March 21, 2026

Private Mortgages Surge to 15.8% Market Share: Toronto’s Shift from Frozen HELOCs and Bank Denials

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

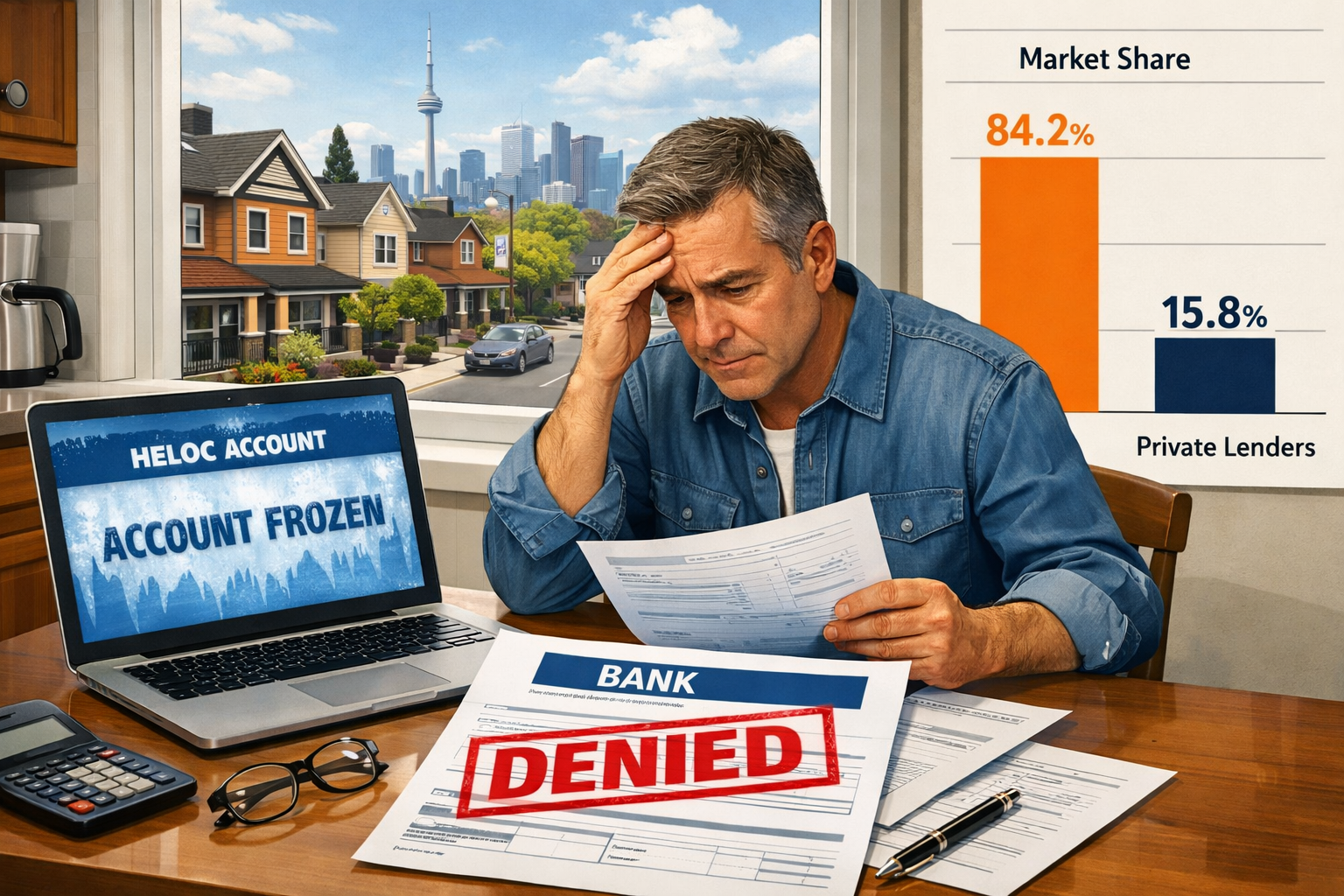

Something significant is happening in Toronto’s mortgage market — and most homeowners don’t see it coming until they’re already stuck. Private Mortgages Surge to 15.8% Market Share: Toronto’s Shift from Frozen HELOCs and Bank Denials is not just a headline. It reflects a real, data-backed shift in how Torontonians are financing their homes in 2026. According to the Financial Services Regulatory Authority of Ontario (FSRA), private mortgages now represent 15.8% of Ontario’s mortgage market by count — a level that signals deep structural cracks in how traditional banks serve everyday borrowers [8]. Bank HELOC freezes, low appraisals, and rigid renewal stress tests are pushing equity-rich homeowners toward private lenders at a pace the industry has never seen before.

