March 22, 2026

Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

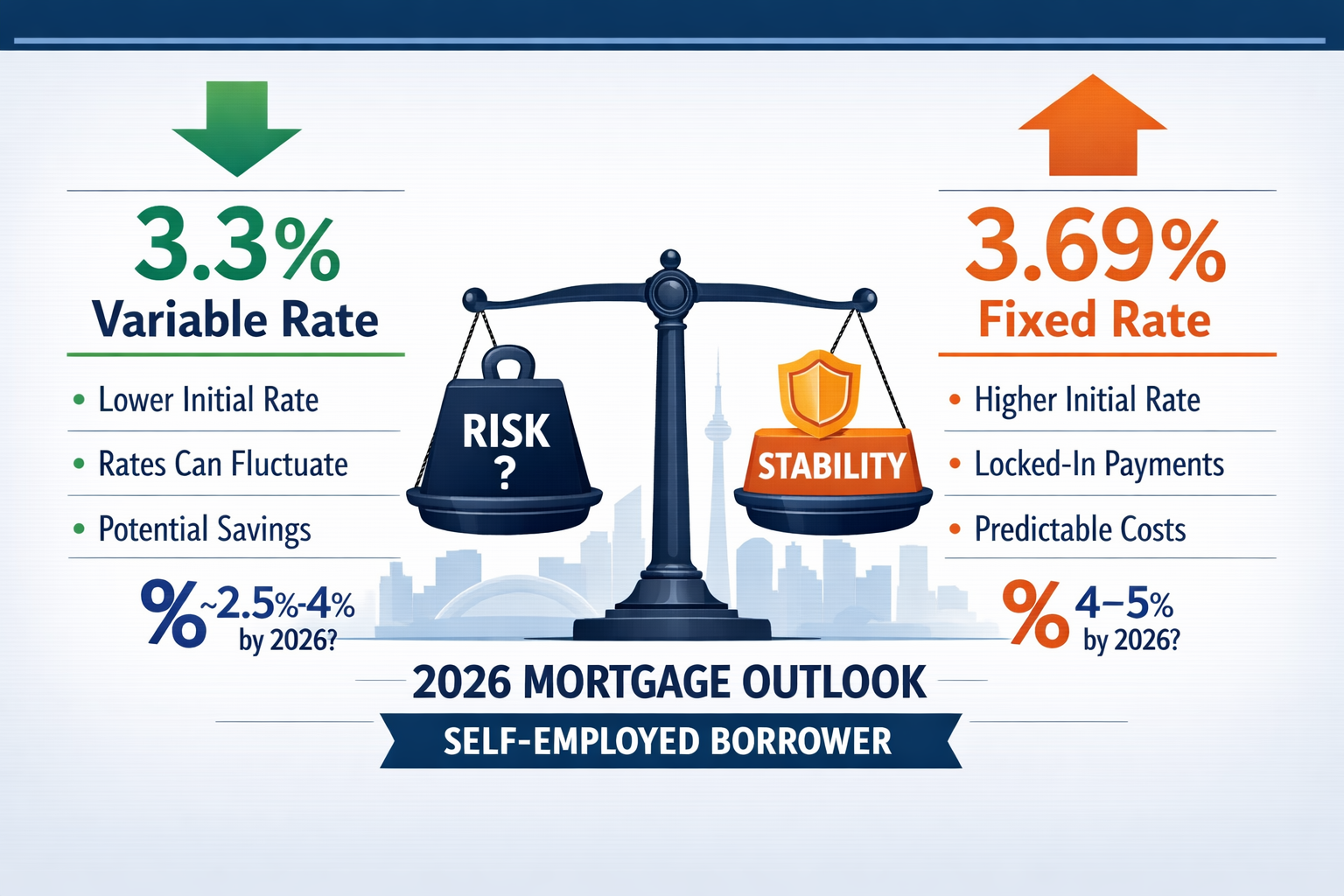

Self-employed borrowers in Toronto currently enjoying variable mortgage rates as low as 3.3% face a critical decision in 2026: should they lock in fixed rates now at 3.69%-4.03%, or wait and risk potential mid-year rate increases? With the Bank of Canada holding its overnight policy rate at 2.25% and conflicting forecasts from major banks, the Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes has never been more relevant. This comprehensive guide examines the unique challenges facing self-employed mortgage holders and provides actionable strategies for navigating the uncertain rate environment ahead.

