February 11, 2026

Why 2026 is the Perfect Time for First-Time Buyers to Enter Toronto’s Cooling Housing Market

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

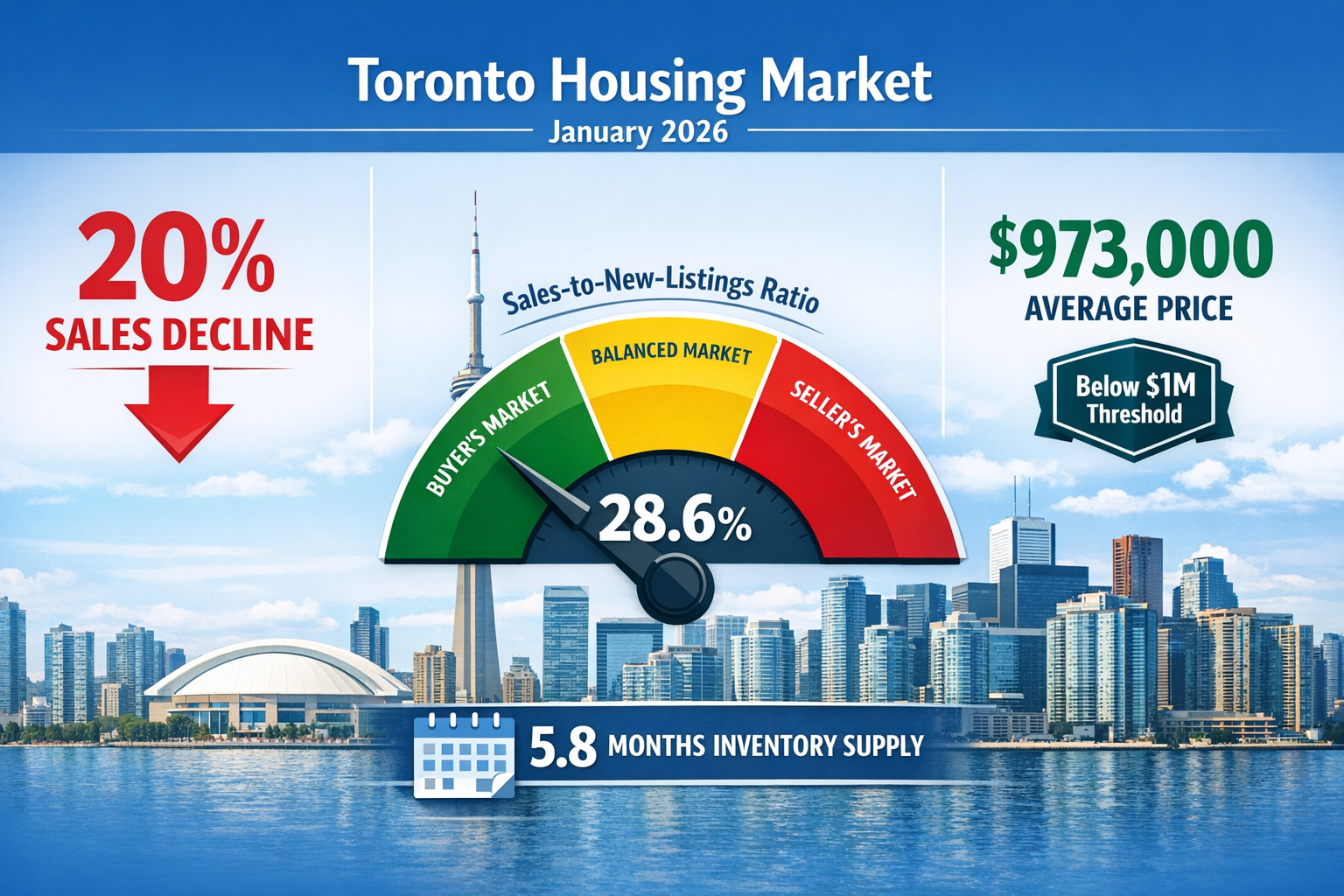

Toronto’s housing market has undergone a dramatic transformation, and why 2026 is the perfect time for first-time buyers to enter Toronto’s cooling housing market becomes crystal clear when examining the January 2026 data. For the first time in five years, average home prices have dipped below the psychologically significant $1 million threshold, sales have plummeted 20%, and the market has decisively shifted into buyer-friendly territory. This rare convergence of factors creates an unprecedented opportunity window for aspiring homeowners who have been priced out for years.