Key Takeaways 📌

- Private mortgages hold 15.8% of Ontario’s mortgage market by count, driven by bank inflexibility and HELOC freezes [8]

- Toronto mortgage delinquencies surged 450% since Q3 2022, reaching 2,797 households by late 2025 [7]

- The Bank of Canada’s 2.25% policy rate is creating payment shock for 60% of renewing Ontario borrowers [1]

- Private lenders approve in 24–48 hours based on equity, not income — a critical advantage for self-employed and investors [1]

- Private mortgage rates average ~9%, making them a short-term bridge tool, not a permanent solution [1]

Why Banks Are Failing Toronto Borrowers in 2026

The HELOC Freeze Problem

One of the most disruptive trends of 2026 has been the quiet freezing of Home Equity Lines of Credit (HELOCs) by major Canadian banks. Lenders are citing property revaluations, OSFI risk pressure, and renewal shocks as justification — but for homeowners who planned to use their equity for renovations or debt consolidation, the impact is severe [1][5].

Banks are reducing or suspending HELOC limits even when homeowners have never missed a payment. The trigger is often a downward property appraisal or an internal risk review. For a deeper look at how HELOCs compare to other equity tools, see this guide on HELOC vs. Home Equity Loan.

💬 “Private mortgages are not a last resort — they are a workable option for borrowers whose assets outpace what banks are willing to acknowledge.” — Lendworth Capital [1]

New OSFI and CMHC Rules Are Making Things Worse

In Q1 2026, new OSFI capital rules tightened how banks count rental income across multiple properties. This hit real estate investors especially hard [3]. Meanwhile, CMHC overhauled its insurance rules in February 2026, raising premiums and restricting rental income recognition for newcomers — making conventional financing even harder to access [9].

The Bank of Canada held its policy rate at 2.25% on March 6, 2026, keeping prime at 4.45%. That sounds manageable — until you realize that 60% of renewing Ontario borrowers are facing payment shock, and Ontario absorbs 38% of Canada’s 438,000 national renewals [1]. The math is brutal for anyone who locked in at pandemic-era rates.

Who Is Being Pushed Out of the Bank System?

The borrowers most affected include:

| Borrower Type | Bank Challenge | Private Lender Advantage |

|---|---|---|

| Self-employed | Income hard to verify | Equity-based approval |

| Real estate investors | Rental income restrictions | Portfolio-level flexibility |

| Newcomers to Canada | Limited credit history | Asset-focused underwriting |

| Renewal-shock victims | Failed stress test | Bridge financing available |

| HELOC freeze victims | Equity locked out | Second mortgage access |

For self-employed borrowers navigating this landscape, qualifying for a mortgage without T4 slips has become a critical skill in 2026.

The Real Borrower Impact: Delinquencies, Denials, and the Private Pivot

Toronto’s Delinquency Crisis Is Fueling Private Demand

Toronto’s mortgage delinquency rate has surged 450% since Q3 2022, reaching 2,797 households by late 2025 — with Q2 2026 data showing continued deterioration [7]. These aren’t reckless borrowers. Many are equity-rich homeowners who simply cannot pass a renewal stress test at today’s rates.

When a homeowner has $400,000 in equity but can’t qualify for a bank renewal, the private mortgage market becomes the only viable bridge. Private lenders focus on loan-to-value (LTV) ratios rather than income documentation — approving files in 24 to 48 hours compared to the 2 to 4 weeks typical of bank processes [1].

This is where understanding how easy it is to get a private mortgage becomes essential for struggling homeowners.

B-Lenders vs. Private Lenders: What’s the Difference?

Many borrowers don’t realize there’s a middle ground between banks and private lenders. Here’s a quick breakdown:

- 🏦 Banks: Rates ~4%, strict income verification, 2–4 week approval

- 🏢 B-Lenders (Alt-A): Rates 5–6%, 1% fees, higher debt ratios but still income-dependent

- 🤝 Private Lenders: Rates ~9%, equity-based, 24–48 hour approval, short-term focus [1]

The rate gap is real — but so is the access gap. For borrowers facing bank denial, paying 9% for 12 months while restructuring finances is far better than losing a home to power of sale.

📊 Key Stat: Private lenders plan 10% origination growth in 2026, targeting competitive positioning amid strong capitalization [3].

For homeowners exploring equity-based solutions, second mortgages in Toronto offer another pathway worth understanding alongside private first mortgages.

The Role of Mortgage Brokers in Navigating Private Options

Mortgage brokers have become the critical link between distressed borrowers and private capital. Unlike banks, brokers can access dozens of private lenders simultaneously and match borrowers to the right equity-based product quickly.

The benefits of working with a mortgage broker are especially pronounced in 2026’s complex market. Brokers understand which private lenders specialize in which property types, and they can structure short-term private loans as bridges to eventual bank qualification.

Navigating the Private Mortgage Surge: What Borrowers Should Know

Private Mortgages Surge to 15.8% Market Share: What the FSRA Data Really Means

The FSRA’s finding that private mortgages represent 15.8% of Ontario’s mortgage market by count deserves careful interpretation [8]. This figure reflects mortgages originated, not the total outstanding balance — meaning private lending is even more active at the transaction level than balance-sheet numbers suggest.

