March 18, 2026

Garden Suite Financing Boom: Private Mortgages Fueling Toronto’s 2026 Accessory Dwelling Unit Surge

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto homeowners are quietly transforming their backyards into income-generating assets — and private lenders are making it happen faster than ever. The Garden Suite Financing Boom: Private Mortgages Fueling Toronto’s 2026 Accessory Dwelling Unit Surge is reshaping how Canadians think about property investment, rental income, and creative mortgage strategies. With regulatory barriers falling, federal loan programs expanding, and rental recovery on the horizon, 2026 has become the defining year for accessory dwelling unit (ADU) development across the city. [3]

Key Takeaways 🏡

- Private mortgages now fund ~20% of Ontario’s mortgage market, up from 8–12% nationally five years ago, largely driven by garden suite investors who need fast, flexible capital [3]

- New regulations (Ontario Reg. 462/24) make ~80% of Toronto residential lots eligible for garden suites or secondary suites [3]

- Federal Secondary Suite Loans of up to $80,000 at 2% interest are available but insufficient alone — private bridge financing fills the gap [3]

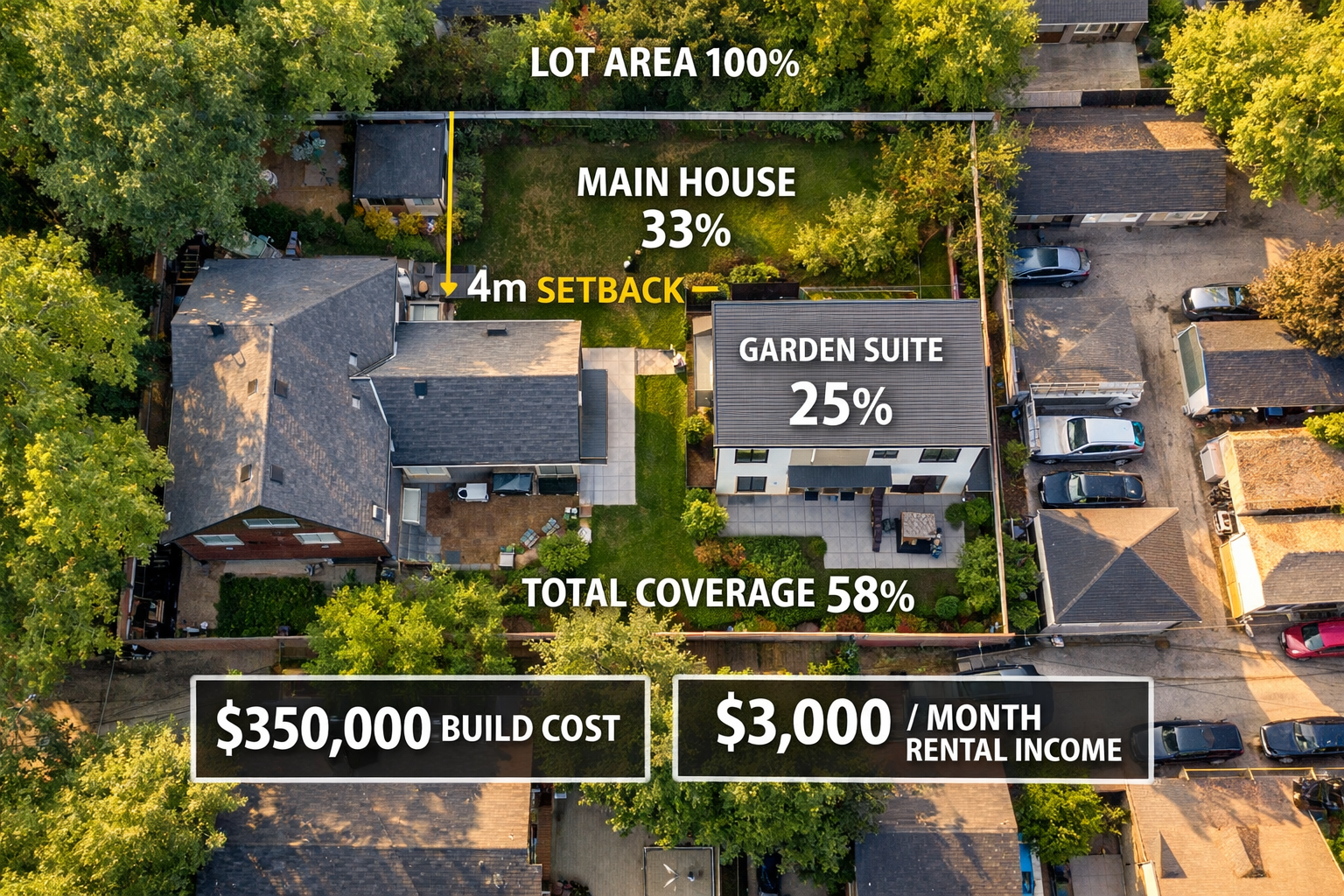

- Two-storey garden suites (~1,200 sq ft, ~$350,000 build) can generate $3,000/month in rent, with most capital recovered via 80% LTV refinancing [10]

