March 19, 2026

Shorter-Term Private Mortgages in Toronto: Capitalizing on 71% New Borrower Trend for 2026 Rate Flexibility

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

🏙️ Toronto’s mortgage market is shifting fast — and borrowers who understand the data are positioning themselves ahead of the curve.

In 2026, a striking trend has emerged from Bank of Canada research: 71% of mortgages originated in 2024 carried fixed terms under five years [2]. This isn’t a coincidence. It reflects a deliberate strategy by new borrowers to stay nimble in a volatile rate environment. The concept of Shorter-Term Private Mortgages in Toronto: Capitalizing on 71% New Borrower Trend for 2026 Rate Flexibility sits at the heart of this shift — and for many Toronto homeowners, private lenders are making this strategy not just possible, but practical.

Key Takeaways 📌

- 71% of 2024-originated mortgages chose fixed terms under five years, signaling a broad preference for rate flexibility [2]

- Private mortgages now represent 15.8% of Ontario’s mortgage market by count, driven by bank inflexibility during the 2026 renewal wave [3]

- Private lenders offer 6-month to 3-year terms at 8.99–13.99%, with approvals in as little as 24–48 hours [3][5]

- The Bank of Canada held its policy rate at 2.25% in March 2026, but 60% of renewing borrowers still face payment increases [2]

- Short-term private mortgages act as a strategic bridge — not a last resort — for borrowers expecting rates to ease further by late 2026

Why 71% of New Borrowers Are Choosing Shorter Terms in 2026

The Bank of Canada’s own data tells a compelling story. Among mortgages originated in 2024, 74% of low-ratio borrowers chose fixed terms shorter than five years [2]. The reasoning is straightforward: with rate forecasts pointing to further movement through 2026, locking into a long-term deal feels like a gamble.

💬 “Borrowers aren’t being reckless — they’re being strategic. Shorter terms mean more chances to refinance at a better rate.”

TD Economics confirmed in March 2026 that average payment increases for renewing borrowers have dropped to around 6% in 2026, down from 10% in 2025 — a sign that the worst of the renewal shock is easing [1]. Still, one-third of mortgage holders will still face increases, and Ontario alone accounts for 38% of the 438,000 national renewals expected this year [2][3].

For borrowers who don’t fit neatly into bank qualification boxes — the self-employed, those with recent credit challenges, or investors with complex income — shorter-term private mortgages offer the same rate flexibility that the 71% trend captures, but with far greater access.

Understanding how private lenders work and what they can offer is the first step to using this strategy effectively.

Understanding Shorter-Term Private Mortgages in Toronto: Capitalizing on 71% New Borrower Trend for 2026 Rate Flexibility

What Makes Private Mortgages Different?

Private lenders operate outside the traditional banking system. They focus on equity in the property rather than rigid income verification or stress test thresholds. This makes them especially valuable in Toronto’s high-cost housing environment, where asset values often outpace what banks are willing to acknowledge.

As Lendworth Capital noted in 2026: “Private mortgages are not a last resort — they are a workable option for borrowers whose assets outpace what banks are willing to acknowledge.” [3]

