March 10, 2026

Mortgage Renewal Calculator Canada: How to Estimate Your 2026 Payment Increase

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Last updated: March 10, 2026

Key Takeaways

- Over 1.2 million Canadian mortgages are renewing in 2026, many at rates 2–4 percentage points higher than pandemic-era lows. [1]

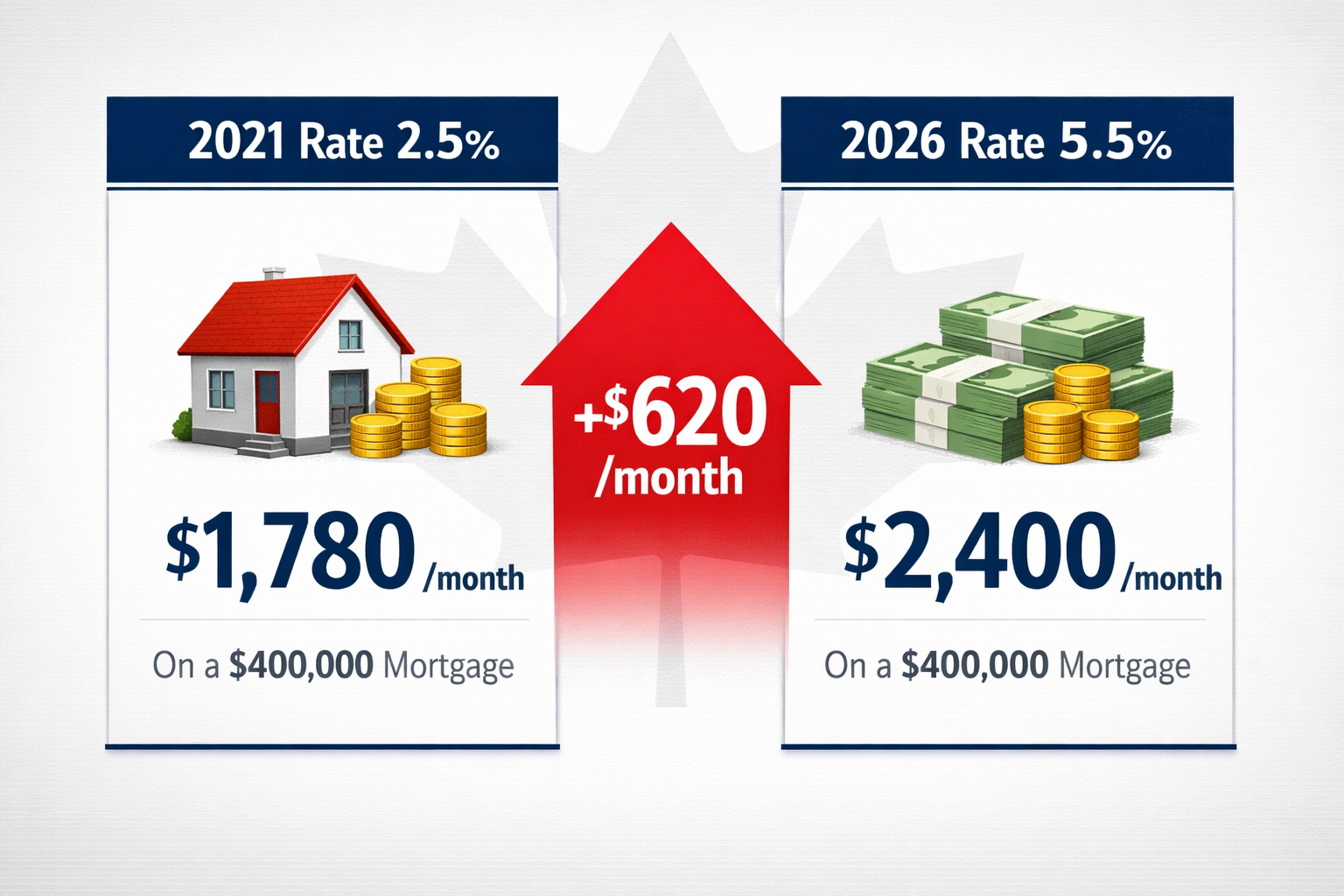

- A $400,000 mortgage originally locked in at 2.5% renewing at 5.5% with 20 years remaining will see monthly payments jump by roughly $620 — a 29% increase. [1]

