February 4, 2026

Fixed vs Variable Rates for Toronto First-Time Buyers Refinancing in 2026: Which Saves More?

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

The mortgage landscape in Toronto has shifted dramatically, and first-time buyers facing refinancing decisions in 2026 are standing at a critical crossroads. With variable rates now dipping below 4% and surging in popularity—up 25.7% year-over-year—while the Bank of Canada holds steady at 2.25%, the question of Fixed vs Variable Rates for Toronto First-Time Buyers Refinancing in 2026: Which Saves More? has never been more relevant. The answer could mean thousands of dollars in savings or unexpected payment shocks.

As approximately 1.15 million Canadian mortgage holders prepare to renew their mortgages in 2026, understanding the true cost difference between fixed and variable options has become essential.[1] The stakes are particularly high for first-time buyers who purchased during the pandemic’s ultra-low rate environment and now face their first renewal in a vastly different economic climate.

Key Takeaways

- 💰 Variable rates currently sit at approximately 3.55%, offering immediate savings compared to fixed rates at 3.94%, with forecasts showing stability through 2026[1][2]

- 📊 Variable-rate borrowers face only 4% average payment increases at renewal, while fixed-rate holders experience shocking 26% jumps—a difference of over $5,600 annually[1]

- 🏦 The Bank of Canada’s policy rate remains at 2.25% with expectations for continued stability through most of 2026, reducing variable rate volatility[3][4]

- 🎯 Market conditions create a rare opportunity for first-time buyers refinancing in 2026, with borrowing costs significantly lower than during the recent rate-hiking cycle[3]

- ⚖️ Your choice depends on risk tolerance and budget flexibility, but current data suggests variable rates offer substantial short-term savings for those who can handle minor fluctuations

