March 20, 2026

Toronto’s 2026 Renewal Wave: Why Tightening Bank Criteria Are Forcing Thousands Into Private Mortgages

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Imagine locking in a mortgage at 1.5% in 2021 — only to sit across from a bank manager in 2026 and hear the word “denied.” This is the reality hitting thousands of Toronto homeowners right now. Toronto’s 2026 Renewal Wave: Why Tightening Bank Criteria Are Forcing Thousands Into Private Mortgages is not just a headline — it is a structural shift reshaping how Canadians access home financing, and it is happening faster than most people expected.

Key Takeaways 📌

- ~60% of all outstanding Canadian mortgages are renewing in 2025–2026, creating a historic payment shock cycle [1]

- OSFI’s 2026 rule changes have cut investor borrowing power by up to 23%, making bank renewals harder to qualify for [5]

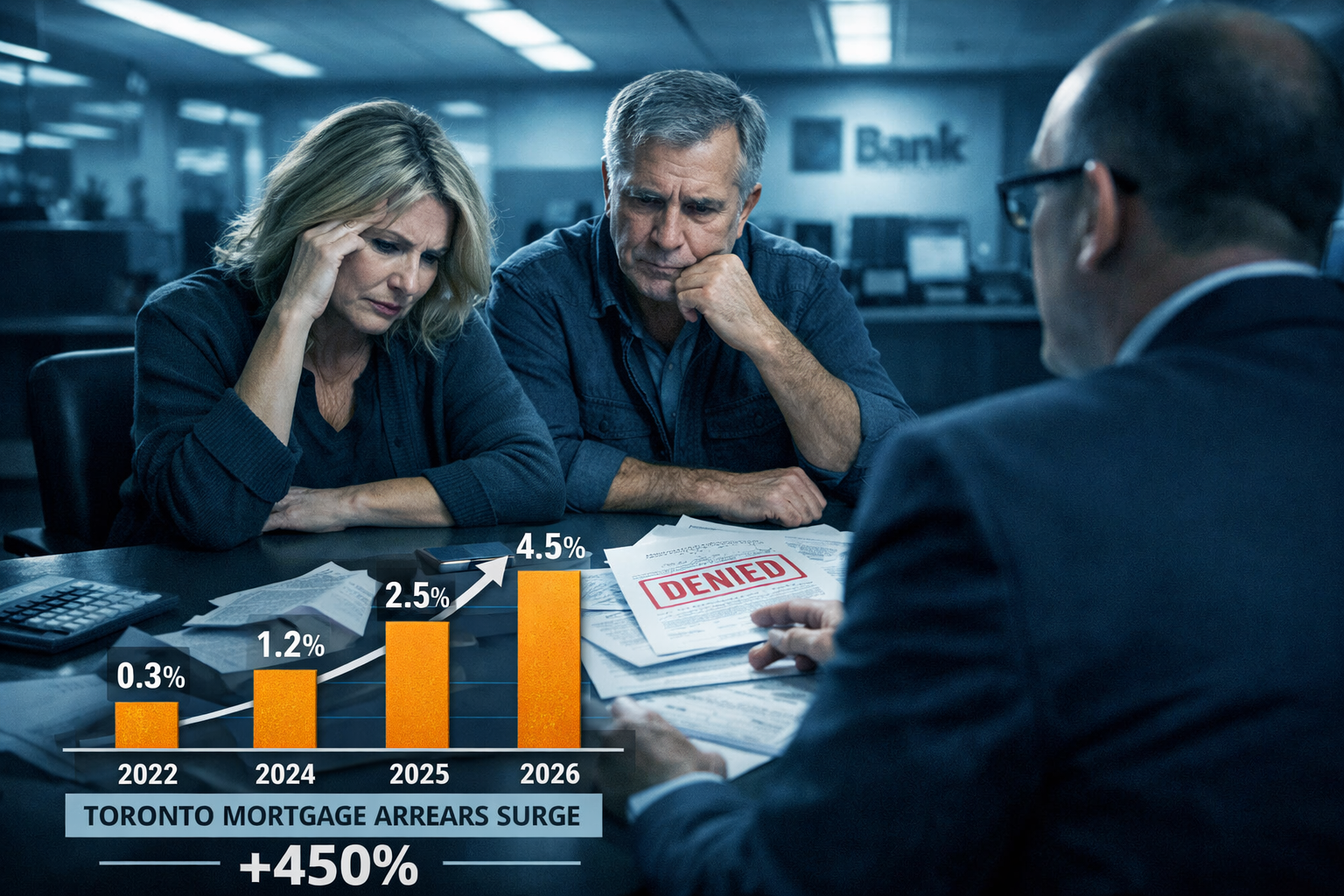

- Mortgage delinquencies in Toronto have surged 450% since Q3 2022, with ~2,797 families now 90+ days behind [9]