The numbers tell a compelling story: with a sales-to-new-listings ratio hovering around 28.6%–31%[3][4], well below the 40% threshold that defines a buyer’s market, first-time purchasers now hold negotiating power that hasn’t existed since before the pandemic. Combined with 5.8 months of inventory supply[4], declining prices across all property types, and reduced competition from investors, the conditions have aligned for those ready to take decisive action.

Key Takeaways

🏠 Buyer’s Market Advantage: Toronto’s sales-to-new-listings ratio of 28.6%–31% signals strong buyer leverage, with inventory levels at 5.8 months providing ample selection and negotiation power[3][4].

📉 Historic Price Decline: Average home prices have fallen to approximately $973,000, dropping below $1 million for the first time in five years, with the benchmark price at $936,100 representing an 8% year-over-year decline[4][5].

🏢 Condo Entry Opportunity: Median condo prices reached $749,500 in January 2026, down 6.3% year-over-year, offering the most accessible entry point for budget-conscious first-time buyers[4].

👥 First-Time Buyer Dominance: An impressive 45% of intending homebuyers in 2026 will be first-time purchasers, positioning this demographic as a potential market recovery driver[1][4].

⏰ Reduced Competition: Overall homebuying intentions have fallen to 22% for 2026, down five percentage points from 2025, meaning less competition for motivated buyers ready to act[1][6].

Understanding Toronto’s 2026 Market Transformation

The Shift from Seller to Buyer Control

The Toronto housing market has experienced a fundamental power shift that makes why 2026 is the perfect time for first-time buyers to enter Toronto’s cooling housing market more than just opportunistic timing—it’s a structural market change. The sales-to-new-listings ratio, a critical metric that determines market dynamics, now sits between 28.6% and 31%[3][4], firmly in buyer’s market territory.

Understanding the sales-to-new-listings ratio:

- Above 60%: Seller’s market (high competition, bidding wars, premium prices)

- 40–60%: Balanced market (fair negotiation for both parties)

- Below 40%: Buyer’s market (negotiating power, price flexibility, more choices)[5]

At the current ratio, buyers have significant leverage. For every 100 new listings that come to market, only 28 to 31 are selling, creating a surplus of available properties. This surplus forces sellers to become more flexible on pricing, closing timelines, and conditions—advantages that first-time buyers can capitalize on.

Inventory Levels Favor Patient Buyers

The 5.8 months of inventory supply[4] represents a critical advantage for first-time purchasers. In a balanced market, 4–6 months of inventory is typical, meaning Toronto is at the upper end of this range with a slight tilt toward oversupply. This metric indicates how long it would take to sell all current listings if no new properties came to market.

What this means practically:

✅ More time for due diligence: Buyers can thoroughly inspect properties, review condo documents, and assess neighborhood fit without pressure

✅ Reduced bidding wars: The days of 20+ offers on a single property have largely disappeared

✅ Negotiation opportunities: Sellers are more willing to consider price reductions, cover closing costs, or include appliances and fixtures

✅ Extended decision-making: Average days on market are increasing across the GTA[5], allowing buyers to avoid rushed decisions

Active listings increased 8.1% year-over-year despite new listings declining 13%[5], a paradox that reveals properties are sitting longer on the market. This accumulation of inventory gives first-time buyers unprecedented selection.

Price Declines Create Affordability Windows

The most dramatic indicator of why 2026 is the perfect time for first-time buyers to enter Toronto’s cooling housing market is the price correction underway. The GTA benchmark price has fallen to $936,100, representing an 8% year-over-year decline[4]. More significantly, average prices have dropped from approximately $1,060,000 last year to near $973,000[5], crossing below the million-dollar psychological threshold.

Price decline breakdown by metric:

| Metric | Current Value | Year-Over-Year Change |

|---|---|---|

| MLS House Price Index | Declined 8% | -8.0%[5] |

| Average Home Price | ~$973,000 | -6.5%[5] |

| Benchmark Price | $936,100 | -8.0%[4] |

| Median Condo Price | $749,500 | -6.3%[4] |

This price correction translates to real savings. A buyer purchasing at $973,000 instead of $1,060,000 saves $87,000 on the purchase price. With a 10% down payment, that’s $8,700 less required upfront, plus reduced mortgage insurance premiums and lower monthly carrying costs.