Key Takeaways

- 🏦 Current Rate Advantage: Variable rates at 3.3%-3.45% remain below fixed rates at 3.69%-4.03%, but this gap may narrow by mid-2026

- 📊 Split Bank Consensus: Five of six major banks forecast rates staying at 2.25% through 2026, while Scotiabank predicts increases to 3.0% by year-end

- ⏰ Critical Timing Window: Self-employed borrowers should evaluate switching before Q3 2026 when inflation pressures and geopolitical risks could trigger rate hikes

- 💼 Self-Employed Considerations: Income documentation requirements and qualification challenges make early planning essential for successful rate switching

- 🎯 Strategic Lock-In: Locking in at 3.69%-3.85% now provides payment certainty versus risking 4.0%-4.5% rates if forecasted hikes materialize

Understanding the Current Rate Environment for Toronto’s Self-Employed Borrowers

The mortgage landscape in March 2026 presents both opportunities and challenges for self-employed professionals in Toronto. The Bank of Canada maintained its overnight policy rate at 2.25% on March 18, 2026, keeping the prime rate steady at 4.45%[2]. This stability has allowed variable mortgage rates to remain competitive, with qualified borrowers accessing rates as low as 3.3% as of March 21, 2026[5].

For self-employed borrowers, these rates represent a significant advantage compared to the 5-year fixed rates currently ranging from 3.69% to 4.03%[5]. However, the Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes requires understanding the broader economic context.

Current Rate Snapshot (March 2026)

| Mortgage Type | Current Rate Range | Prime Rate Discount |

|---|---|---|

| 5-Year Variable | 3.3% – 3.8% | 0.65 – 1.15 points |

| 3-Year Fixed | 3.69% – 4.3% | N/A |

| 5-Year Fixed | 3.69% – 4.03% | N/A |

The variable rate discount of 0.75-0.9 percentage points below prime remains stable[4][1], maintaining the attractiveness of variable products for borrowers who can tolerate payment uncertainty.

The Self-Employed Challenge

Self-employed borrowers face unique hurdles when considering rate switches. Unlike salaried employees, self-employed mortgage applicants must provide additional documentation, including:

- Two years of Notice of Assessments (NOAs) from the Canada Revenue Agency

- Business financial statements (profit and loss, balance sheets)

- Corporate tax returns (T2s for incorporated businesses)

- Proof of business continuity and client contracts

This documentation requirement means self-employed borrowers need more lead time to prepare for rate switches compared to traditional employees. Understanding self-employed mortgage rates in Toronto 2026 is essential for making informed decisions.

Expert Insight: “Self-employed borrowers should begin gathering income documentation at least 60-90 days before their intended switch date. Lenders scrutinize self-employed income more carefully, and any delays in documentation can mean missing favorable rate windows.”

Analyzing the 2026 Rate Forecast: Consensus vs. Outlier Predictions

The Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes depends heavily on understanding where rates are headed. The forecasts from Canada’s Big 6 banks reveal a fascinating split that creates both opportunity and risk.

The Majority Consensus (5 of 6 Banks)

BMO, CIBC, National Bank, RBC, and TD all forecast that the Bank of Canada’s overnight rate will remain at 2.25% throughout all of 2026[2][7]. This consensus suggests:

- Variable rates should remain stable near current 3.3%-3.8% levels

- Limited urgency to switch to fixed rates immediately

- Continued payment predictability for variable rate holders

The Scotiabank Outlier Forecast

Scotiabank diverges significantly from its peers, projecting the BoC rate will rise to 2.75% by October 2026 and reach 3.0% by year-end[1][2]. If this scenario materializes:

- Variable rates could climb to 3.85%-4.3% by Q4 2026

- Monthly payment increases of $150-$300 on a $500,000 mortgage

- Trigger rate concerns for borrowers already near their limits

Understanding trigger rates in variable mortgages becomes critical in this scenario, as payment shocks could force borrowers into difficult financial positions.