- Private lenders are stepping in where banks won’t, approving borrowers based on property equity rather than income alone [4]

- Extended amortizations and FCAC protections are keeping most borrowers afloat — but a vulnerable segment has no bank-side options left

The Scale of Toronto’s 2026 Mortgage Renewal Crisis

To understand why so many Toronto homeowners are being pushed toward private lending, it helps to understand the sheer size of what is happening. Approximately 60% of all outstanding Canadian mortgages are renewing between 2025 and 2026 — the largest renewal cycle in Canadian history [1]. Many of these borrowers locked in at pandemic-era rates between 1.5% and 2.5%. They are now renewing into a world where rates sit dramatically higher.

CMHC reported on February 5, 2026, that Toronto leads all Canadian cities in projected mortgage arrears growth through Q4 2026. The drivers include high household debt loads, investor cash flow problems, declining home prices, and weakness in the GTA labour market [1]. CMHC Deputy Chief Economist Tania Bourassa-Ochoa specifically flagged pandemic-era first-time buyers in high-priced markets like Toronto as the most vulnerable group — high leverage combined with steep rate resets is a dangerous combination.

The numbers are striking. Equifax data from March 2026 shows approximately 2,797 Toronto families are now 90+ days delinquent on their mortgages — a 450% surge since Q3 2022. Projections suggest this number could climb to ~3,500 by mid-2026, right at the June renewal peak [9].

💬 “Pandemic-era first-time buyers in high-priced areas like Toronto are most vulnerable due to high leverage and rate resets.” — CMHC Deputy Chief Economist Tania Bourassa-Ochoa [1]

For variable-rate borrowers with fixed payments, the situation is especially acute. A March 2026 analysis citing Bank of Canada and TD Economics data found that 10% of variable-rate fixed-payment borrowers renewing in 2026 face payment increases of 40% or more — that translates to roughly $700 more per month on a $600,000 mortgage. Many of these households also added $20,000–$50,000 in unsecured debt during the pandemic years [2].

To understand the broader impact of rate resets on renewal outcomes, see this detailed breakdown of how rate resets and the renewal wave are affecting Canadian borrowers.

How Tightening Bank Criteria Are Driving the Private Mortgage Shift

This is where Toronto’s 2026 renewal wave gets structural. It is not just about higher rates — it is about banks applying stricter criteria at renewal, disqualifying borrowers who would have sailed through approval five years ago.

OSFI’s 2026 Rule Changes: A Game-Changer for Investors

OSFI’s updated Capital Adequacy Requirements (CAR 2026), effective January 1, 2026, introduced a critical change: banks can no longer double-count rental income across multiple investment properties when calculating borrowing capacity. The result? Investors and landlords have seen their borrowing power drop by up to 23% overnight [5][8]. A Toronto investor who qualified easily in 2021 may now fall short of the bank’s debt service ratios at renewal — through no fault of their own spending habits.