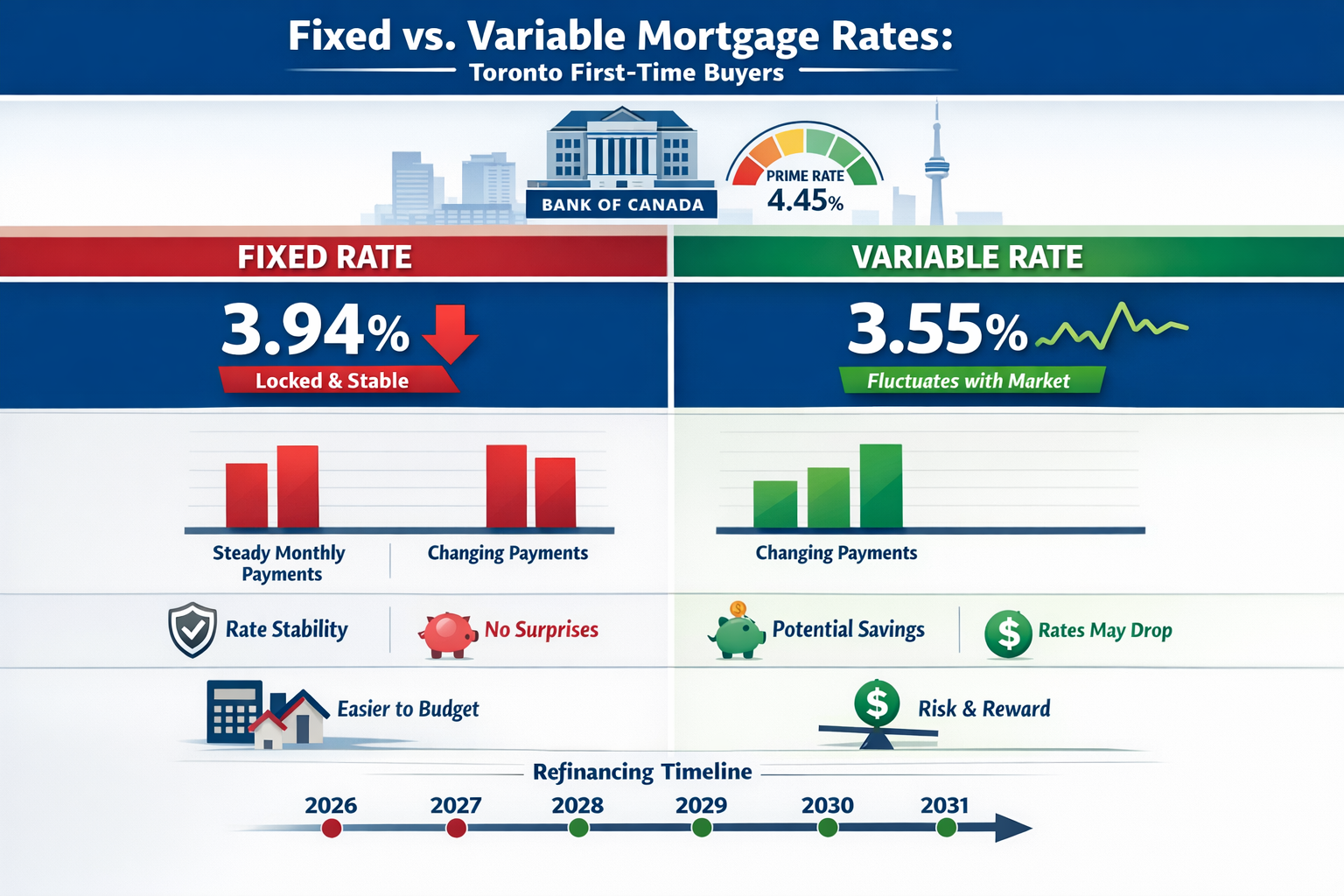

Understanding the Current Rate Environment in Toronto

Where Rates Stand in 2026

The mortgage rate landscape in Toronto has stabilized considerably compared to the volatility experienced during 2022-2024. As of early 2026, prime rate stands at 4.45% across major Canadian banks, with the Bank of Canada maintaining its policy rate at 2.25% for the second consecutive decision.[2][5]

For first-time buyers exploring refinancing options, the current competitive rates are:

| Rate Type | Current Rate | Monthly Payment (on $500,000) |

|---|---|---|

| Variable Rate | 3.55% | ~$2,228 |

| Fixed Rate (5-year) | 3.94% | ~$2,350 |

| Monthly Savings (Variable) | — | $122 |

| Annual Savings (Variable) | — | $1,464 |

These numbers represent a significant shift from the pandemic era when rates bottomed out below 2%. Understanding how mortgages work in Toronto helps contextualize why these current rates actually represent favorable conditions for refinancing.

Bank of Canada Policy Outlook

The Bank of Canada’s measured approach to monetary policy in 2026 has created an environment of relative predictability. Major financial institutions forecast no significant rate movements through most of 2026, with some projecting potential increases only toward Q4 or into 2027.[4][6]

This stability is crucial for first-time buyers weighing their options. Unlike the aggressive rate-hiking cycle of 2022-2023, the current environment allows for more confident decision-making. Variable rates are projected to range from 3.55% in January 2026 to approximately 3.65% by December 2026—a minimal spread that suggests limited downside risk.[6]

Fixed vs Variable Rates for Toronto First-Time Buyers Refinancing in 2026: The Payment Shock Reality