For those exploring the rise of condo living in Toronto, the $749,500 median condo price represents an even more accessible entry point, particularly for single buyers or young couples starting their homeownership journey.

Why 2026 Market Conditions Favor First-Time Buyers Specifically

Property Type Performance Creates Strategic Opportunities

Not all property types are experiencing the same market pressures, and understanding these variations is crucial for first-time buyers making strategic decisions. The sales decline data reveals where the greatest opportunities—and negotiating leverage—exist.

Sales decline by property type (January 2026):

🏢 Condos: -26% sales decline[4]

- Why it matters: The hardest-hit segment offers maximum negotiation power

- Opportunity: Investor demand that drove pandemic-era appreciation has evaporated

- Best for: Single buyers, young professionals, those prioritizing location over space

🏘️ Townhomes: -24% sales decline[4]

- Why it matters: Middle-tier pricing with family-friendly layouts

- Opportunity: Bridge between condo and detached home affordability

- Best for: Growing families, those wanting outdoor space without detached home prices

🏠 Semi-Detached: -20% sales decline[4]

- Why it matters: Suburban family homes with yard space

- Opportunity: Less competitive than detached but more space than townhomes

- Best for: Families prioritizing space and schools

🏡 Detached Homes: -14% sales decline[4]

- Why it matters: Smallest decline indicates relatively stronger demand

- Opportunity: Still under price pressure but most competitive segment

- Best for: Larger families, those with higher budgets, long-term hold strategies

The 26% decline in condo sales[4] is particularly significant for first-time buyers. During the pandemic, investor speculation drove condo prices to unsustainable levels as landlords anticipated continued rental demand. That investor class has largely exited, creating opportunities for owner-occupiers to purchase without competing against cash-heavy investors.

First-Time Buyers Represent 45% of Market Demand

One of the most encouraging statistics for aspiring homeowners is that 45% of intending homebuyers in 2026 will be first-time buyers[1][4]. This disproportionate representation positions first-time purchasers as a potential recovery driver despite broader market weakness.

Why this demographic shift matters:

💪 Market power: Lenders and builders are tailoring products to first-time buyers 📊 Government support: Programs like the Home Buyers’ Plan remain accessible 🎯 Industry focus: Real estate professionals are prioritizing first-time buyer needs 💰 Competitive advantage: Less competition from move-up buyers and investors

The Canada 2024 Budget initiatives have continued to support first-time buyers through 2026, including extended amortization periods for insured mortgages on new builds and enhanced RRSP withdrawal limits for down payments.

Reduced Overall Competition Creates Opportunity

While 45% of buyers are first-timers, overall homebuying intentions have fallen dramatically. Ipsos polling shows homebuying intentions fell to just 22% for 2026, down five percentage points from 2025[1][6]. This reflects economic uncertainty and cautious consumer sentiment despite improved affordability.

What declining competition means:

✅ Fewer offers per property: Multiple offer scenarios are increasingly rare ✅ Longer negotiation windows: Sellers can’t create artificial urgency ✅ Condition flexibility: Buyers can include financing and inspection conditions ✅ Price discovery: True market value becomes clearer without bidding wars

This dynamic creates a paradox: the market is more accessible for those ready to act, but overall caution keeps many potential buyers sidelined. Decisive first-time buyers who have prepared financially can capitalize while others hesitate.

Strategic Actions for First-Time Buyers in 2026

Get Pre-Approved with Competitive Rate Options

The foundation of any successful home purchase is mortgage pre-approval. In 2026’s market, understanding your borrowing capacity and securing rate holds is more important than ever. Interest rate volatility means the difference between affordable monthly payments and budget strain.

Pre-approval advantages in a buyer’s market:

🔒 Rate holds: Lock in current rates for 90-120 days while you shop 💰 Budget clarity: Know exactly what you can afford before making offers ⚡ Faster closing: Pre-approval speeds up the purchase process 💪 Negotiation strength: Sellers take pre-approved buyers more seriously

For first-time buyers, choosing between fixed vs variable rates requires careful consideration of risk tolerance and market forecasts. In 2026, with rate uncertainty persisting, many first-time buyers are opting for fixed rates to ensure payment predictability.

Maximize Down Payment Strategies

The down payment remains the biggest barrier for most first-time buyers. Fortunately, several strategies can help bridge the gap:

RRSP Home Buyers’ Plan: Withdraw up to $35,000 tax-free from your RRSP ($70,000 for couples) to fund your down payment. This powerful tool allows you to use your own retirement savings without immediate tax consequences. Learn more about RRSPs and the Home Buyers’ Plan.