- The Bank of Canada estimates that 60% of mortgages renewing in 2025–2026 will face higher payments, with 5-year fixed renewals averaging 15–20% payment shocks. [6]

- CMHC projects an average monthly payment increase of $516 for 2026 renewals; Ontario and BC absorb 58% of the national impact. [3]

- As of March 10, 2026, the best 5-year fixed renewal rate is 3.69% (ON, QC, BC, AB) and the best 5-year variable is 3.35% nationwide. [2]

- Free tools like the Ratehub mortgage renewal calculator let borrowers estimate new payments and compare lender offers before committing. [9]

- Shopping for renewal rates at least 120 days before your term ends gives you room to negotiate or switch lenders without penalty.

- Extending amortization by 5 years is one of the most effective ways to reduce monthly payment shock — but it increases total interest paid.

- Hardship renewal applications have a 78% approval rate with major lenders, so struggling borrowers have real options. [3]

Quick Answer

A mortgage renewal calculator Canada tool estimates your new monthly payment by applying a current renewal rate to your remaining mortgage balance and amortization. For most Canadians renewing in 2026, payments will be $400–$620 higher per month compared to 2020–2021 terms. Use a free calculator (like Ratehub’s), input your remaining balance, current rate, new rate, and remaining amortization, then compare the output against your budget to decide whether to extend amortization, switch lenders, or make a lump-sum payment.

What Is a Mortgage Renewal Calculator and How Does It Work?

A mortgage renewal calculator estimates what your monthly payment will be when your current term ends and you sign a new one. It applies a new interest rate to your outstanding principal balance over whatever amortization period remains (or a new one you choose).

Inputs you need:

- Remaining mortgage balance (check your latest statement)

- Current interest rate and remaining term

- New interest rate (use today’s best available rates as a benchmark)

- Remaining amortization period (in years)

- Payment frequency (monthly, bi-weekly, accelerated)

What it outputs:

- New monthly (or bi-weekly) payment amount

- Total interest paid over the new term

- Side-by-side comparison of old vs. new payment

💡 Pull quote: “The calculator doesn’t just show you a number — it shows you the gap between what you pay now and what you’ll pay next, which is where the real planning starts.”

Common mistake: Many borrowers only input their original rate and balance, forgetting that their balance has decreased over 5 years. Always use your actual remaining balance, not the original mortgage amount. Your lender’s annual statement or online portal will show this.

Why Are 2026 Mortgage Renewals So Different From Previous Years?

2026 renewals are uniquely painful because millions of Canadians locked in 5-year fixed rates during 2020–2021 at historic lows — often between 1.5% and 2.5%. Those terms are now expiring into a rate environment that, while improved from 2023 peaks, is still significantly higher. [5]

The scale of the problem:

- Approximately 1.2 million mortgages are renewing in 2026. [1]

- Major Canadian lenders (TD, Scotiabank, BMO, CIBC, National Bank, Desjardins) had roughly $154 billion in mortgages renewing in the 6 months following Q3 2025, and another $209 billion renewing into mid-2026. [7]

- BMO Economics identified a peak renewal wave of approximately 1.8 million mortgages in the 12 months from September 2025, cresting around June 2026. [10]

Payment shock by mortgage type (Bank of Canada estimates): [6]

| Mortgage Type | Average Payment Increase | Notes |

|---|---|---|

| 5-year fixed (2020–2021 vintage) | 15–20% | Most common scenario |

| Variable-rate, fixed payment | Wide variance; top 10% see >40% | Depends on trigger rate history |

| 3-year fixed (2022–2023 vintage) | 5–10% | Renewing at closer-to-peak rates |

The Bank of Canada’s analysis found that the median debt service ratio for renewing borrowers rises by 2.7 percentage points to approximately 18%, up from 15.3% at the end of 2024. [6] That’s manageable for most households — but not all.

For context on how Bank of Canada policy decisions drove rates to these levels and what might happen next, see The Impact of Bank of Canada’s Policy Decisions on Your Mortgage.