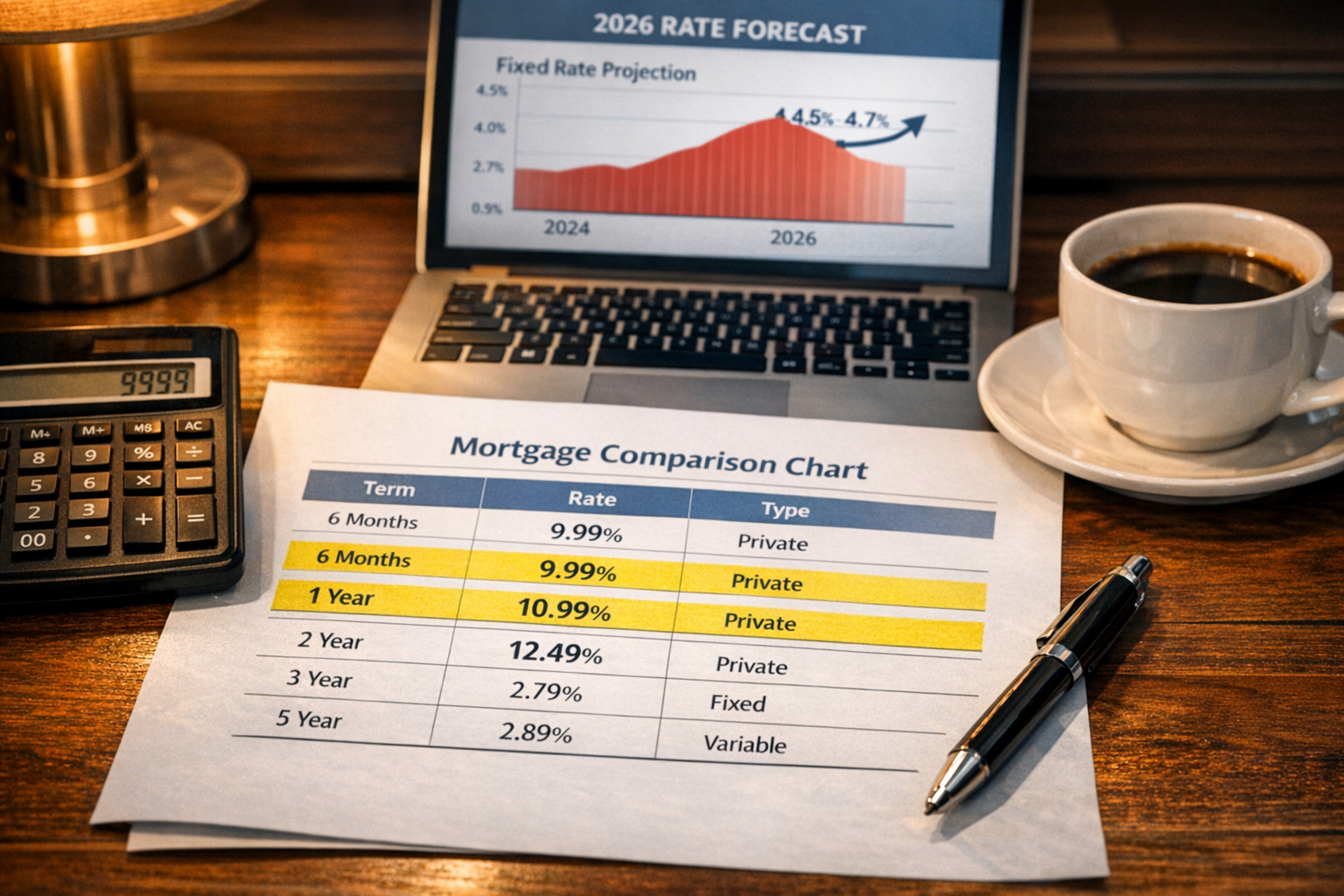

Typical Private Mortgage Terms in 2026

| Feature | Bank Mortgage | Private Mortgage |

|---|---|---|

| Term Length | 1–5 years (typically 5) | 6 months – 3 years |

| Interest Rate | ~3.35% variable (Mar 2026) | 8.99% – 13.99% |

| Approval Time | 2–4 weeks | 24–48 hours |

| Income Verification | Strict (T4, NOA, stress test) | Flexible (equity-based) |

| Amortization | Up to 30 years (some lenders) | Typically 25–30 years |

| Best For | Qualified salaried borrowers | Complex income, renewal denied |

Sources: [3][5]

The Rate Flexibility Argument

Fixed rates are forecast to rise to 4.5–4.7% by year-end 2026 [1]. For a borrower who takes a 1-year private mortgage today, that creates a defined decision point: reassess, refinance, or transition back to a bank product — whichever makes the most sense at renewal.

This mirrors exactly what the 71% of 2024 borrowers were thinking when they avoided long-term locks. The difference is that private mortgages extend this flexibility to borrowers who might not qualify for bank products at all.

Fitch Ratings warned in February 2026 that 1.2 million renewals at higher rates will pressure household finances, especially in high-cost markets like Toronto [6]. Short-term private deals give these households a structured exit ramp.

Who Benefits Most from Short-Term Private Lending in Toronto?

Not every borrower needs a private mortgage. But for specific situations, it can be the smartest tool available. Here’s who tends to benefit most:

🏠 Homeowners Facing Renewal Denials

Bank inflexibility around rental income and updated OSFI appraisal rules has left many Toronto homeowners unable to renew with their existing lender [3]. A 1–2 year private mortgage buys time to restructure finances and re-qualify.

💼 Self-Employed Borrowers

Income documentation challenges are common for business owners and contractors. Private lenders assess the property’s equity rather than a T4 slip. This is especially relevant given how many Toronto professionals fall outside traditional income categories. Learn more about securing mortgage rates without traditional income verification.

🏗️ Real Estate Investors

TRREB forecasts approximately 100,000 sidelined buyers re-entering the GTA market by late 2026 [3]. Investors who need fast financing to capture opportunities can’t wait weeks for bank approvals. Private lenders’ 24–48 hour turnaround is a competitive advantage.

