March 13, 2026

Private Mortgages Fueling Toronto’s 2026 Garden Suite Boom: Financing Legal Basement Rentals Amid Rent Recovery

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Toronto’s backyard has become the city’s hottest investment frontier. As housing affordability pressures mount and new zoning rules open the door for secondary suites on nearly every residential lot, savvy homeowners are racing to build garden suites and legalize basement rentals — and private mortgages are fueling Toronto’s 2026 garden suite boom like never before. With banks slow to adapt to non-traditional property types, private lenders are stepping in to bridge the gap, helping investors close fast, build smart, and refinance before the anticipated 2028 rent rebound fully materializes.

Key Takeaways 🏡

- Ontario Regulation 462/24 dramatically expanded garden suite eligibility, making ~80% of Toronto homes now suitable for secondary suites [1]

- Private mortgages now represent ~20% of Ontario’s mortgage market, up from 8–12% nationally five years ago, driven by speed and flexibility needs [10]

- The Federal Secondary Suite Loan Program doubled its maximum to $80,000 at 2% interest (January 2025), stacking well with private bridge financing [8]

- Private lenders close in 5–10 business days vs. 30–60 days for banks — a critical advantage in a competitive construction window [10]

- A step-by-step financing playbook combining private bridge loans, construction draws, and conventional refinancing can deliver strong ROI ahead of the rent recovery cycle

Why 2026 Is the Pivotal Year for Toronto Garden Suites

The regulatory stars have aligned. In November 2024, Ontario Regulation 462/24 fundamentally rewrote the rules for secondary suites. Garden suites now require only 4 metres of separation from the main house (down from 5–7.5 metres), angular plane restrictions were removed, and lot coverage allowances increased to 45% [1]. The result? Approximately 80% of Toronto’s residential properties now qualify for a garden suite or secondary suite addition.

Then came the City of Toronto’s “Made in Toronto” pre-approved garden and laneway suite plans, released in July 2025. These ready-to-use blueprints slash design costs and accelerate permit approvals — removing two of the biggest friction points that previously deterred homeowners from building.

On the federal side, the Canada Secondary Suite Loan Program doubled its maximum loan to $80,000 at just 2% interest over 15 years (effective January 2025), up from $40,000 [8][9]. Meanwhile, secondary suite refinancing rules expanded to allow homeowners to refinance up to 90% loan-to-value (previously 80%), with a $2 million property value ceiling and 30-year amortization available [4][1].

💡 Pull Quote: “The regulatory window is open. The question isn’t whether to build — it’s how to finance fast enough to capture the opportunity before the market catches up.”

Why the urgency? CMHC forecasts rental market softening through 2026 as new supply enters the market. But most analysts — including TD’s housing team — project a “modest, gradual recovery” that builds toward a stronger rebound by 2027–2028. Investors who complete construction and place tenants in 2026 position themselves to benefit from rising rents on a stabilized, cash-flowing asset.

For context on how Toronto’s evolving housing policies are reshaping buyer and investor strategies, the rental-to-ownership arbitrage analysis for 2026 GTA offers valuable perspective on the rent vs. buy calculus playing out right now.

How Private Mortgages Are Fueling Toronto’s 2026 Garden Suite Boom

Here’s the core problem: traditional banks struggle with garden suites and basement conversion projects. Lenders applying standard residential underwriting often can’t account for projected rental income from a suite that doesn’t yet exist. Appraisals on properties mid-renovation come in conservative. And the 30–60 day bank approval timeline can kill deals in a fast-moving construction market.

Private lenders solve all three problems.

The Private Lending Advantage in 2026

Private mortgages now represent approximately 20% of Ontario’s mortgage market, up from just 8–12% nationally five years ago [10]. This growth isn’t driven by desperate borrowers — it’s driven by smart investors who need speed and flexibility that banks simply can’t provide.

| Feature | Bank/A-Lender | Private Lender |

|---|---|---|

| Approval timeline | 30–60 business days | 5–10 business days |

| Income verification | Strict T4/NOA required | Flexible; asset-based |

| Rental income counted | Limited/none (pre-build) | Yes, projected income considered |

| Mid-renovation financing | Rarely available | Common |

| Typical rate range | Prime + 0.5–2% | 8–12% |

| Term length | 5 years standard | 6–12 months bridge |

Critically, 81% of private lenders are planning to increase originations in 2026, targeting roughly 10% volume growth over 2025 [10]. This means a well-capitalized, competitive private lending ecosystem — which translates to better rates and more flexible terms for borrowers.

New OSFI capital rules tightened in Q1 2026 further restrict how banks can double-count income across multiple mortgages, pushing portfolio investors squarely toward private lenders for expansion [10]. Understanding how private mortgages work in Ontario is now essential knowledge for any Toronto real estate investor.

EQ Bank also entered the space in October 2024, launching a specialized garden suite financing product designed specifically for laneway and garden suite projects — a sign that even alternative institutional lenders see the opportunity [6].

For a comprehensive overview of working with non-bank lenders, the full guide to getting a mortgage with a private lender is an excellent starting resource.

