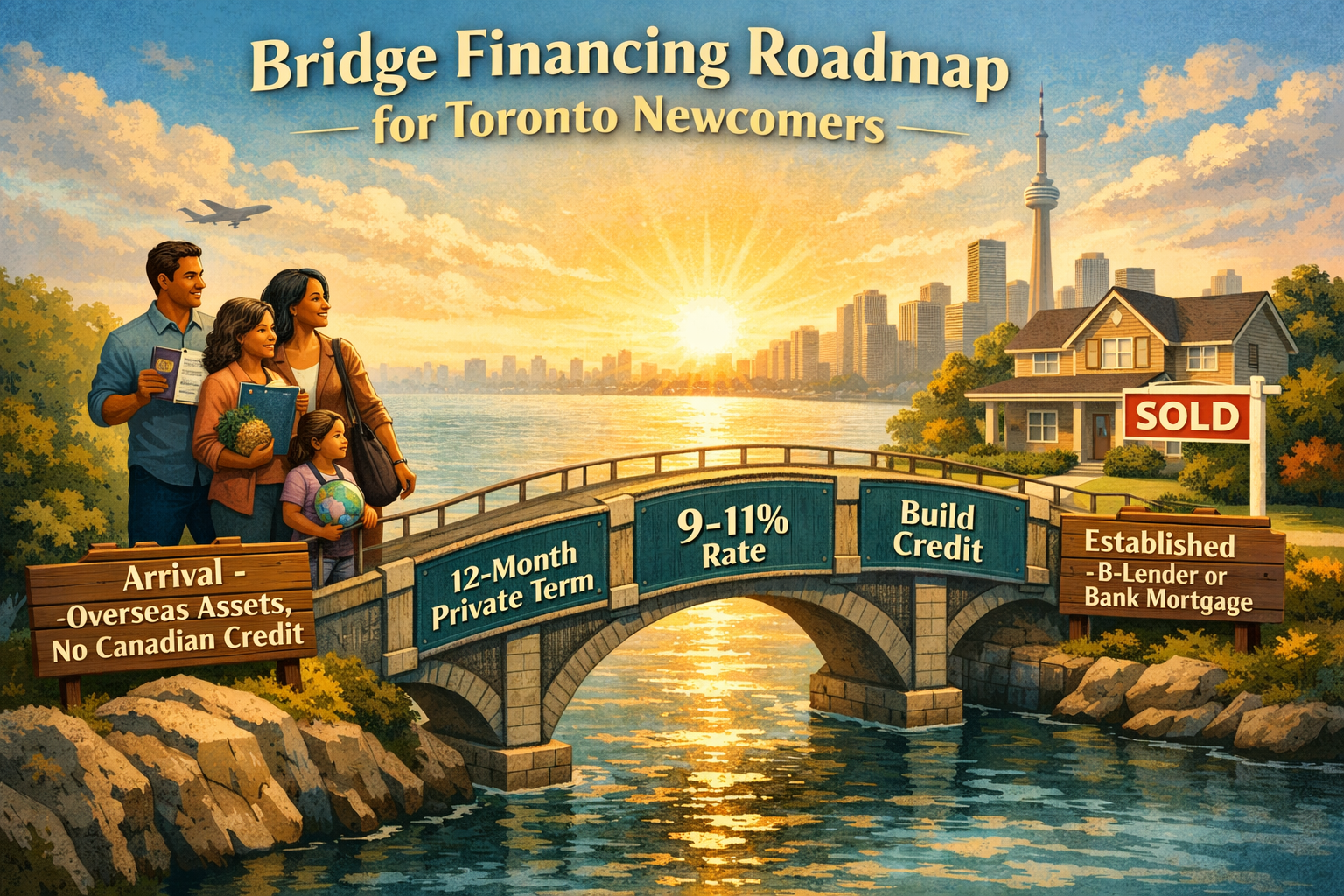

- Private mortgages are a bridge, not a destination — most newcomers refinance to B-lenders or banks within 12–24 months after building Canadian credit.