Minimum down payment requirements:

- Under $500,000: 5% minimum

- $500,000–$999,999: 5% on first $500,000, 10% on remainder

- $1,000,000+: 20% minimum (no mortgage insurance available)

Example calculation for $750,000 condo:

- First $500,000 @ 5% = $25,000

- Remaining $250,000 @ 10% = $25,000

- Total minimum down payment: $50,000

Down payment sources: ✅ Personal savings ✅ RRSP Home Buyers’ Plan withdrawal ✅ Gifted funds from family (with proper documentation) ✅ Sale of other assets ✅ Tax-Free Savings Account (TFSA) withdrawals

Target Properties with Maximum Leverage

In why 2026 is the perfect time for first-time buyers to enter Toronto’s cooling housing market, property selection strategy becomes paramount. Focus on segments where you have maximum negotiating leverage.

High-leverage opportunities:

1️⃣ Condos priced $700,000–$800,000: The hardest-hit segment with -26% sales decline[4] 2️⃣ Properties with 30+ days on market: Sellers become increasingly motivated 3️⃣ Units requiring cosmetic updates: Buyers can negotiate price reductions for renovation costs 4️⃣ Buildings with higher maintenance fees: Less competition allows for better pricing 5️⃣ Locations slightly outside prime neighborhoods: Value opportunities in emerging areas

Make Strategic Offers with Conditions

Unlike the pandemic-era market where unconditional offers were standard, 2026’s buyer’s market allows for protective conditions:

Essential conditions for first-time buyers:

🏠 Home inspection condition: Protects against hidden defects and structural issues 💰 Financing condition: Ensures mortgage approval at acceptable terms 📋 Condo document review: For condos, review status certificates, reserve fund studies, and bylaws 🔍 Title search condition: Confirms clean title and identifies any liens or encumbrances

Negotiation tactics in 2026:

- Start 5–10% below asking price on properties with extended market time

- Request seller-paid closing costs or appliance inclusions

- Negotiate flexible closing dates that align with your lease end or sale timeline

- Ask for repairs or credits based on inspection findings

Understand Total Ownership Costs

First-time buyers often focus exclusively on mortgage payments while underestimating total ownership costs. A comprehensive budget includes:

Monthly carrying costs:

| Cost Category | Typical Range | Notes |

|---|---|---|

| Mortgage Payment | $3,000–$4,500 | Based on $750K purchase, 10% down |

| Property Tax | $250–$400 | Varies by municipality and assessment |

| Condo Fees (if applicable) | $400–$700 | Includes maintenance, amenities, reserve fund |

| Home Insurance | $100–$200 | Required by lenders |

| Utilities | $150–$300 | Heat, hydro, water, internet |

| Maintenance Reserve | $100–$200 | For repairs and replacements |

| Total Monthly | $4,000–$6,300 | Comprehensive ownership cost |

One-time closing costs:

- Legal fees: $1,500–$2,500

- Land transfer tax: 0.5%–2% of purchase price

- Toronto municipal land transfer tax (additional): 0.5%–2%

- Home inspection: $400–$600

- Title insurance: $200–$400

- Moving costs: $500–$2,000

- Total closing costs: Typically 3–4% of purchase price

Act Decisively While the Window Remains Open

Market windows don’t remain open indefinitely. While why 2026 is the perfect time for first-time buyers to enter Toronto’s cooling housing market is supported by current data, several factors could shift conditions:

Potential market changes ahead:

⚠️ Interest rate cuts: Further Bank of Canada rate reductions could reignite demand ⚠️ Immigration policy: Changes to immigration targets affect housing demand ⚠️ Economic recovery: Improved consumer confidence could bring buyers back ⚠️ Investor return: If rental yields improve, investor competition may resume

Timeline for action:

📅 Months 1–2: Get pre-approved, review finances, research neighborhoods 📅 Months 2–4: Active property search, attend open houses, make offers 📅 Months 4–6: Firm up purchase, complete inspections, finalize financing 📅 Month 6+: Close and take possession

The TRREB 2026 Market Outlook emphasizes improved buyer choice and affordability[1], but also notes weak consumer confidence. Those who overcome hesitation and act strategically while others remain cautious will capture the greatest value.