Fixed Rate Trajectory

The Big 6 banks forecast that Government of Canada 5-year bond yields will rise from approximately 2.80% at the start of 2026 to as high as 3.25% by year-end[2]. Specific December 2026 forecasts range from:

- BMO: 2.85%

- CIBC: 3.00%

- National Bank: 3.00%

- RBC: 3.10%

- TD: 3.15%

- Scotiabank: 3.25%

These bond yield increases suggest fixed mortgage rates could gradually increase to the 4.0%-4.5% range by late 2026, making current fixed rates at 3.69%-4.03% relatively attractive for risk-averse borrowers.

Inflation and Geopolitical Wildcards

Two factors could accelerate rate increases beyond consensus forecasts:

Inflation Pressures: Core inflation remained elevated at 2.6% in February 2026, with headline inflation at 1.8%[3]. Surging fuel costs in March 2026 could push inflation toward 3%, creating upward rate pressure.

Geopolitical Risk: The Iran conflict has lifted oil prices above $100/barrel and bond yields to 3.1%[1], increasing inflation risk and potential rate hike pressure.

However, weak labour data from February 2026 pushes back against rate-hike expectations[1], creating conflicting signals that make timing decisions more complex.

For self-employed borrowers reviewing 2026 mortgage rate forecasts, these competing factors require careful analysis and potentially professional guidance.

Strategic Considerations for Variable-to-Fixed Rate Switching

The Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes requires evaluating multiple factors beyond simple rate comparisons. Self-employed professionals must consider their unique financial circumstances, business stability, and risk tolerance.

Calculating Your Break-Even Point

The decision to switch from variable to fixed hinges on the break-even analysis:

Current Scenario (March 2026):

- Variable rate: 3.3%

- Fixed rate: 3.69%

- Rate differential: 0.39 percentage points

On a $500,000 mortgage with 25 years remaining:

- Additional monthly cost of switching to fixed: Approximately $110

- Annual additional cost: $1,320

If variable rates increase by 0.40 percentage points or more (to 3.7% or higher), the fixed rate becomes the better choice. Given Scotiabank’s forecast of rates reaching 3.0% by year-end (which would push variable rates to approximately 3.85%-4.0%), switching to fixed now could save $80-$170 monthly by Q4 2026.

Self-Employed Income Stability Assessment

Self-employed borrowers must honestly assess their business income stability:

✅ Consider switching to fixed if:

- Your business revenue fluctuates seasonally

- You have irregular client contracts or project-based income

- You’re in a cyclical industry sensitive to economic downturns

- You prefer predictable budgeting for business planning

⚠️ Consider staying variable if:

- You have long-term contracts or retainer clients

- Your business shows consistent year-over-year growth

- You maintain substantial cash reserves (6+ months expenses)

- You can absorb payment increases of 15-20% without hardship

For professionals working as IT consultants or contractors, income predictability varies significantly by specialization and client base.

Penalty Considerations When Breaking Variable Mortgages

Unlike fixed-rate mortgages with potentially expensive Interest Rate Differential (IRD) penalties, variable-rate mortgages typically charge only three months’ interest as a penalty for breaking the term early.

Example penalty calculation:

- Mortgage balance: $500,000

- Current variable rate: 3.3%

- Three months’ interest penalty: $4,125

This relatively modest penalty makes switching from variable to fixed more financially feasible compared to breaking a fixed mortgage. However, some lenders may also charge administrative fees ($200-$500) and potentially require a new appraisal ($300-$500).

Qualification Challenges for Self-Employed Switchers

When switching from variable to fixed, self-employed borrowers must re-qualify under current lending standards, which include:

- Stress Test Requirement: Qualify at the greater of your contract rate plus 2% OR 5.25%[9]

- Income Documentation: Updated NOAs, financial statements, and tax returns

- Debt Service Ratios: Total Debt Service (TDS) typically must remain below 44%

For self-employed borrowers who used alternative documentation methods for their original mortgage, switching to a traditional lender for fixed rates may prove challenging.

The Hybrid Approach: Splitting Your Mortgage

Rather than an all-or-nothing decision, consider splitting your mortgage between variable and fixed portions:

Example Strategy:

- 60% of mortgage ($300,000) locked at 3.69% fixed

- 40% of mortgage ($200,000) remains at 3.3% variable

Benefits:

- Partial protection against rate increases

- Maintained exposure to potential rate decreases

- Reduced switching penalties if circumstances change

- Balanced risk management approach

This strategy works particularly well for self-employed borrowers with moderate risk tolerance who want to hedge their bets on rate direction.