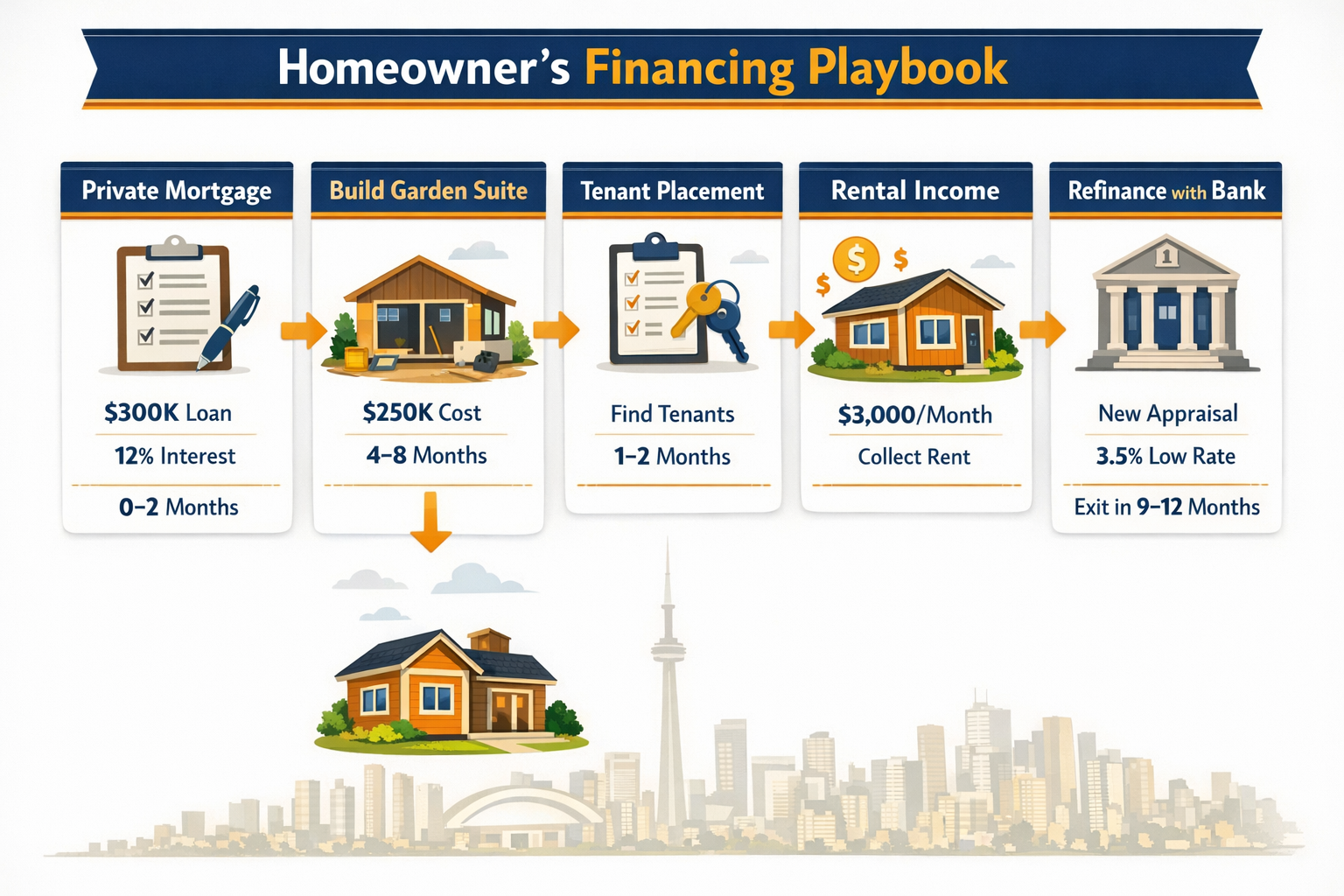

The Step-by-Step Garden Suite Financing Playbook

Here is a practical, stage-by-stage financing strategy that investors are using in 2026 to build garden suites and legal basement rentals efficiently.

Stage 1: Assess Existing Equity 🏠

Before approaching any lender, understand what equity is available. With secondary suite refinancing now allowing up to 90% LTV, many Toronto homeowners sitting on properties valued at $1M–$2M have significant accessible equity. Use a mortgage refinance calculator to model your numbers.

Example:

- Property value: $1,400,000

- Existing mortgage: $600,000

- Available equity at 90% LTV: $660,000

- Estimated garden suite build cost: $250,000–$400,000 [5]

Stage 2: Stack Government Programs First 💰

Before drawing on private capital, maximize low-cost government money:

- Canada Secondary Suite Loan Program: Up to $80,000 at 2% over 15 years [8]

- City of Toronto pre-approved plans: Reduce design/permit costs by $15,000–$30,000

- HST rebates on new construction (consult a tax professional)

Stage 3: Bridge with a Private Mortgage 🔑

This is where private mortgages fueling Toronto’s 2026 garden suite boom play their most important role. A private bridge loan covers:

- Construction costs not covered by government programs

- Carrying costs during the build (typically 4–8 months)

- Permit and soft costs if needed

Private lenders can fund within 5–10 business days [10], allowing construction to start immediately after permit approval rather than waiting months for bank approval. Understanding the difference between second mortgages vs. refinancing helps determine the right structure for each situation.