Navigating Financing in 2026’s Market Environment

Understanding Current Rate Environment

Interest rates remain a critical factor in affordability calculations. While rates have declined from their 2023 peaks, they remain elevated compared to the ultra-low pandemic era. First-time buyers need to understand the current landscape and forecast trends.

2026 rate considerations:

📊 Fixed rates: Currently ranging from 4.5%–5.5% for 5-year terms 📊 Variable rates: Typically 0.25%–0.75% lower than fixed rates initially 📊 Rate forecast: Economists predict gradual declines through 2026–2027 📊 Qualification rates: Stress test requires qualification at higher rate (typically 5.25% or contract rate + 2%)

The decision between fixed and variable rates depends on individual circumstances. Risk-averse first-time buyers often prefer fixed rates for payment certainty, while those comfortable with potential fluctuation may benefit from variable rates if the Bank of Canada continues cutting rates.

Mortgage Insurance Requirements and Costs

For down payments under 20%, mortgage default insurance (often called CMHC insurance, though multiple providers exist) is mandatory. While this adds to upfront costs, it also enables homeownership with smaller down payments.

Mortgage insurance premium rates:

| Down Payment | Premium Rate | Example on $750K Purchase |

|---|---|---|

| 5.00%–9.99% | 4.00% | $28,000 premium |

| 10.00%–14.99% | 3.10% | $21,700 premium |

| 15.00%–19.99% | 2.80% | $19,600 premium |

These premiums are typically added to the mortgage amount rather than paid upfront, spreading the cost over the amortization period. While this increases total interest paid, it allows buyers to enter the market sooner rather than waiting years to save a 20% down payment.

Self-Employed and Non-Traditional Income Buyers

Self-employed individuals and those with non-traditional income face additional documentation requirements but can absolutely succeed as first-time buyers in 2026. The key is working with experienced mortgage professionals who understand alternative documentation pathways.

For self-employed buyers, options include traditional income verification through tax returns (typically requiring 2 years of business history) or alternative stated income programs through B-lenders at slightly higher rates. The cooling market actually benefits self-employed buyers, as lower prices mean lower mortgage amounts and easier qualification.

Government Programs and Incentives

First-time buyers in 2026 can access several government programs designed to improve affordability:

Federal programs:

- Home Buyers’ Plan: RRSP withdrawal up to $35,000 tax-free

- First-Time Home Buyer Incentive: Shared equity mortgage (income and price restrictions apply)

- GST/HST New Housing Rebate: For new construction purchases

Provincial programs (Ontario):

- Land Transfer Tax Refund: Up to $4,000 refund for first-time buyers

- Ontario Home Ownership Savings Plan: Tax-deferred savings (if implemented)

These programs can save thousands of dollars and should be factored into any first-time buyer’s strategy.

Common Mistakes to Avoid in 2026’s Buyer’s Market

Overextending Financial Capacity

The most common mistake first-time buyers make is purchasing at the absolute maximum of their pre-approval amount. While lenders will approve you up to certain debt service ratios, that doesn’t mean you should spend that much.

Financial buffer recommendations:

✅ Keep mortgage payments under 30% of gross income (lenders allow up to 39%) ✅ Maintain 3–6 months emergency fund after down payment and closing costs ✅ Budget for lifestyle maintenance beyond basic shelter costs ✅ Plan for rate increases at renewal (if choosing variable or short-term fixed)

A buyer’s market creates temptation to stretch for a “dream home,” but financial stress can turn that dream into a nightmare. Purchase conservatively and upgrade later when equity has built.

Skipping Professional Inspections

In a buyer’s market, some purchasers assume they can skip inspections to save a few hundred dollars. This is false economy. A $500 inspection can identify $50,000 in hidden problems.

What inspections reveal:

- Structural issues (foundation, framing, roof)

- Mechanical systems condition (HVAC, plumbing, electrical)

- Water damage or moisture intrusion

- Code violations or unpermitted work

- Deferred maintenance requiring immediate attention

For condos, reviewing the status certificate and reserve fund study is equally critical. Buildings with underfunded reserves may face special assessments that dramatically increase ownership costs.

Ignoring Neighborhood Research

First-time buyers often focus exclusively on the property itself while neglecting neighborhood research. The location will impact resale value, lifestyle satisfaction, and long-term appreciation potential.