Implementing Your Rate Switching Strategy: Action Steps for Self-Employed Toronto Borrowers

Successfully executing the Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes requires methodical planning and preparation. Follow these actionable steps to position yourself for optimal timing.

Step 1: Gather Your Documentation (60-90 Days Before Switch)

Start assembling your financial documentation well in advance:

Required Documents:

- ✅ Last 2 years of personal tax returns (T1 Generals)

- ✅ Last 2 years of Notice of Assessments (NOAs)

- ✅ Last 2 years of business financial statements

- ✅ Last 2 years of corporate tax returns (T2s if incorporated)

- ✅ Year-to-date profit and loss statement

- ✅ Business bank statements (3-6 months)

- ✅ Proof of business registration and licensing

- ✅ Current mortgage statement showing balance and payment history

For borrowers who may not qualify through traditional channels, explore alternative documentation options that some lenders accept.

Step 2: Review Your Current Mortgage Terms

Before initiating a switch, thoroughly understand your existing mortgage:

Key Questions:

- What is your current mortgage balance?

- When does your term mature?

- What penalties apply for breaking your current term?

- Does your lender offer internal switches without penalties?

- Are there any prepayment privileges you haven’t used?

Many lenders allow internal switches from variable to fixed without penalties, though you’ll be limited to that lender’s current fixed rates. Shopping the market through a mortgage broker may yield better rates but could incur switching costs.

Step 3: Calculate Your True Cost of Switching

Create a comprehensive cost-benefit analysis:

Switching Costs:

- Penalty for breaking variable term (typically 3 months’ interest)

- Legal fees (if changing lenders): $500-$1,500

- Appraisal fees (if required): $300-$500

- Administration fees: $200-$500

- Total estimated costs: $1,000-$6,500

Potential Savings:

- Monthly payment difference if rates increase as forecasted

- Peace of mind value (difficult to quantify but important)

- Budget certainty for business planning

If forecasted rate increases materialize, most borrowers recoup switching costs within 12-18 months.

Step 4: Consult with a Mortgage Professional

Self-employed borrowers benefit significantly from professional guidance. A qualified mortgage broker can:

- Access multiple lenders simultaneously

- Identify lenders with favorable self-employed policies

- Navigate complex income documentation requirements

- Time your application to coincide with optimal rate offerings

- Structure your mortgage for maximum flexibility

Brokers have access to wholesale rates and specialized lenders that may not be available to retail borrowers, potentially offsetting their fees through better rate negotiation.

Step 5: Time Your Lock-In Strategically

Based on 2026 forecasts, consider these timing windows:

🟢 Optimal Switching Windows:

April-June 2026: If you believe Scotiabank’s aggressive forecast, lock in before Q3 rate increases. Current fixed rates at 3.69%-4.03% may represent the best available pricing before summer.

September-October 2026: If consensus forecasts prove correct and rates remain stable, waiting until fall may provide opportunities to lock in at similar or potentially lower fixed rates if bond yields soften.

⚠️ Avoid These Timing Mistakes:

- Waiting until renewal: By the time your term matures, rates may have increased significantly

- Switching during business low season: If your income documentation shows seasonal weakness, wait for stronger income periods

- Rushing without documentation: Incomplete applications lead to delays and missed rate holds

Step 6: Negotiate Rate Holds and Conditions

When ready to proceed:

- Request a 90-120 day rate hold: This protects you if rates increase while your application processes

- Negotiate removal of conditions: Work to eliminate appraisal requirements or reduce documentation requests

- Confirm prepayment privileges: Ensure your new fixed mortgage includes 15-20% annual prepayment options

- Verify portability: If you might move before term end, confirm the mortgage is portable

Step 7: Monitor Rate Movements and Adjust

Even after initiating a switch, stay informed:

- Track Bank of Canada announcements (scheduled decision dates: April 16, June 4, July 16, September 3, October 22, December 10, 2026)

- Monitor inflation reports and economic indicators

- Review bond yield movements weekly

- Maintain communication with your mortgage professional

If circumstances change dramatically (such as unexpected rate cuts), you may have options to adjust your strategy before final commitment.