- Private bridge mortgages (6–12 months, 8–12% rates) offer 5–10 day approvals vs. 30–60 days for banks, making them the preferred tool for ADU investors [3]

Why Toronto’s Garden Suite Market Exploded in 2026

Several forces converged to ignite the Garden Suite Financing Boom in Toronto. Understanding each one helps explain why 2026 is considered a pivotal year for ADU development. [3]

Regulatory Changes That Opened the Floodgates

Ontario Regulation 462/24, enacted in November 2024, fundamentally rewrote the rules for backyard housing. Key changes include:

- 📐 Reduced separation from the main house: down to 4 meters (from 5–7.5 meters)

- 🏗️ Removed angular plane restrictions, allowing taller, more functional structures

- 📊 Increased lot coverage to 45%, unlocking approximately 80% of Toronto’s residential properties for garden or secondary suites [3]

In July 2025, the City of Toronto released “Made in Toronto” pre-approved garden and laneway suite plans, cutting design and permit costs by $15,000–$30,000 per project. This dramatically accelerated approvals and reduced the financial risk of starting a build. [3]

Federal Funding That Sweetens the Deal

The Canada Secondary Suite Loan Program doubled its maximum loan to $80,000 at 2% interest over 15 years, effective January 2025. This low-cost federal funding acts as a strong foundation — but it rarely covers the full cost of a garden suite build, which typically runs $250,000–$400,000. [3]

That gap is precisely where private mortgage financing steps in.

💬 “2026 is the year where regulation, financing, and rental demand have all aligned. Investors who act now will be positioned for the 2027–2028 rent rebound.” — Manzeel Patel, Mortgage Broker, Everything Mortgages [3]

How Private Mortgages Are Powering the ADU Surge

The Garden Suite Financing Boom: Private Mortgages Fueling Toronto’s 2026 Accessory Dwelling Unit Surge isn’t just a trend — it’s a structural shift in how Canadians finance non-traditional real estate projects. Here’s why private lenders have become the go-to solution.

Banks vs. Private Lenders: A Clear Comparison

| Feature | Bank / A-Lender | Private Lender |

|---|---|---|

| Approval Time | 30–60 days | 5–10 days |

| Rental Income Considered | Rarely | Often flexible |

| Mid-Renovation Funding | Almost never | Yes |

| Rate Range | Prime + 0.5–2% | 8–12% |

| ADU Appraisal Approach | Often undervalues | More accommodating |

| Income Verification | Strict | Flexible |

Banks frequently undervalue ADUs in appraisals and apply strict income verification rules that ignore projected rental income — making them a poor fit for garden suite investors. [2] Private lenders, by contrast, evaluate the asset’s potential, not just the borrower’s T4 slips.

For a deeper look at how private lending works in Ontario, see this complete guide to private mortgages in Ontario.