The True Cost of Fixed-Rate Renewals

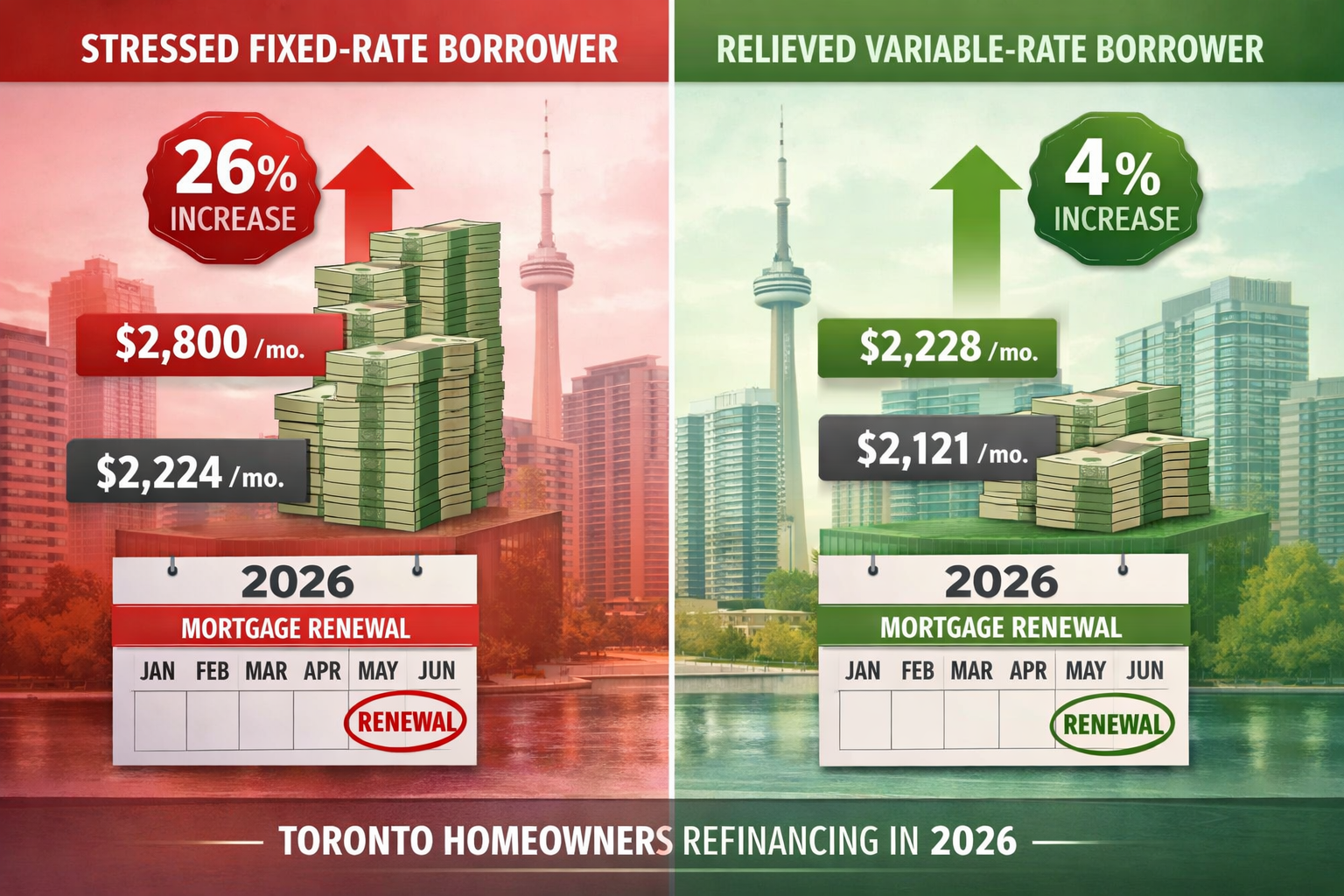

For first-time buyers who locked in ultra-low fixed rates during 2020-2021, the renewal reality in 2026 brings significant payment increases. Fixed-rate borrowers face an average payment increase of 26% when renewing at current rates.[1]

Consider this real-world scenario:

Original Mortgage (December 2020):

- Rate: 1.39% (5-year fixed)

- Monthly Payment: $2,224

- Borrower Profile: Toronto first-time buyer, $500,000 mortgage

Renewal (2026):

- New Rate: 3.94% (current 5-year fixed)

- New Monthly Payment: $2,800

- Monthly Increase: $576

- Annual Increase: $6,912

This represents a substantial budget adjustment that many first-time buyers may struggle to accommodate, especially in Toronto’s high cost-of-living environment. Approximately 33% of mortgage holders renewing in 2026 will face higher monthly payments, with 75% of those affected holding 5-year fixed-rate mortgages.[4]

The Variable Rate Advantage

In stark contrast, variable-rate borrowers experience dramatically smaller increases at renewal. The average payment increase for variable-rate holders is only 4%—a fraction of what fixed-rate borrowers face.[1]

Variable Rate Scenario:

Original Mortgage (December 2020):

- Rate: 0.99% (variable)

- Monthly Payment: $2,121

- Borrower adjusted payments during rate increases

Renewal (2026):

- New Rate: 3.55% (current variable)

- New Monthly Payment: $2,228

- Monthly Increase: $107

- Annual Increase: $1,284

The difference is striking: variable-rate borrowers save approximately $5,628 annually compared to their fixed-rate counterparts when renewing in 2026. This advantage exists because variable-rate holders already absorbed rate increases gradually during the Bank of Canada’s hiking cycle, while fixed-rate borrowers face the full adjustment at once.