How to Use a Mortgage Renewal Calculator Canada: Step-by-Step

Using a mortgage renewal calculator in Canada takes about five minutes and requires only a few numbers from your mortgage statement.

Step 1: Find your remaining balance Log into your lender’s online portal or check your most recent annual mortgage statement. This is the principal you still owe — not the original loan amount.

Step 2: Confirm your remaining amortization If you started with a 25-year amortization and have been paying for 5 years, you likely have 20 years remaining (assuming no changes to payment schedule).

Step 3: Enter today’s best available renewal rate As of March 10, 2026, the best 5-year fixed renewal rate is 3.69% and the best 5-year variable is 3.35%. [2] Use these as benchmarks, not your lender’s first offer — which is typically higher.

Step 4: Run multiple scenarios

- Scenario A: Accept your lender’s posted renewal rate

- Scenario B: Apply the best available market rate

- Scenario C: Extend amortization by 5 years at the market rate

- Scenario D: Make a lump-sum prepayment before renewal, then apply the market rate

Step 5: Compare total cost, not just monthly payment A longer amortization lowers your monthly payment but increases total interest paid. The calculator will show both.

Step 6: Shop and negotiate Take your calculator results to a mortgage broker or competing lenders. You can lock in a rate up to 120 days before renewal at most lenders without penalty. [9]

For a deeper look at how switching lenders or refinancing at renewal works, see Mortgage Tips: How to Refinance Your Mortgage to Save Money.

What Payment Increase Should You Expect in 2026?

The answer depends on your original rate, remaining balance, and what rate you renew at. Here are concrete examples based on verified data.

Example 1: $400,000 balance, 20 years remaining

| Original Rate | Renewal Rate | Old Payment | New Payment | Monthly Increase |

|---|---|---|---|---|

| 2.5% | 5.5% | ~$1,780 | ~$2,400 | +$620 (+29%) |

| 2.5% | 3.69% | ~$1,780 | ~$2,050 | +$270 (+15%) |

| 1.99% | 3.69% | ~$1,700 | ~$2,050 | +$350 (+21%) |

Source: Estimates based on standard mortgage payment formula; renewal rate benchmarks from Ratehub.ca as of March 10, 2026. [1][2]

Example 2: $500,000 balance, 20 years remaining

| Original Rate | Renewal Rate | Old Payment | New Payment | Monthly Increase |

|---|---|---|---|---|

| 2.0% | 5.5% | ~$2,125 | ~$3,000 | +$875 (+41%) |

| 2.0% | 3.69% | ~$2,125 | ~$2,565 | +$440 (+21%) |

📌 Key insight: Getting the best available market rate instead of accepting your lender’s posted offer can cut your payment shock roughly in half on a $400,000 balance.

CMHC projects the average monthly payment increase for 2026 renewals at $516. Ontario homeowners (38% of all renewals, roughly 438,000 households) and BC homeowners (20%) absorb 58% of the national impact. [3]

Fixed vs. Variable Rate: Which Should You Choose at Renewal?

For most borrowers renewing in 2026, a 5-year fixed rate offers more predictability, while a variable rate offers a lower starting payment with more risk. The right choice depends on your income stability, risk tolerance, and how long you plan to stay in the home.

As of March 10, 2026: [2]

- Best 5-year fixed renewal rate: 3.69% (ON, QC, BC, AB)

- Best 5-year variable renewal rate: 3.35% nationwide

The gap between fixed and variable is relatively narrow right now (about 0.34 percentage points). That means the variable rate’s cost advantage is smaller than usual, while the fixed rate’s certainty is fully intact.

Choose fixed if:

- Your income is salaried or predictable

- You’re already stretched by the payment increase

- You want to budget with certainty for the next 5 years

- You’re concerned about global economic uncertainty affecting Canadian rates

Choose variable if:

- You have financial flexibility to absorb potential rate increases

- You believe rates will fall further over the next 1–2 years

- You may sell or refinance before the term ends (variable rates typically have lower prepayment penalties)

- Your remaining amortization is short (less than 10 years)

For a detailed breakdown of how fixed and variable mortgages compare across different scenarios, see the Mortgage Rate Guide: Fixed or Variable Mortgage Options.

How Can You Reduce Your 2026 Renewal Payment Shock?