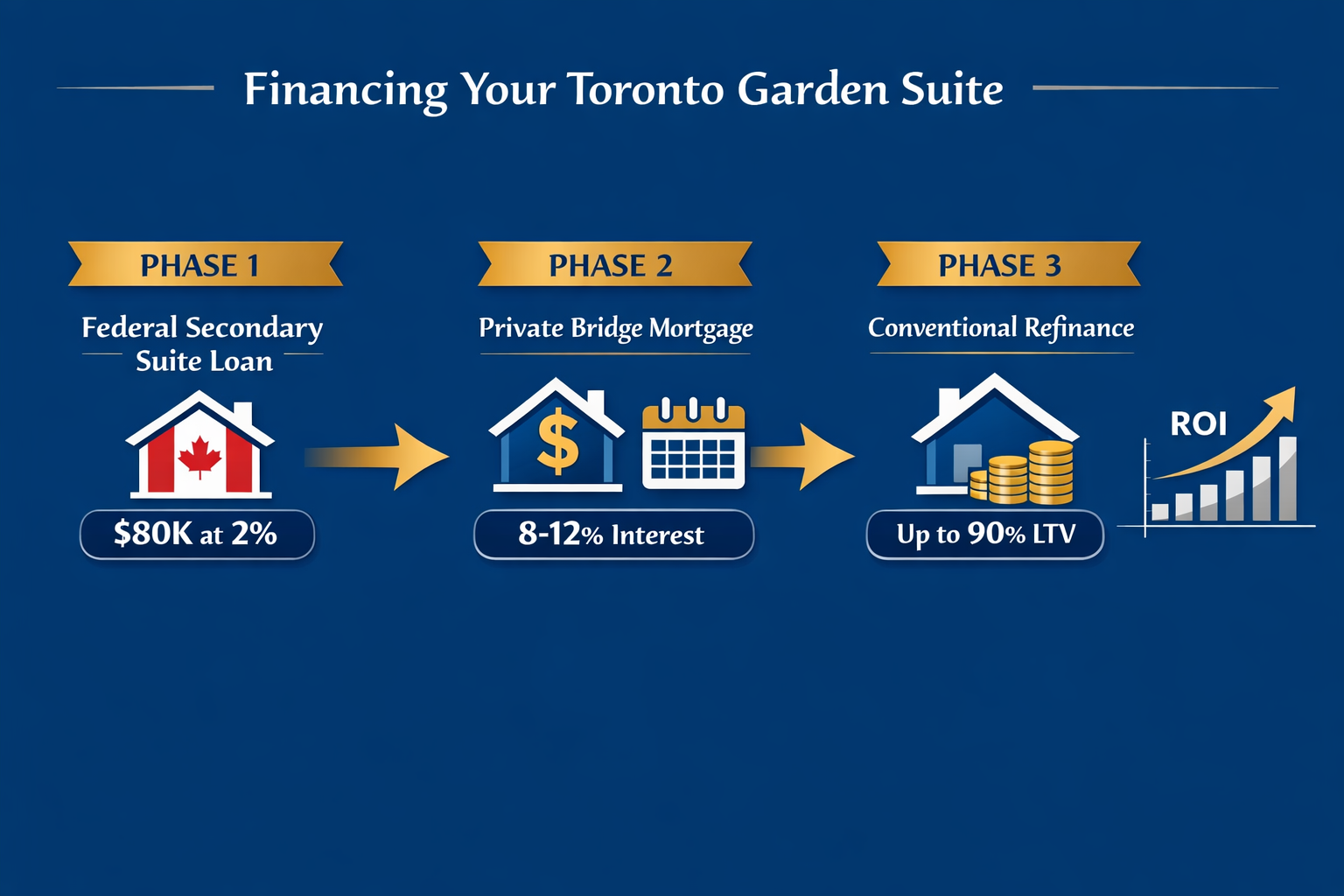

The Private Bridge Strategy: Build Now, Refinance Later

The most common financing approach in 2026 follows a three-phase model:

- Phase 1 — Federal Loan: Access up to $80,000 at 2% through the Canada Secondary Suite Loan Program

- Phase 2 — Private Bridge Mortgage: Secure 6–12 months of private financing at 8–12% to cover the construction gap

- Phase 3 — Conventional Refinance: Once the suite is complete and tenanted, refinance at up to 90% LTV (expanded from 80% in early 2025) with a 30-year amortization and a $2 million property cap [3]

This strategy allows investors to move quickly, complete the build, and then lock in lower long-term rates once the property’s value is proven. For guidance on making refinancing work in your favour, explore how 2026 rate forecasts could make refinancing a smart move for Toronto buyers.

Institutional Lenders Are Taking Notice

Even traditional lenders are beginning to adapt. EQ Bank launched a specialized garden suite financing product in October 2024, targeting laneway and garden suites specifically. [1] This signals that the private mortgage space is maturing — and that mainstream lenders are watching the ADU market closely.

Private mortgages now represent approximately 20% of Ontario’s mortgage market, up from 8–12% nationally just five years ago. [3] For those unfamiliar with this lending tier, the full guide to getting a mortgage with a private lender is an essential starting point.

ROI, Costs, and the 2026 Investment Case for Garden Suites

What Does a Garden Suite Actually Cost?

Build costs vary based on size, finishes, and site conditions. Here’s a realistic breakdown for a typical Toronto project:

| Cost Category | Estimated Range |

|---|---|

| Construction (per sq ft) | $250–$400 |

| Design & Permits (pre-approved plans) | $5,000–$15,000 |

| Site Preparation | $15,000–$30,000 |

| Total Build (typical) | $250,000–$400,000 |

| Two-Storey (~1,200 sq ft) | ~$350,000 |

Source: [9][10]

The City of Toronto’s pre-approved plans have been a game-changer for cost control, reducing design and permitting fees by up to $30,000 compared to custom designs. [3]

The Rental Income Equation

A two-storey garden suite (~1,200 sq ft) on a sub-$1 million Toronto lot can generate approximately $3,000/month in rent. [10] That’s $36,000 annually — a meaningful income stream for any homeowner.