📉 Borrowers with Recent Credit Challenges

A short-term private mortgage can serve as a credit-rebuilding bridge. For guidance on this path, see how to get a mortgage with bad credit in Ontario.

How to Capitalize on the 71% Trend: A Practical Strategy for 2026

Step 1: Assess Your Equity Position

Private lenders in Ontario typically lend up to 75–80% loan-to-value (LTV). Toronto’s property values, despite recent softening, still provide strong equity positions for most homeowners [9]. Calculate your current LTV before approaching any lender.

Step 2: Define Your Exit Strategy

A short-term private mortgage only makes sense if there’s a clear plan for what happens at the end of the term. Common exit strategies include:

- ✅ Refinancing with a bank after improving credit or income documentation

- ✅ Selling the property before term expiry

- ✅ Transitioning to a longer-term product once rates stabilize

Avoid the trap of rolling over private mortgages indefinitely — the higher interest costs compound quickly. Review strategies for accelerated mortgage repayment to stay on track.

Step 3: Understand the True Cost

The rate differential between bank and private products is real. At 10–12% versus 3.35% (variable), the monthly cost is significantly higher. However, for a 12-month bridge, the total premium may be far less than the cost of a forced sale, a missed investment opportunity, or a prolonged credit damage spiral.

💡 Pro Tip: Always compare the total cost of the private term against the cost of alternative scenarios — not just the rate.

Step 4: Work with a Mortgage Broker

Private lenders don’t advertise like banks. Access to the best terms and the most reputable lenders comes through broker relationships. A knowledgeable broker can also help structure the deal to minimize fees and penalties. Explore what a mortgage broker does and how they help.

Also consider reviewing fixed vs. variable rate options to understand how private short-term deals compare to conventional choices.

Step 5: Watch the Rate Environment

The Bank of Canada held its rate at 2.25% in March 2026 [3]. Most economists expect further movement through mid-2026. Borrowers in short-term private deals should monitor BoC announcements closely — the impact of Bank of Canada policy decisions on your mortgage can directly affect the timing of a refinance.

Risks to Keep in Mind ⚠️

Shorter-term private mortgages are a tool, not a cure-all. Key risks include:

- Higher interest rates (8.99–13.99%) significantly increase carrying costs [5]

- Lender fees (typically 1–3% of the mortgage amount) add to the total cost

- Renewal risk — if the exit strategy fails, rolling into another private term compounds costs

- Less regulatory protection compared to federally regulated banks

- Penalty structures vary widely — always read the fine print. See how mortgage penalties work and how to avoid them

Conclusion: Short-Term Thinking for Long-Term Gains 🎯

The 71% new borrower trend isn’t just a statistic — it’s a signal. Toronto’s most informed borrowers are choosing flexibility over false security, and shorter-term private mortgages are giving that same flexibility to those who can’t access it through traditional channels.

In 2026’s complex rate environment, with renewal pressures mounting and fixed rates potentially climbing to 4.5–4.7% by year-end, a well-structured short-term private mortgage can be the bridge between financial stress and a stronger long-term position.

Actionable Next Steps:

- 📊 Calculate your current home equity and LTV ratio

- 🗓️ Map out a 12–24 month exit strategy before signing anything

- 🤝 Consult a licensed mortgage broker with private lending experience

- 📰 Monitor Bank of Canada rate announcements for optimal refinance timing

- 📋 Get a personalized mortgage solution assessment to explore your options

The data is clear. The trend is set. The question is whether Toronto borrowers will use the tools available to them — or wait for the perfect moment that may never come.

References

[1] Watch – https://www.youtube.com/watch?v=lSQJu2PTr7M [2] 60 Of Canadian Mortgage Renewals To Face Higher Rates By 2026 Boc – https://www.canadianmortgagetrends.com/2025/01/60-of-canadian-mortgage-renewals-to-face-higher-rates-by-2026-boc/ [3] Why Toronto Homeowners Are Ditching Banks For Private Mortgages In 2026 Real Stories And Stats – https://everythingmortgages.ca/blog/why-toronto-homeowners-are-ditching-banks-for-private-mortgages-in-2026-real-stories-and-stats/ [4] Short Term Rental Mortgages – https://citadelmortgages.ca/short-term-rental-mortgages/ [5] Private Mortgage – https://citadelmortgages.ca/private-mortgage/ [6] Canadian Mortgage Repricing May Pressure Lower Priority Consumer Debt 23 02 2026 – https://www.fitchratings.com/research/structured-finance/canadian-mortgage-repricing-may-pressure-lower-priority-consumer-debt-23-02-2026 [9] Private Lenders Ontario – https://alpinecredits.ca/alpine-blog/private-lenders-ontario/