Private lending dipped slightly from its pandemic-era peak, but the FSRA data confirms it remains vital for affordability-challenged borrowers [8]. The combination of rising delinquencies, HELOC freezes, and tighter bank rules ensures private demand stays elevated through 2026 and beyond.

Is a Private Mortgage Right for You? ✅

Consider a private mortgage if you:

- ✔️ Have been denied by a bank or B-lender at renewal

- ✔️ Have strong equity (typically 75–80% LTV or better)

- ✔️ Are self-employed with non-traditional income documentation

- ✔️ Need fast financing for a time-sensitive purchase or renovation

- ✔️ Are a newcomer investor affected by CMHC insurance restrictions [9]

- ✔️ Have a frozen HELOC and need bridge capital

Government Programs That Can Work Alongside Private Mortgages

The Federal Secondary Suite Loan Program offers $80,000 at 2% interest (doubled in January 2025), stackable with private bridge loans for renovation projects [3]. This combination can be powerful for homeowners adding legal basement suites or garden suites — a trend explored in detail in the guide on private mortgages fueling Toronto’s 2026 garden suite boom.

Key Risks to Understand Before Signing

Private mortgages are tools — not solutions. Key risks include:

- ⚠️ Higher rates (~9%) that compound quickly if the bridge period extends

- ⚠️ Lender fees of 1–3% that increase effective borrowing costs

- ⚠️ Short terms (typically 1 year) requiring a clear exit strategy

- ⚠️ Power of sale risk if the borrower cannot refinance at term end

A qualified mortgage broker can help structure the loan with a realistic exit plan — whether that’s qualifying for a bank mortgage after 12 months of improved credit, selling the property, or refinancing with a B-lender. For a full walkthrough of the process, the complete guide to getting a mortgage with a private lender is an essential starting point.

Conclusion: Private Mortgages Are a Bridge — Use Them Wisely

The data is clear. Private Mortgages Surge to 15.8% Market Share: Toronto’s Shift from Frozen HELOCs and Bank Denials is not a temporary blip — it reflects a structural realignment of how Torontonians access mortgage financing in 2026. Banks are tightening. HELOCs are being frozen. Renewal stress tests are failing equity-rich homeowners. And private lenders are filling the gap.

Actionable Next Steps 🎯

- Assess your equity position — know your current LTV before approaching any lender

- Consult a licensed mortgage broker who has access to private lender networks

- Build an exit strategy before signing any private mortgage — plan for 12 months

- Explore stacking options like the Federal Secondary Suite Loan Program for renovation needs

- Review your HELOC status proactively — don’t wait for a freeze notice

- Compare all tiers — bank, B-lender, and private — before committing

The private mortgage market exists to serve borrowers that the traditional system has left behind. Used strategically, with professional guidance and a clear timeline, it can be the bridge that saves a home, funds a renovation, or buys time to rebuild financial standing.

References

[1] Why Toronto Homeowners Are Ditching Banks For Private Mortgages In 2026 Real Stories And Stats – https://everythingmortgages.ca/blog/why-toronto-homeowners-are-ditching-banks-for-private-mortgages-in-2026-real-stories-and-stats/

[2] Watch – https://www.youtube.com/watch?v=GvF4XBzzJJs

[3] Private Mortgages Fueling Torontos 2026 Garden Suite Boom Financing Legal Basement Rentals Amid Rent Recovery – https://everythingmortgages.ca/blog/private-mortgages-fueling-torontos-2026-garden-suite-boom-financing-legal-basement-rentals-amid-rent-recovery/

[4] Housing Market Outlook – https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/market-reports/housing-market/housing-market-outlook

[5] Ontario Heloc Frozen Why Banks Are Quietly Cutting Off Access To Home Equity In 2026 – https://www.lendworth.ca/blog/lendworth-blog-1/ontario-heloc-frozen-why-banks-are-quietly-cutting-off-access-to-home-equity-in-2026-728

[6] Residential Mortgage Industry Report – https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/housing-research/research-reports/housing-finance/residential-mortgage-industry-report

[7] Private Mortgages For Torontos 450 Delinquency Surge Early Intervention Strategies In Q2 2026 – https://everythingmortgages.ca/blog/private-mortgages-for-torontos-450-delinquency-surge-early-intervention-strategies-in-q2-2026/

[8] Private Lending Declines Slightly Remains Significant Borrowers Facing Affordability Challenges – https://www.fsrao.ca/announcements/private-lending-declines-slightly-remains-significant-borrowers-facing-affordability-challenges

[9] Toronto Private Mortgages For Newcomer Investors Navigating 2026 Cmhc Restrictions And Equity Pathways – https://everythingmortgages.ca/blog/toronto-private-mortgages-for-newcomer-investors-navigating-2026-cmhc-restrictions-and-equity-pathways/

[10] After The Surge Understanding The GTA’s Housing Market Decline – https://www.airdberlis.com/insights/news/news-item/after-the-surge–understanding-the-gta-s-housing-market-decline