For those interested in exploring various refinancing strategies, our guide on how to refinance your mortgage to save money provides additional insights.

Breaking Down the Numbers: Which Rate Type Saves More?

Five-Year Cost Projection Analysis

When evaluating Fixed vs Variable Rates for Toronto First-Time Buyers Refinancing in 2026: Which Saves More?, looking at the total cost over a typical mortgage term provides clarity.

Assumptions:

- Mortgage Amount: $500,000

- Amortization: 25 years remaining

- Time Horizon: 5 years (2026-2031)

- Variable Rate Forecast: 3.55% – 3.65% range[6]

- Fixed Rate: 3.94%[2]

Total Interest Paid Over 5 Years:

| Rate Type | Average Rate | Total Interest Paid | Total Payments |

|---|---|---|---|

| Variable | 3.60% | ~$86,400 | ~$133,680 |

| Fixed | 3.94% | ~$94,200 | ~$141,000 |

| Savings with Variable | — | $7,800 | $7,320 |

These projections assume relatively stable rates based on current Bank of Canada forecasts. Even if variable rates increase to the upper end of predictions (3.65%), the savings remain substantial compared to locking in at 3.94% fixed.

Risk-Adjusted Considerations

While the numbers favor variable rates, first-time buyers must consider their risk tolerance and budget flexibility. Here’s how different scenarios might play out:

Best-Case Scenario (Variable):

- Bank of Canada cuts rates in late 2026/early 2027

- Variable rate drops to 3.40%

- Additional savings of $1,200+ annually

Worst-Case Scenario (Variable):

- Unexpected economic shock triggers rate increases

- Variable rate rises to 4.25%

- Monthly payments increase by approximately $150

Fixed Rate Certainty:

- Payments remain exactly $2,350/month

- No surprises, easier budgeting

- Peace of mind for risk-averse borrowers

For Toronto first-time buyers with tight budgets or irregular income, the predictability of fixed rates may outweigh the statistical savings of variable rates. Our comprehensive mortgage rate guide covering fixed or variable mortgage options explores these trade-offs in greater detail.

Special Considerations for Toronto First-Time Buyers

The Toronto Real Estate Context

Toronto’s unique housing market creates specific considerations for first-time buyers refinancing in 2026. With the rise of condo living in Toronto continuing to shape the market, many first-time buyers hold mortgages on condominiums where condo fees already strain monthly budgets.

Toronto-Specific Factors:

🏙️ High Property Values: Toronto’s average home price means larger mortgage amounts, amplifying the impact of rate differences

💼 Employment Volatility: Toronto’s diverse economy includes sectors with varying stability—tech workers may prefer variable flexibility, while public sector employees might value fixed certainty

📈 Property Appreciation: Strong Toronto real estate appreciation may allow refinancing to access equity for renovations or debt consolidation

🚇 Location Premium: Properties near transit command premiums but also hold value better, potentially justifying variable rate risk

Income Stability and Budget Capacity

First-time buyers should honestly assess their financial situation before choosing between fixed and variable rates:

Choose Variable If:

- ✅ You have stable employment with regular income

- ✅ Your budget includes a 10-15% buffer for payment increases

- ✅ You can make lump-sum payments when rates are low

- ✅ You’re comfortable with minor monthly payment fluctuations

- ✅ You plan to sell or refinance within 3-5 years

Choose Fixed If:

- ✅ You’re self-employed with variable income (see our guide for opportunities for first-time homebuyers among self-employed Canadians)

- ✅ Your budget is already stretched to maximum capacity

- ✅ You prioritize payment certainty over potential savings

- ✅ You’re planning major life changes (career shift, family expansion)

- ✅ You lose sleep worrying about rate increases

Leveraging New Mortgage Programs

Toronto first-time buyers refinancing in 2026 may benefit from recent policy changes. The introduction of 30-year amortization for first-time buyers’ mortgages on new homes can reduce monthly payments regardless of rate type chosen.

Additionally, programs like Ontario’s new secondary suite refinancing program allow first-time buyers to refinance while adding rental income potential, which can offset the risk of variable rate increases.