Neighborhood due diligence:

🏫 School quality: Even without children, good schools drive property values 🚇 Transit access: Proximity to subway, GO stations, or major bus routes 🛒 Amenities: Grocery stores, restaurants, parks, recreation facilities 📈 Development plans: Upcoming infrastructure or zoning changes 🚨 Safety statistics: Crime rates and community safety perception 💼 Employment proximity: Commute time to major employment centers

Toronto’s diverse neighborhoods offer vastly different value propositions. Areas like North York, Scarborough, and Etobicoke often provide better entry-level pricing than downtown core locations while still offering excellent amenities and transit access.

Failing to Negotiate in a Buyer’s Market

Many first-time buyers, intimidated by the process, accept asking prices or make minimal negotiation efforts. In 2026’s market conditions, this leaves significant money on the table.

Negotiation opportunities:

💰 Purchase price: Start 5–10% below asking on properties with extended market time 🏠 Included items: Appliances, window coverings, light fixtures, outdoor furniture 💵 Closing cost credits: Seller pays portion of land transfer tax or legal fees 🔧 Repair credits: Cash back at closing for items identified in inspection 📅 Flexible closing: Timing that benefits your situation (lease end, rate hold expiry)

Remember: in a buyer’s market with 5.8 months of inventory[4], sellers are motivated. The worst they can say is no, and counteroffers often meet buyers somewhere in the middle.

The Long-Term Perspective: Building Wealth Through Homeownership

Equity Building in a Stabilizing Market

While 2026 presents a cooling market, the long-term trajectory of Toronto real estate remains positive. The current correction creates an entry point, but the fundamentals supporting Toronto housing demand remain intact:

Long-term demand drivers:

📈 Population growth: Immigration and interprovincial migration continue 🏙️ Economic hub: Toronto remains Canada’s financial and business center 🎓 Education destination: Major universities attract domestic and international students 🌍 Global city status: International investment and talent attraction 🚧 Supply constraints: Geographic limitations and regulatory barriers limit new supply

Even if prices remain flat for 1–2 years, mortgage principal reduction builds equity with every payment. A $700,000 mortgage at 5% amortized over 25 years will build approximately $60,000 in equity over the first five years through principal paydown alone—plus any market appreciation.

Forced Savings and Wealth Accumulation

Homeownership functions as a forced savings mechanism. Unlike rent payments that build zero equity, mortgage payments gradually increase your net worth. Over time, this becomes the primary wealth-building tool for middle-class Canadians.

10-year wealth building example:

Scenario: Purchase $750,000 condo with 10% down ($75,000)

| Year | Mortgage Balance | Home Value (2% annual appreciation) | Equity Position |

|---|---|---|---|

| 0 | $675,000 | $750,000 | $75,000 |

| 5 | $565,000 | $828,000 | $263,000 |

| 10 | $445,000 | $914,000 | $469,000 |

Even with conservative 2% annual appreciation, equity grows from $75,000 to $469,000 over 10 years—a 525% return on the initial down payment investment.

Tax Advantages of Principal Residence

Canadian tax law provides significant advantages for principal residence ownership:

✅ Capital gains exemption: No tax on appreciation when you sell your principal residence ✅ No annual property tax on equity: Unlike investments, home equity isn’t taxed annually ✅ RRSP Home Buyers’ Plan: Tax-free withdrawal for down payment ✅ First-time buyer credits: Land transfer tax rebates and other provincial benefits

These tax advantages amplify the wealth-building potential of homeownership compared to other investment vehicles.

Why Waiting Could Cost More Than Buying Now

The Price of Hesitation

Many potential first-time buyers adopt a “wait and see” approach, hoping prices will fall further. While caution is prudent, excessive hesitation carries real costs:

Opportunity costs of waiting:

📈 Rent payments: $2,000–$3,000 monthly rent builds zero equity ⏰ Time out of market: Every year of waiting is a year of missed equity building 📊 Rate risk: If rates fall, demand may surge and prices could stabilize or rise 🏠 Inventory depletion: Best properties in your price range may sell to other buyers 💰 Inflation impact: Your down payment savings may not keep pace with price changes

Example calculation:

If you wait one year while paying $2,500 monthly rent, that’s $30,000 in rent payments with zero equity building. If you had purchased instead, that same $30,000 in mortgage payments would have built approximately $10,000–$12,000 in equity through principal reduction, plus any market appreciation.

Market Timing is Nearly Impossible

Professional investors and economists struggle to time markets perfectly. For first-time buyers, attempting to “call the bottom” often results in missing opportunities entirely.