There are several practical strategies to lower the payment increase at renewal — some require action before your renewal date, others can be negotiated at signing.

1. Shop the market early (120 days out) Your current lender’s renewal offer is rarely their best rate. A mortgage broker can access rates from dozens of lenders simultaneously. The best available 5-year fixed rate as of March 2026 is 3.69% — well below what most major banks post as their “standard” renewal rate. [2][9]

2. Make a lump-sum prepayment Most mortgages allow 10–20% annual prepayments without penalty. Applying a lump sum before renewal reduces your principal, which directly lowers your new payment. Even $10,000–$20,000 can make a meaningful difference.

3. Extend your amortization Extending from 20 to 25 years spreads payments over a longer period, reducing the monthly amount. On a $400,000 balance at 4.5%, extending by 5 years can reduce monthly payments by roughly $300–$400 compared to keeping the original amortization. [5] About half of borrowers facing significant payment shocks can offset the increase this way. [3]

4. Switch to accelerated bi-weekly payments This doesn’t lower your payment — it actually increases total annual payments slightly — but it reduces your amortization faster and saves significant interest. See Maximize Your Mortgage: The Power of Biweekly Payments for a full breakdown.

5. Apply for a hardship renewal If your financial situation has changed significantly, ask your lender about hardship provisions. Hardship renewal applications have a 78% approval rate with major lenders, and options can include extended amortization, temporary payment deferrals, or blended rate arrangements. [3]

6. Consider refinancing If you have significant home equity, refinancing to consolidate high-interest debt alongside your renewal can improve your overall cash flow even at a higher mortgage rate. See Mortgage Tips: How to Refinance Your Mortgage to Save Money for details.

For borrowers who have experienced credit challenges since their original mortgage, improving your credit score before renewal can also unlock better rates. See How to Improve Your Credit Score in Canada.

What Happens If You Can’t Afford Your Renewal Payment?

If your new renewal payment is unaffordable, you have more options than most borrowers realize — but acting early is critical. Waiting until you’ve missed payments significantly narrows your choices.

Options to explore, in order of preference:

Negotiate with your current lender — Ask specifically about extended amortization, blended rate options, or a hardship program. Document your income and expenses before the conversation.

Switch lenders at renewal — Switching at renewal (not mid-term) typically carries no penalty. A broker can find lenders with more flexible qualification criteria.

Refinance to access equity — If your home has appreciated, refinancing can provide cash flow relief, though it resets your amortization and may increase total interest costs.

Consider a longer term — A 3-year fixed instead of 5-year gives you a chance to renew again sooner if rates drop further.

Explore the renewal denial path — If your lender declines to renew (rare, but possible), understand your rights and alternatives. See What Happens If Your Mortgage Renewal Is Denied for a full guide.

Edge case: Variable-rate borrowers with fixed payments who hit their trigger rate during 2022–2023 may have already been making interest-only payments. At renewal, their full amortization resets — meaning their payment shock can be significantly larger than the average figures above. [6]

FAQ: Mortgage Renewal Calculator Canada

Q: What is the best free mortgage renewal calculator in Canada? Ratehub.ca offers a free mortgage renewal calculator that estimates new payments, compares lender rates, and shows amortization schedules. It’s updated regularly with current market rates. [9]

Q: How much will my mortgage payment increase at renewal in 2026? The average increase for 2026 renewals is projected at $516/month (CMHC estimate). On a $400,000 balance renewing from 2.5% to 5.5%, the increase is roughly $620/month. Renewing at the best available rate of 3.69% instead reduces that to about $270/month. [1][3]

Q: Can I lock in a renewal rate early? Yes. Most Canadian lenders allow you to lock in a renewal rate 120 days (about 4 months) before your term ends, without penalty. This protects you if rates rise before your renewal date.

Q: Should I renew with my current lender or switch? Compare your lender’s offer against the best available market rates before deciding. Switching at renewal carries no penalty, and a mortgage broker can access rates from many lenders simultaneously. The rate difference can easily be $200–$400/month on a mid-sized mortgage.