Special Considerations for Toronto Real Estate Investors

Self-employed borrowers who also invest in rental properties face additional complexity:

- Rental income qualification: Lenders typically use 50-80% of gross rental income

- Multiple property management: Consider staggering mortgage terms to avoid simultaneous renewals

- Portfolio risk assessment: Balance variable and fixed rates across your property portfolio

- Cash flow protection: Fixed rates on rental properties provide more predictable cash flow projections

Comparing Fixed vs. Variable: The Long-Term Perspective

While the Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes focuses on current conditions, understanding the historical context helps inform better decisions.

Historical Rate Performance

Over the past 20 years, variable rates have typically saved borrowers money compared to fixed rates, with some notable exceptions:

- 2007-2008: Variable rate holders benefited as rates dropped during financial crisis

- 2017-2018: Fixed rate holders saved money as rates increased rapidly

- 2020-2022: Variable rate holders initially benefited, then faced sharp increases

- 2023-2025: Variable rates remained elevated but have begun declining

The general principle remains: variable rates win over time, but fixed rates win during periods of rapid rate increases.

The Self-Employed Risk Premium

Self-employed borrowers should consider an additional risk premium in their calculations:

Risk Factors:

- Income volatility increases vulnerability to payment shocks

- Qualification challenges make refinancing more difficult

- Business downturns could coincide with rate increases

- Limited access to emergency credit compared to salaried employees

These factors suggest self-employed borrowers may benefit from slightly more conservative rate strategies than traditional employees, making fixed rates more attractive even when mathematical models favor variable.

Understanding the Fixed vs. Variable Decision Framework

Beyond current rate forecasts, consider these psychological and practical factors:

Choose Fixed If:

- Sleep-at-night factor is important to you

- Your business faces near-term uncertainty

- You’re approaching retirement or major life changes

- You have limited financial cushion for payment increases

- You value budgeting certainty for business planning

Choose Variable If:

- You have substantial cash reserves

- Your business shows strong, consistent growth

- You can tolerate payment fluctuations of 20-30%

- You believe consensus forecasts of stable rates

- You want to maintain flexibility for prepayments

Conclusion

The Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes presents a complex but manageable decision in the current economic environment. With variable rates at historic lows of 3.3%-3.45% and fixed rates available at 3.69%-4.03%, self-employed borrowers face a narrow window of opportunity to lock in predictable payments before potential mid-2026 rate increases.

The split between bank forecasts—five predicting stable rates versus Scotiabank’s aggressive hike projection—creates uncertainty that requires careful analysis. For self-employed professionals, the additional challenges of income documentation, qualification requirements, and business income volatility make early planning essential.

Key Decision Points

✅ Switch to fixed now if:

- You believe rate hikes will materialize by Q3-Q4 2026

- Your business income shows volatility or seasonal fluctuation

- Payment predictability is critical for your financial planning

- You can absorb the 0.39-0.73 percentage point premium for certainty

⏰ Wait and monitor if:

- You believe the consensus forecast of stable rates

- Your business shows strong, consistent income growth

- You maintain substantial cash reserves

- You can quickly pivot to fixed rates if conditions change

Your Next Steps

- Schedule a consultation with a mortgage professional specializing in self-employed borrowers

- Gather your documentation now, even if you’re not ready to switch immediately

- Run the numbers on your specific mortgage balance and payment scenarios

- Set rate alerts to monitor bond yields and Bank of Canada announcements

- Review quarterly as new economic data and forecasts emerge

The mortgage market in 2026 offers both opportunities and risks. By understanding the Variable-to-Fixed Rate Switching Strategy for Self-Employed Toronto Borrowers: Timing Your Lock-In Before Forecasted 2026 Rate Hikes, you can make informed decisions that protect your financial future while optimizing your borrowing costs.

Remember: the best mortgage strategy is one that aligns with your unique business circumstances, risk tolerance, and financial goals. Take action now to position yourself for success regardless of which rate forecast proves accurate.

References

[1] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast

[2] Mortgage Rates Forecast Canada – https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/

[3] Canada Interest Rate Forecast – https://altrua.ca/canada-interest-rate-forecast/

[4] Watch – https://www.youtube.com/watch?v=edX4btOxgi0

[5] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast

[7] Mortgage Report – https://rates.ca/mortgage-report

[9] What Can Mortgage Borrowers Expect In 2026 – https://www.ratehub.ca/blog/what-can-mortgage-borrowers-expect-in-2026/