Strategic Refinancing Approaches for 2026

Hybrid Strategies: The Best of Both Worlds

Rather than choosing strictly fixed or variable, sophisticated first-time buyers in Toronto are exploring hybrid approaches that balance risk and reward:

1. Split Mortgage Strategy

- Allocate 60% to variable rate (maximize savings)

- Allocate 40% to fixed rate (ensure payment stability)

- Benefit from variable savings while limiting exposure

2. Variable with Fixed Payment Amount

- Choose variable rate at 3.55%

- Make payments as if rate were 4.25%

- Extra payments reduce principal faster

- Built-in buffer if rates increase

3. Short-Term Fixed with Variable Conversion

- Lock in 2-year fixed rate (often lower than 5-year)

- Reassess in 2028 when rate environment may be clearer

- Maintain flexibility while avoiding immediate variable exposure

Timing Your Refinancing Decision

The timing of your refinancing can significantly impact outcomes. Current market conditions suggest:

Optimal Timing Indicators:

📅 Early 2026 (Now): Excellent time to lock in variable rates before any potential increases

📅 Mid-2026: Monitor Bank of Canada announcements; if rate cuts are signaled, variable becomes even more attractive

📅 Late 2026: If your renewal isn’t until Q4, waiting could capture any rate decreases

Red Flags to Watch:

- 🚩 Inflation rising above 3% consistently

- 🚩 Bank of Canada shifting to hawkish language

- 🚩 U.S. Federal Reserve beginning aggressive rate increases

- 🚩 Canadian employment data showing significant weakening

For guidance on optimal timing, our article on the best time to renew a mortgage offers valuable insights.

Negotiation Leverage in 2026

First-time buyers refinancing in 2026 hold more negotiating power than many realize. With variable rates surging 25.7% in popularity year-over-year, lenders are competing aggressively for refinancing business.

Negotiation Tactics:

💪 Shop Multiple Lenders: Don’t accept your current lender’s first offer—competitors may beat it by 0.10-0.20%

💪 Leverage Your Payment History: Perfect payment records justify requesting rate discounts

💪 Bundle Products: Some lenders offer rate reductions for holding multiple products (checking, savings, credit cards)

💪 Use Broker Networks: Mortgage brokers access wholesale rates unavailable to retail customers

💪 Request Rate Holds: Lock in current rates while shopping, protecting against increases during your search

Making Your Decision: Fixed vs Variable Rates for Toronto First-Time Buyers Refinancing in 2026

Decision Framework

To determine which option saves more for your specific situation, work through this framework:

Step 1: Calculate Your Payment Capacity

- Current monthly payment: $_______

- Maximum comfortable payment: $_______

- Buffer amount (difference): $_______

Step 2: Assess Risk Tolerance

- Rate this statement on 1-10 scale: “I can handle my payment increasing by $100-150/month without significant stress”

- Score 1-4: Consider fixed rates

- Score 5-7: Hybrid approach may be optimal

- Score 8-10: Variable rates likely suitable

Step 3: Project Your Housing Timeline

- Do you plan to stay in your current home beyond 5 years?

- Are you considering upgrading, downsizing, or relocating?

- Shorter timelines favor variable flexibility

Step 4: Calculate Breakeven Points

Using current rates (3.55% variable vs 3.94% fixed):

- Monthly savings with variable: $122

- If variable rate increases by 0.39% (to match fixed), you break even

- Current forecasts suggest variable rates rising only 0.10% through 2026[6]

- Probability of variable savings: High

Real Toronto Buyer Scenarios

Scenario A: Young Professional in Downtown Condo

- Age: 28, Income: $85,000

- Mortgage: $450,000 on $550,000 condo

- Employment: Stable tech sector job

- Recommendation: Variable rate—maximizes savings, can handle fluctuations, likely to upgrade in 5-7 years

Scenario B: Growing Family in Scarborough

- Age: 35, Income: $110,000 (household)

- Mortgage: $550,000 on $750,000 home

- Employment: One public sector, one commission-based

- Recommendation: 60/40 split (60% variable, 40% fixed)—balances savings with stability for growing family expenses

Scenario C: Self-Employed Entrepreneur

- Age: 32, Income: $95,000 (variable)

- Mortgage: $500,000 on $650,000 townhouse

- Employment: Business owner, income fluctuates

- Recommendation: Fixed rate—payment certainty crucial with variable income, peace of mind worth premium

Common Mistakes to Avoid When Refinancing

Pitfall #1: Focusing Only on Rate

Many first-time buyers make the critical error of choosing based solely on the advertised rate without considering:

❌ Prepayment penalties on existing mortgages ❌ Refinancing fees (appraisal, legal, administration) ❌ Restrictions on lump-sum payments or payment increases ❌ Portability if you plan to move

Solution: Calculate the effective rate including all costs over your expected holding period.