The Stress Test Trap at Renewal

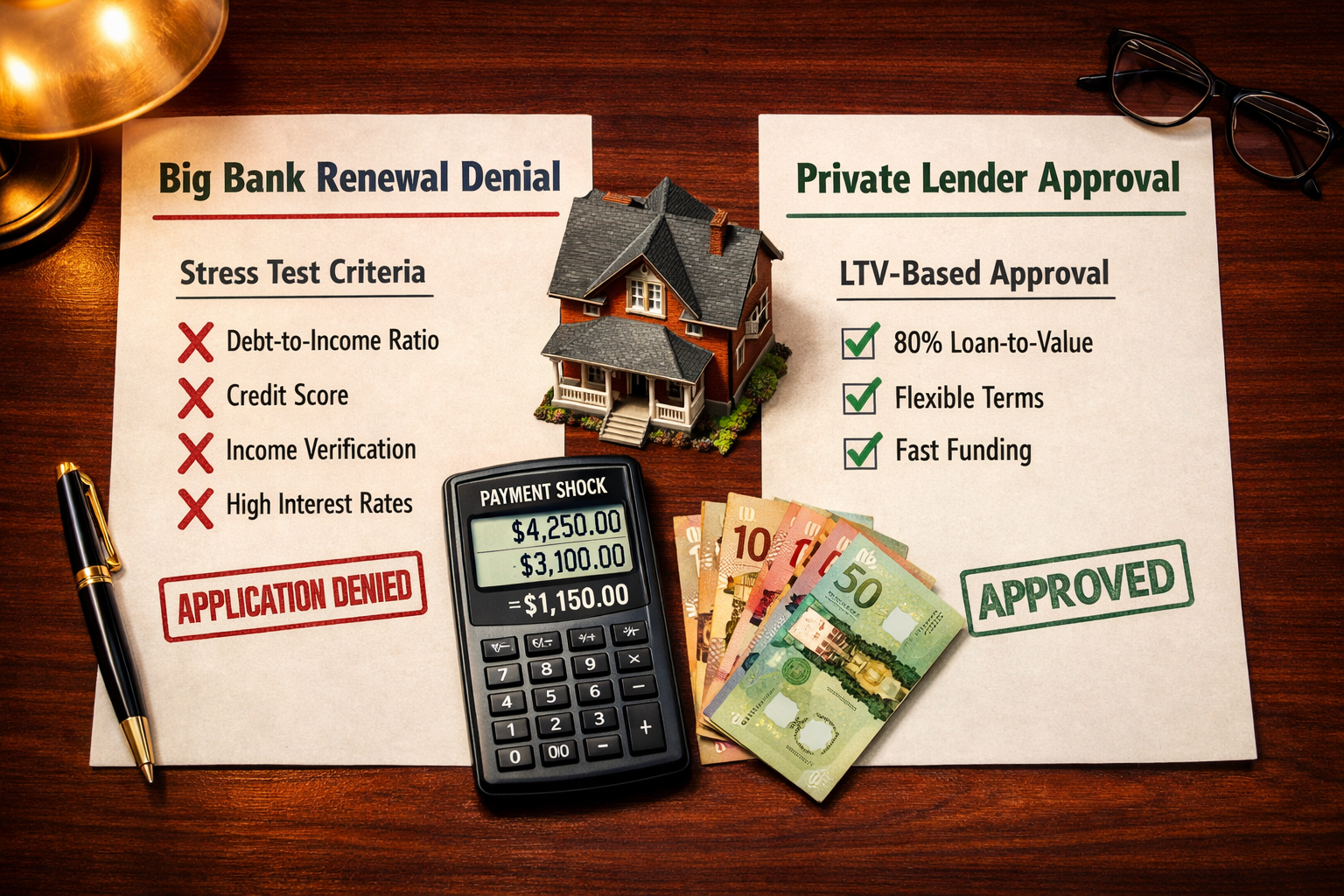

Even for owner-occupiers, the mortgage stress test remains a significant hurdle. Borrowers must qualify at the higher of their contract rate plus 2%, or 5.25%. For someone renewing a $700,000 mortgage, this can mean proving they can afford payments at 7%+ even if their actual rate is 4.9%. Many borrowers — especially the self-employed or those with variable income — simply cannot pass this test at their current bank [3].

Frozen HELOCs, Low Appraisals, and Delayed Renewals

Banks are also freezing HELOCs, delaying renewal approvals, and declining refinances when property appraisals come in lower than expected. In a softening Toronto market, this is increasingly common. As Lendworth noted in February 2026, equity-rich Ontario homeowners are being turned away by banks that focus on income verification, and are finding that private lenders — who focus on loan-to-value (LTV) ratios instead — are their only viable path forward [4].

If your renewal has been denied, understanding what happens when your mortgage renewal is denied is a critical first step.

Who Is Most Affected? 🏠

| Borrower Type | Key Challenge | Likely Outcome |

|---|---|---|

| Pandemic first-time buyers | High LTV + rate shock | Payment stress, may need B-lender |

| Self-employed investors | Rental income rule changes | Reduced qualifying power, private route |

| Variable-rate fixed-payment holders | 40%+ payment jumps | Refinance needed, bank may decline |

| Borrowers with credit bruising | Delinquency history | Private lender as bridge solution |

| Multi-property landlords | OSFI CAR 2026 limits | Up to 23% less borrowing power |

Navigating Your Options: From B-Lenders to Private Mortgages

Being declined by a major bank at renewal does not mean losing your home. The Canadian lending landscape has multiple tiers, and understanding them is essential.

The Lending Tier Breakdown

🏦 Tier 1 — Big Banks (A-Lenders) Strict income verification, stress test required, OSFI rules apply. Best rates but least flexible.

🏢 Tier 2 — B-Lenders (e.g., MCAP, First National, Home Trust) More flexible income criteria, still regulated but with more room for self-employed borrowers or minor credit issues. Rates typically 1–2% higher than big banks. A strong middle-ground option for those who narrowly miss bank criteria.

🤝 Tier 3 — Private Lenders Approval based primarily on property equity and LTV, not income. Higher rates (typically 2–4% above prime), but accessible when banks and B-Lenders say no. Ideal as a bridge solution — not a permanent home [4].