Stage 4: Legalize, Build, and Tenant-Place 🔨

During construction, focus on:

- Meeting all Toronto Building Code requirements for legal basement apartments [2]

- Using pre-approved “Made in Toronto” plans to accelerate inspections

- Securing a tenant before the refinancing conversation with a bank

A signed lease agreement transforms the property’s income profile entirely in a lender’s eyes.

Stage 5: Refinance into Conventional Product 🏦

Once the suite is complete, tenanted, and generating rental income, refinancing into a conventional mortgage (A or B lender) at significantly lower rates becomes achievable. The private bridge loan — typically held for just 6–12 months — is retired [10].

Working with a mortgage broker at this stage is highly recommended, as brokers can access multiple lenders simultaneously and structure the refinancing to maximize the rental income inclusion.

Projected ROI Snapshot 📊

| Scenario | Build Cost | Monthly Rent | Annual Gross Income | Cap Rate (Est.) |

|---|---|---|---|---|

| Garden Suite (600 sq ft) | $280,000 | $2,200 | $26,400 | ~9.4% |

| Legal Basement (800 sq ft) | $120,000 | $1,900 | $22,800 | ~19% |

| Both (combined) | $400,000 | $4,100 | $49,200 | ~12.3% |

Estimates based on 2026 Toronto rental market data and average construction costs [2][5]

For investors concerned about how 2026 mortgage rate forecasts affect their refinancing exit, the 2026 rate forecast analysis provides useful context for timing the conventional refinance.

Key Risks to Manage ⚠️

Even with strong fundamentals, investors should account for:

- Construction cost overruns: Budget a 15–20% contingency on all build estimates

- Permit delays: Even pre-approved plans can face queue backlogs at the City

- Private mortgage carrying costs: At 8–12% interest, delays extend costs quickly — timeline discipline is essential

- Toronto’s luxury land transfer tax increase (effective April 1, 2026) adds costs on properties over $3M, affecting higher-end acquisitions [1]

- Rental market softening in 2026: CMHC projects higher vacancy rates as supply increases — underwrite conservatively

Avoiding common mortgage application mistakes during both the private and conventional financing stages protects the entire investment thesis.

Conclusion: Build Now, Refinance Smart, Capture the Recovery

The convergence of permissive zoning, federal loan programs, expanded refinancing rules, and a well-capitalized private lending market has created a rare financing window in 2026. Private mortgages fueling Toronto’s 2026 garden suite boom are not a workaround — they are the strategic tool that makes the entire playbook work.

Actionable Next Steps ✅

- Assess your property’s eligibility under Ontario Regulation 462/24 — most Toronto homes now qualify

- Calculate available equity using the 90% LTV refinancing rules before approaching any lender

- Apply for the Canada Secondary Suite Loan Program ($80,000 at 2%) as your first capital layer

- Consult a mortgage broker to structure the private bridge loan and plan the refinancing exit

- Start construction in 2026 to place tenants and stabilize income ahead of the projected 2027–2028 rent recovery

The window is open. The financing tools exist. The investors who move in 2026 will be collecting rent when the recovery arrives.

References

[1] New Toronto Mortgage Rules – https://landsignal.ai/blog/new-toronto-mortgage-rules/ [2] Legal Basement Apartment Toronto Complete Guide To Permits Costs Roi 2025 – https://acebuildcontracting.ca/legal-basement-apartment-toronto-complete-guide-to-permits-costs-roi-2025/ [3] Guest Blog How Garden Suites Are Helping Homeowners In Collingwood – https://www.jaguarmortgages.ca/guest-blog-how-garden-suites-are-helping-homeowners-in-collingwood/ [4] Playing By New Rules What Changed For Toronto Real Estate In 2025 2026 – https://www.getwhatyouwant.ca/playing-by-new-rules-what-changed-for-toronto-real-estate-in-2025-2026 [5] Toronto Basement Apartments Garden Suites – https://alasya-construction.ca/toronto-basement-apartments-garden-suites/ [6] Financing For Laneway Homes Garden Suites – https://thecanadianinvestorpodcast.com/podcast/the-canadian-real-estate-investor/episode/financing-for-laneway-homes-garden-suites [7] Financing Options For Building A Toronto Laneway Suite Or Garden Suite – https://www.urbanlanes.com/resources/financing-options-for-building-a-toronto-laneway-suite-or-garden-suite/ [8] 2024 Fall Economic Statement Making It Easier For Homeowners To Build Secondary Suites – https://www.canada.ca/en/department-finance/news/2024/12/2024-fall-economic-statement-making-it-easier-for-homeowners-to-build-secondary-suites.html [9] How To Finance A Tiny Home – https://attimohomes.com/how-to-finance-a-tiny-home/ [10] Private Mortgages For Toronto Multi Family Investors Capitalizing On 2026 Rental Recovery Trends – https://everythingmortgages.ca/blog/private-mortgages-for-toronto-multi-family-investors-capitalizing-on-2026-rental-recovery-trends/