Pitfall #2: Ignoring Mortgage Features

The lowest rate isn’t always the best deal. Critical features include:

✔️ Prepayment privileges: Ability to pay 10-20% annually without penalty ✔️ Payment flexibility: Options to increase payments or make lump sums ✔️ Portability: Transfer mortgage to new property without penalty ✔️ Convertibility: Switch from variable to fixed without penalty (crucial for variable-rate borrowers)

Pitfall #3: Overestimating Risk Tolerance

Many first-time buyers choose variable rates based on potential savings but discover they can’t psychologically handle payment fluctuations. If rate anxiety will impact your quality of life, the savings aren’t worth it.

Pitfall #4: Neglecting to Stress-Test

Before committing to variable rates, stress-test your budget:

- Can you afford payments if rates increase by 1%?

- What if rates increase by 2%?

- Do you have emergency savings to cover 6 months of higher payments?

If the answer to any question is “no,” fixed rates provide necessary security.

Expert Insights: What Mortgage Professionals Are Recommending

Current Industry Consensus

Mortgage professionals across Toronto are observing a clear trend: variable rates are experiencing a renaissance in 2026 after years of fixed-rate dominance. The combination of competitive variable rates below 4%, stable Bank of Canada policy, and the painful renewal shock facing fixed-rate holders has shifted sentiment.

Key Professional Recommendations:

🎯 For Risk-Tolerant Buyers: Variable rates offer compelling value with limited downside risk given current forecasts

🎯 For Conservative Buyers: Even fixed rates at 3.94% are historically reasonable; the certainty may justify the premium

🎯 For Undecided Buyers: Convertible variable mortgages provide an ideal middle ground—start variable, convert to fixed if circumstances change

The Convertibility Safety Net

One of the most powerful features available to Toronto first-time buyers in 2026 is variable-rate convertibility. Most lenders allow borrowers to convert from variable to fixed at any time without penalty.

This creates an asymmetric opportunity:

- ✅ Start with variable rates at 3.55%

- ✅ Enjoy immediate savings of $122/month

- ✅ Monitor rate environment quarterly

- ✅ Convert to fixed if Bank of Canada signals aggressive rate increases

- ✅ Worst case: you saved money for several months before converting

This strategy effectively provides “free insurance”—you benefit from variable savings while retaining the option to lock in fixed certainty if conditions deteriorate.

Looking Ahead: Rate Forecasts Through 2026 and Beyond

What the Data Suggests

Based on current economic indicators and Bank of Canada guidance, the rate outlook for Toronto first-time buyers refinancing in 2026 appears relatively benign:

2026 Forecast Summary:

| Quarter | Variable Rate Projection | Fixed Rate Projection | Confidence Level |

|---|---|---|---|

| Q1 2026 | 3.55% | 3.94% | High |

| Q2 2026 | 3.55-3.60% | 3.90-3.95% | Medium-High |

| Q3 2026 | 3.60-3.65% | 3.95-4.00% | Medium |

| Q4 2026 | 3.60-3.70% | 4.00-4.10% | Medium |

Sources: [4][6][7]

The Bank of Canada’s commitment to stable policy through most of 2026 provides unusual certainty for variable-rate borrowers. Major financial institutions, including TD, RBC, and Scotiabank, forecast no policy rate changes until late 2026 at the earliest.[4]

Potential Game-Changers

While the base case suggests stability, first-time buyers should monitor these potential disruptors:

⚠️ Global Economic Shocks: Geopolitical events or financial crises could trigger rapid policy changes

⚠️ Inflation Resurgence: If inflation rebounds above 3%, the Bank of Canada may resume rate increases

⚠️ U.S. Policy Divergence: Significant rate increases by the U.S. Federal Reserve could pressure Canadian rates upward

⚠️ Housing Market Correction: Sharp price declines could trigger policy responses affecting rates

That said, current indicators suggest these scenarios remain low-probability events for 2026.