CMHC and TD analysts project rental softening through 2026, followed by a gradual recovery in 2027–2028. [1] This means investors who complete builds now will be positioned to benefit from rising rents just as their suites hit the market. For a broader comparison of investment strategies, the condo vs. ADU investment breakdown offers valuable perspective.

Capital Recovery Through Refinancing

One of the most compelling aspects of the garden suite investment model is capital recovery:

- Build cost: ~$350,000

- Post-build property value increase: Significant (varies by lot and suite quality)

- Refinance at 80% LTV: Recovers most of the invested capital

- Net cost of rental income: Potentially very low after refinancing [10]

This approach — sometimes called the BRRRR strategy (Build, Rent, Refinance, Repeat) — is gaining traction among Toronto property investors. Those who want to understand how refinancing fits into long-term wealth building should review mortgage refinancing tips to save money.

Who Is Building Garden Suites in 2026?

The typical garden suite investor in 2026 falls into one of three profiles:

- 🏠 Long-term homeowners with significant equity who want rental income without selling

- 💼 Self-employed professionals seeking asset-backed income streams (often using flexible private financing)

- 👨👩👧 Multi-generational families creating in-law suites while adding property value

Self-employed borrowers in particular benefit from private mortgage flexibility. Learn more about self-employed mortgage options in Toronto for 2026.

Navigating the Garden Suite Financing Boom: Private Mortgages Fueling Toronto’s 2026 Accessory Dwelling Unit Surge

Key Risks to Understand Before You Build

The opportunity is real — but so are the risks. Investors should be aware of:

- ⚠️ Higher short-term costs: Private bridge rates of 8–12% add up during construction

- ⚠️ Appraisal gaps: Banks may still undervalue completed suites, complicating refinancing [2]

- ⚠️ Rental softening: CMHC projects continued softness through 2026 before recovery [1]

- ⚠️ Construction delays: Cost overruns can extend the private mortgage period

Practical Steps to Get Started

- ✅ Assess your lot eligibility under Ontario Reg. 462/24 (4-meter setback, 45% lot coverage)

- ✅ Apply for the Canada Secondary Suite Loan ($80,000 at 2%) as a low-cost foundation

- ✅ Consult a mortgage broker experienced in ADU financing to structure the bridge loan

- ✅ Use City of Toronto pre-approved plans to reduce design and permit costs

- ✅ Plan your exit strategy — know your refinancing timeline before you break ground

For those concerned about qualifying under non-traditional income scenarios, understanding how to get a second mortgage in Ontario may also open additional financing pathways.

Conclusion: Act Now or Wait for the Crowd

The Garden Suite Financing Boom: Private Mortgages Fueling Toronto’s 2026 Accessory Dwelling Unit Surge represents one of the most significant residential investment opportunities in Toronto’s recent history. Regulatory changes, federal funding, pre-approved city plans, and a maturing private lending market have all aligned in 2026 to make garden suite development more accessible than ever before.

The window is open — but it won’t stay quiet for long.

Investors who move now can complete builds ahead of the projected 2027–2028 rental recovery, recover capital through strategic refinancing, and generate long-term passive income from a fully legal, city-approved rental unit.

Actionable Next Steps 🚀

- Get a free mortgage assessment from a broker who specializes in ADU and private financing

- Check your lot eligibility using the City of Toronto’s updated zoning maps

- Stack your financing — combine the federal $80,000 loan with a private bridge mortgage

- Download pre-approved suite plans from the City of Toronto to cut upfront costs

- Model your ROI using realistic rental projections and a clear refinancing exit plan

The tools, the regulations, and the financing are all in place. The only question is whether to act now or watch from the sidelines.

References

[1] Finance – https://gardensuitehome.ca/finance/ [2] Adu Add Value To Home – https://tridacmortgages.com/blog/adu-add-value-to-home/ [3] Private Mortgages Fueling Torontos 2026 Garden Suite Boom Financing Legal Basement Rentals Amid Rent Recovery – https://everythingmortgages.ca/blog/private-mortgages-fueling-torontos-2026-garden-suite-boom-financing-legal-basement-rentals-amid-rent-recovery/ [9] Toronto Garden Suite Cost – https://bridge.broker/home-improvement/toronto-garden-suite-cost/ [10] Toronto Garden Suite 2026 Multiplex Strategy – https://www.elevatepartners.ca/resources/toronto-garden-suite-2026-multiplex-strategy/