- Toronto mortgage arrears have quadrupled from post-pandemic lows, amplifying demand for flexible, equity-based financing solutions. [4]

Why CMHC Barriers Are Blocking Toronto Newcomers in 2026

Canada’s housing insurance system was designed for established residents with verifiable Canadian income. For newcomers, it has become a significant obstacle.

The February 2026 CMHC Overhaul

On February 12, 2026, CMHC overhauled its MLI Select program in a sweeping policy change. Key impacts included:

- 📈 Raised insurance premiums across most property categories

- 🚫 Rental income restrictions that disqualify properties with non-stabilized tenancy

- ❌ Elimination of multi-title property bundling, a strategy many newcomer investors relied on

- 📋 Stricter scoring thresholds — MLI Select now requires 100+ points, demanding documented Canadian income history [2]

These changes were driven by Basel 3 capital standards and federal regulatory pressure. The result? Newcomers with substantial overseas wealth but no Canadian T4 slips are effectively locked out of CMHC-insured products. [2]

The Credit Score Catch-22

Conventional banks demand a 680+ credit score, strict T4 verification, and 60–75% loan-to-value (LTV) ratios. For someone who arrived in Canada six months ago — regardless of their net worth — these requirements are nearly impossible to meet immediately.

Understanding how credit scores affect the mortgage approval process in Canada helps explain why even financially strong newcomers get rejected at traditional institutions.

💬 “The system wasn’t built for the globally mobile professional. Private lending fills that gap by asking the right question: not ‘what did you earn last year?’ but ‘what equity do you bring today?'” — Everything Mortgages, March 2026 [2]

How Private Mortgages for Toronto Newcomers Work: Overcoming CMHC Barriers with Equity-Based Financing in 2026

Private mortgages operate on a fundamentally different logic than institutional lending. Instead of evaluating borrower income, they evaluate property equity.

The Equity-First Approval Model

Private lenders in Ontario typically require:

| Requirement | Private Lender | CMHC MLI Select | Conventional Bank |

|---|---|---|---|

| LTV Ratio | 75–80% | 85–95% | 60–75% |

| Credit Score | Flexible / Not required | 650+ | 680+ |

| Income Verification | Minimal / Asset-based | Full T4 required | Full T4 required |

| Approval Time | 5–10 days | 3–6 months | 4–8 weeks |

| Interest Rate | 9–12% | 3.5–4.25% | 5–7% |

| Lender Fees | 1–3% | 0.5–1% | Minimal |

For a newcomer with a 30–40% down payment on a Toronto property, private lenders will approve based almost entirely on that equity position. [2]

Why This Works for Newcomers Specifically

Many newcomers arrive with:

- ✅ Significant savings or liquidated overseas assets

- ✅ Strong professional backgrounds

- ✅ Clear intent to establish Canadian roots

- ❌ No Canadian credit file

- ❌ No Canadian employment history (yet)

Private lenders recognize that asset wealth is real wealth. A newcomer putting $400,000 down on a $1,000,000 Toronto property represents a low-risk loan — regardless of what their Canadian credit report shows.

For those wondering how easy it is to get a private mortgage, the answer for equity-rich newcomers in 2026 is: considerably easier than any other option.

The 2026 Market Context: Rising Arrears, Rising Demand

Toronto’s mortgage market is under significant stress. CMHC data shows mortgage arrears have quadrupled from post-pandemic lows, reaching 0.22% in Q1 2025 and projected to climb through 2026. [4] The Bank of Canada held rates at 2.25% as of March 2026, providing some stability, but renewal shocks remain severe — payments on $500K–$700K loans could rise 20–40% at renewal. [4]

This environment is pushing more borrowers — including newcomers — toward flexible private equity financing as institutional lenders tighten standards further. [6]

The Strategic Bridge: From Private to Mainstream Financing

The smartest newcomers don’t view private mortgages as a permanent solution. They use them as a deliberate bridge to conventional financing.

A Typical 24-Month Newcomer Pathway

Phase 1 (Months 1–12): Private Mortgage

- Secure property with 30–40% equity

- Private lender approves in 5–10 days at 9–11% [3]

- Begin building Canadian credit (secured cards, utility bills, etc.)