Q: What is the best mortgage term to choose at renewal in 2026? Most borrowers are choosing 3-year or 5-year fixed terms. A 5-year fixed at 3.69% locks in certainty; a 3-year fixed allows you to renew again sooner if rates fall further. Variable rates at 3.35% offer a lower starting point but carry rate risk. [2]

Q: Can I extend my amortization at renewal to lower my payment? Yes. Most lenders allow amortization extensions at renewal, up to the maximum allowed period (25 years for insured mortgages, 30 years for uninsured in some cases). This lowers monthly payments but increases total interest paid over the life of the mortgage.

Q: Does renewing my mortgage require a new stress test? If you stay with your current lender, no stress test is required at renewal. If you switch lenders, you will need to qualify under the current stress test rules. See the mortgage stress test guide for current thresholds.

Q: What if my financial situation has changed since I got my mortgage? If your income has dropped, you’ve changed jobs, or your credit has been affected, switching lenders at renewal may be harder. Work with a broker who can assess your full picture and find lenders suited to your current situation.

Q: How does the 2026 renewal wave affect the broader housing market? The renewal wave is adding financial pressure on existing homeowners, which can dampen discretionary spending and slow housing market activity. For a broader view, see the analysis on Canada’s mortgage renewal wall.

Q: Are there any government programs to help with 2026 mortgage renewals? As of March 2026, there is no specific federal program targeting renewal payment shock. However, CMHC’s mortgage deferral guidelines and lender hardship programs remain available. Contact your lender directly and ask about all available options.

Conclusion: What to Do Before Your 2026 Renewal

The 2026 mortgage renewal landscape is challenging, but it’s manageable with the right preparation. Here’s a concise action plan:

✅ Action checklist for 2026 mortgage renewal:

- Calculate your payment increase now — Use a free mortgage renewal calculator with your actual remaining balance, not your original loan amount. Ratehub.ca’s tool is a solid starting point. [9]

- Start shopping 120 days before your renewal date — The best available 5-year fixed rate as of March 2026 is 3.69%, which is significantly lower than most lenders’ posted renewal rates. [2]

- Run multiple scenarios — Compare keeping your current amortization vs. extending it, and fixed vs. variable, side by side.

- Consider a lump-sum prepayment — Even a modest prepayment before renewal reduces your principal and lowers your new payment.

- Talk to a mortgage broker — Brokers access multiple lenders and can often secure rates unavailable directly from banks. See Mortgage Broker vs. Bank to understand the difference.

- If you’re struggling, ask about hardship options early — Hardship renewal approvals run at 78% with major lenders. [3] Early conversations produce better outcomes than waiting.

- Don’t auto-renew without comparing — Accepting your lender’s first offer without shopping is the single most expensive mistake renewal borrowers make.

The payment shock is real, but the gap between the worst-case scenario (auto-renewing at a posted rate) and the best-case scenario (shopping the market and negotiating) can easily be $300–$500 per month. That difference is worth a few hours of research.

References

[1] Mortgage Shock – https://www.collectorhq.ca/calculators/mortgage-shock/ [2] Mortgage Renewal Rates – https://www.ratehub.ca/mortgage-renewal-rates [3] Watch – https://www.youtube.com/watch?v=cj_E35jCzTE [5] Mortgage Renewal Crisis 2026 – https://www.collectorhq.ca/crisis/mortgage-renewal-crisis-2026/ [6] 60 Of Canadian Mortgage Renewals To Face Higher Rates By 2026 Boc – https://www.canadianmortgagetrends.com/2025/01/60-of-canadian-mortgage-renewals-to-face-higher-rates-by-2026-boc/ [7] Mortgage Renewals Of Major Canadian Lenders – https://wowa.ca/infographics-finance-realestate-canada/mortgage-renewals-of-major-canadian-lenders [9] Mortgage Renewal Calculator – https://www.ratehub.ca/mortgage-renewal-calculator [10] BMO Economics Renewal Wave – https://economics.bmo.com/en/publications/detail/f9a87ba8-9962-4265-a2a9-e51303e269ca/

Tags: mortgage renewal calculator Canada, 2026 mortgage renewal, mortgage payment increase, Canadian mortgage rates, mortgage renewal shock, fixed vs variable mortgage, mortgage renewal strategies, Bank of Canada mortgage, CMHC renewal, mortgage amortization extension, mortgage broker Canada, refinancing at renewal