For a full walkthrough of how private lending works, the complete guide to getting a mortgage with a private lender covers everything from rates to approval timelines.

Other Creative Solutions Worth Knowing

- Second mortgages: Tap existing home equity without breaking your first mortgage. Explore Second Mortgage options in Toronto as a way to manage cash flow during renewal stress.

- Refinancing: In some cases, restructuring the entire mortgage makes more sense than renewing. Review when Refinancing your Mortgage makes sense before deciding.

- Vendor Take-Back (VTB) mortgages: Seller financing that bypasses banks entirely, useful in purchase scenarios.

- Extended amortizations: TD Economics data from March 2026 shows 13% of TD mortgages now exceed 35 years — a sign that lenders are using amortization extensions to manage payment shock [2].

A Word of Balance ⚖️

It is important to note that Toronto’s 2026 renewal wave has not caused a market meltdown. Most borrowers are managing. TD Economics forecasts average 2026 payment increases at approximately 6% — down from 10% in 2025 — and median payment changes are near zero when extended amortizations are factored in [2]. The FCAC Mortgage Charter also provides protections, including temporary payment extensions and relief guidance for distressed borrowers [6][7].

The private mortgage surge is real, but it is concentrated in specific pockets: over-leveraged investors, self-employed borrowers with complex income, and those who accumulated debt during the low-rate era. For these groups, private lending is not a last resort — it is a strategic bridge back to bank qualification.

Self-employed Torontonians facing this challenge should also explore how self-employed borrowers can navigate the 2026 mortgage stress test and current private mortgage rates in Ontario to benchmark their options.

Conclusion: What Toronto Homeowners Should Do Right Now

Toronto’s 2026 renewal wave is exposing a structural gap between the mortgage market of 2021 and the lending reality of today. Tightening bank criteria — driven by OSFI rule changes, stress test requirements, and cautious appraisals — are pushing thousands of qualified, equity-rich homeowners toward private lending as their only viable renewal path.

Here are the actionable steps to take today:

- ✅ Start early — Begin your renewal review 4–6 months before your renewal date, not 30 days before

- ✅ Get a full mortgage review — A licensed broker can assess all three lending tiers and find the best fit

- ✅ Know your LTV — If your equity is strong, private lending may be faster and easier than you think

- ✅ Plan your exit strategy — Private mortgages work best as 1–2 year bridges back to A or B lenders

- ✅ Explore all income documentation options — Self-employed borrowers have more tools than ever in 2026

- ✅ Do not wait for the bank to say no — Proactive planning beats reactive scrambling every time

The good news: options exist at every lending tier. The key is knowing where you stand and acting before the June 2026 renewal peak arrives.

References

[1] Mortgage Renewal Wave Strains Some Regions Borrowers – https://www.cmhc-schl.gc.ca/observer/2026/mortgage-renewal-wave-strains-some-regions-borrowers

[2] Watch – https://www.youtube.com/watch?v=lSQJu2PTr7M

[3] Canada Mortgage Stress Test Updates What You Need To Know – https://www.gtarealstar.com/Canada-Mortgage-Stress-Test-Updates-What-You-Need-to-Know

[4] Ontario Homeowners Are Using Private Mortgages To Survive 2026 Heres Why Banks Arent The First Call Anymore 717 – https://www.lendworth.ca/blog/lendworth-blog-1/ontario-homeowners-are-using-private-mortgages-to-survive-2026-heres-why-banks-arent-the-first-call-anymore-717

[5] Osfis 2026 Mortgage Changes – https://optimumrealty.c21.ca/2025/11/07/osfis-2026-mortgage-changes

[6] Mortgage Relief Renewal Wave Waning – https://storeys.com/mortgage-relief-renewal-wave-waning/

[7] Renewing Your Mortgage In 2026 Heres What To Expect – https://www.ratehub.ca/blog/renewing-your-mortgage-in-2026-heres-what-to-expect/

[8] Why Toronto Homeowners Are Ditching Banks For Private Mortgages In 2026 Real Stories And Stats – https://everythingmortgages.ca/blog/why-toronto-homeowners-are-ditching-banks-for-private-mortgages-in-2026-real-stories-and-stats/

[9] Private Mortgages For Toronto Homeowners Battling 450 Delinquency Surge Survival Tactics In March 2026 – https://everythingmortgages.ca/blog/private-mortgages-for-toronto-homeowners-battling-450-delinquency-surge-survival-tactics-in-march-2026/

[10] Newmortgagerules – https://www.aaronsantos.net/blog/newmortgagerules