Market timing challenges:

❌ Data is backward-looking: By the time you see recovery in statistics, prices have already risen ❌ Emotional decision-making: Fear during downturns, greed during upturns ❌ Life timing: Your personal circumstances (marriage, children, job changes) don’t wait for perfect markets ❌ Competitive dynamics: When conditions improve, everyone else recognizes it simultaneously

The better approach: buy when you’re financially ready and market conditions are favorable. By both measures, 2026 qualifies for first-time buyers who have prepared adequately.

The “Good Enough” Market Philosophy

Rather than waiting for the “perfect” market (which may never arrive), successful first-time buyers recognize when conditions are “good enough” to act:

✅ Prices below recent peaks: ✓ (Down 6.5%–8% year-over-year)[4][5] ✅ Buyer negotiating leverage: ✓ (28.6%–31% sales-to-new-listings ratio)[3][4] ✅ Adequate inventory selection: ✓ (5.8 months supply)[4] ✅ Manageable interest rates: ✓ (Declined from 2023 peaks, forecast to fall further) ✅ Personal financial readiness: ✓ (If you’ve saved down payment and have stable income)

When these factors align—as they do in 2026—conditions are “good enough” to proceed confidently.

Conclusion: Seizing Toronto’s 2026 Opportunity Window

Why 2026 is the perfect time for first-time buyers to enter Toronto’s cooling housing market isn’t just marketing rhetoric—it’s supported by compelling data showing a rare convergence of favorable conditions. With sales down 20%, prices below $1 million for the first time in five years, a decisive buyer’s market with 5.8 months of inventory, and first-time buyers representing 45% of market demand, the opportunity window is wide open.

The cooling market has created conditions that favor prepared, decisive first-time buyers:

🎯 Negotiating power through low sales-to-new-listings ratios 🎯 Price accessibility with average prices near $973,000 and condos at $749,500 🎯 Reduced competition as overall buying intentions decline 🎯 Time for due diligence with extended days on market 🎯 Property selection across multiple segments experiencing price pressure

However, market windows don’t remain open indefinitely. Interest rate cuts, improved economic sentiment, or policy changes could reignite demand and close this opportunity. The time to act is while others hesitate.

Your Next Steps

Immediate actions for aspiring first-time buyers:

1️⃣ Get pre-approved for a mortgage to understand your buying power and lock in rate holds

2️⃣ Maximize your down payment using RRSP Home Buyers’ Plan and other strategies outlined in this article

3️⃣ Research target neighborhoods focusing on areas with strong fundamentals and future growth potential

4️⃣ Engage experienced professionals including mortgage brokers, real estate agents, and home inspectors

5️⃣ Start actively viewing properties in segments with maximum negotiating leverage (especially condos and townhomes)

6️⃣ Make strategic offers with appropriate conditions to protect your interests

7️⃣ Act decisively when you find a property that meets your needs and budget

The first-time buyers who will look back on 2026 with satisfaction are those who recognized the opportunity, prepared adequately, and acted while others remained paralyzed by uncertainty. Toronto’s cooling housing market has created a rare entry point—the question is whether you’ll seize it.

For personalized guidance on navigating why 2026 is the perfect time for first-time buyers to enter Toronto’s cooling housing market, connect with experienced mortgage professionals who understand the current landscape and can help you structure financing that positions you for long-term success. Your homeownership journey begins with a single decisive step—make 2026 the year you take it.

References

[1] Gta Home Sales And Prices Expected To Remain Stable In 2026 Amid Ongoing Affordability Pressures – https://trreb.ca/gta-home-sales-and-prices-expected-to-remain-stable-in-2026-amid-ongoing-affordability-pressures/

[2] Housing Market Outlook 2026 – https://globalnews.ca/news/11661284/housing-market-outlook-2026/

[3] Gta Analysts Forecast Stable Homes Prices In 2026 – https://www.reminetwork.com/articles/gta-analysts-forecast-stable-homes-prices-in-2026/

[4] Buying Your First Home In Torontos 2026 Buyers Market A Step By Step Guide – https://everythingmortgages.ca/blog/buying-your-first-home-in-torontos-2026-buyers-market-a-step-by-step-guide/

[5] Watch – https://www.youtube.com/watch?v=CwtgWW_ClYM

[6] Gta Sales Prices Trreb 2026 – https://storeys.com/gta-sales-prices-trreb-2026/