Taking Action: Your Next Steps

Immediate Actions for Toronto First-Time Buyers

If you’re refinancing in 2026, take these steps now:

1. Review Your Current Mortgage (This Week)

- Note your maturity date and current rate

- Calculate remaining balance

- Review prepayment penalties and restrictions

- Identify any special features worth preserving

2. Assess Your Financial Situation (This Week)

- Calculate maximum comfortable monthly payment

- Review emergency fund adequacy

- Evaluate income stability and career outlook

- Determine true risk tolerance

3. Shop the Market (Next 2 Weeks)

- Contact at least 3-5 lenders or mortgage brokers

- Request quotes for both fixed and variable options

- Compare total costs, not just rates

- Ask about convertibility, prepayment privileges, and portability

4. Run the Numbers (Next 2 Weeks)

- Calculate 5-year total cost for each option

- Stress-test budget with rate increases of 0.5%, 1.0%, and 1.5%

- Factor in all fees and costs

- Consider tax implications if refinancing for debt consolidation

5. Make Your Decision (Before Renewal Date)

- Lock in rate hold (typically 90-120 days)

- Continue monitoring market conditions

- Finalize choice 30-45 days before renewal

- Complete all documentation promptly

Resources for Further Research

Toronto first-time buyers should leverage these additional resources:

📚 Educational Content: Our guide on how to save and buy your first home provides comprehensive planning strategies

📚 Market Updates: Stay informed about fixed mortgage rate increases amid declining bond yields in Canada to understand rate dynamics

📚 Alternative Options: Explore when it’s a good idea to refinance your mortgage beyond just rate considerations

Conclusion: Which Saves More for Toronto First-Time Buyers?

The question of Fixed vs Variable Rates for Toronto First-Time Buyers Refinancing in 2026: Which Saves More? has a clear answer based on current data: variable rates offer superior savings potential for most first-time buyers who can tolerate modest payment fluctuations.

With variable rates at 3.55% versus fixed rates at 3.94%, the immediate savings of approximately $122 monthly ($1,464 annually) compound significantly over a typical 5-year term. Combined with Bank of Canada forecasts suggesting stable rates through most of 2026, the risk-reward profile favors variable rates for the majority of refinancing scenarios.[1][2][6]

However, the “right” choice ultimately depends on your unique circumstances:

Choose Variable If: You have stable income, adequate emergency savings, and can comfortably absorb potential payment increases of 10-15%. The statistical probability of significant savings is high.

Choose Fixed If: You prioritize payment certainty, have variable income, or operate on a tight budget where unexpected increases would cause genuine hardship. The peace of mind justifies the premium.

Consider Hybrid If: You want to balance both objectives—capture some variable savings while maintaining a foundation of fixed-rate stability.

The current environment represents what industry experts are calling a “rare opportunity” for first-time buyers refinancing in 2026.[3] Rates remain historically reasonable, the Bank of Canada has provided clear forward guidance, and competitive pressure among lenders creates negotiating leverage.

Your Action Plan

Don’t let your mortgage simply auto-renew at your current lender’s posted rates. Take control of your refinancing decision:

- Calculate your specific savings using current rates and your mortgage balance

- Honestly assess your risk tolerance and budget flexibility

- Shop aggressively among multiple lenders and brokers

- Consider convertible variable as a low-risk entry point

- Make an informed decision based on data, not fear

The difference between a strategic refinancing decision and a passive renewal could mean thousands of dollars in savings over your mortgage term. For Toronto first-time buyers navigating one of Canada’s most expensive housing markets, those savings can make a meaningful difference in building long-term wealth.

The mortgage landscape in 2026 favors informed, proactive borrowers. Armed with the insights in this guide, you’re now equipped to make the refinancing choice that maximizes your savings while aligning with your financial goals and risk tolerance.

References

[1] What Can Mortgage Borrowers Expect In 2026 – https://www.ratehub.ca/blog/what-can-mortgage-borrowers-expect-in-2026/

[2] Mortgage Report – https://rates.ca/mortgage-report

[3] Watch – https://www.youtube.com/watch?v=1sXVb_8v75A

[4] Mortgage Rates Forecast Canada – https://www.nesto.ca/mortgage-basics/mortgage-rates-forecast-canada/

[5] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast

[6] Canada Interest Rate Forecast – https://myperch.io/canada-interest-rate-forecast/

[7] Mortgage Rate Forecast – https://www.truenorthmortgage.ca/blog/mortgage-rate-forecast