- Establish Canadian employment or business income documentation

Phase 2 (Months 12–24): B-Lender Refinance

- With 12 months of Canadian credit history, qualify for B-lender rates of 6.5–9%

- B-lenders offer moderate income checks and 1–2 week approvals [6]

- Significantly reduce interest costs

Phase 3 (Year 2+): Conventional Bank or CMHC

- With established credit and income history, qualify for prime rates

- Access full institutional mortgage products

Working with a knowledgeable mortgage broker in Toronto is essential for navigating this multi-phase strategy effectively. Brokers have access to dozens of private lenders and can match newcomers with the right product at each stage.

Understanding Private Mortgage Costs

Be clear-eyed about the costs involved:

- Interest rates: 9–12% annually

- Lender fees: 1–3% of the loan amount

- Broker fees: Typically 1–2%

- Legal fees: Standard closing costs apply

- Short terms: 6–24 months (designed to be temporary)

These costs are real, but they must be weighed against the alternative — renting while Toronto property values continue to move, or missing a purchase opportunity entirely. For many newcomers, the equity gained during a 12-month private term outweighs the higher interest cost. [2]

Alternatives Worth Considering

Before committing to private financing, newcomers should also explore:

- Shared equity mortgages: A partner contributes to the down payment, reducing private loan size — though this dilutes ownership [2]. Learn more about how shared equity mortgages work in Canada.

- New job mortgage options: If employment has recently started, some lenders have pathways — see getting a mortgage in Canada with a new job.

- No-income mortgage strategies: Explore how to get a mortgage in Canada without traditional income documentation.

For a deeper understanding of the private lending landscape, how private mortgages work in Ontario provides essential foundational knowledge before approaching lenders.

Conclusion: A Clear Path Forward for Toronto Newcomers in 2026

The barriers CMHC has erected in 2026 are real — but they are not the end of the road. Private Mortgages for Toronto Newcomers: Overcoming CMHC Barriers with Equity-Based Financing in 2026 represents a proven, strategic pathway for asset-rich individuals who simply haven’t had time to build a Canadian financial footprint.

Actionable Next Steps 🚀

- Calculate your equity position — Determine how much you can put down. 30–40% opens private lending doors immediately.

- Gather overseas asset documentation — Bank statements, property deeds, and investment records strengthen your application.

- Consult a licensed mortgage broker — Brokers with private lending networks can match you with the right lender in days, not months.

- Start building Canadian credit immediately — Open a secured credit card the week you arrive. Every month counts toward your B-lender transition.

- Plan your exit strategy — Know your 12–24 month refinancing target before you sign a private mortgage.

- Review current private mortgage rates — Check the best private mortgage rates in Ontario to benchmark what you should expect to pay.

Toronto’s housing market will not wait. With the right strategy, newcomers with equity can own property in Canada’s most competitive city — starting today.

References

[1] Watch – https://www.youtube.com/watch?v=PMEJjgmzh78

[2] Toronto Private Mortgages For Newcomer Investors Navigating 2026 Cmhc Restrictions And Equity Pathways – https://everythingmortgages.ca/blog/toronto-private-mortgages-for-newcomer-investors-navigating-2026-cmhc-restrictions-and-equity-pathways/

[3] Private Mortgages Fueling Torontos 2026 Garden Suite Boom Financing Legal Basement Rentals Amid Rent Recovery – https://everythingmortgages.ca/blog/private-mortgages-fueling-torontos-2026-garden-suite-boom-financing-legal-basement-rentals-amid-rent-recovery/

[4] Watch – https://www.youtube.com/watch?v=lSQJu2PTr7M

[6] Private Mortgages For Toronto Homeowners Battling 450 Delinquency Surge Survival Tactics In March 2026 – https://everythingmortgages.ca/blog/private-mortgages-for-toronto-homeowners-battling-450-delinquency-surge-survival-tactics-in-march-2026/

[10] Housing Market Outlook – https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/market-reports/housing-market/housing-market-outlook