March 10, 2026

Should You Break Your Mortgage Early in 2026? Penalty vs Savings Analysis

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Last updated: March 10, 2026

Key Takeaways

- Breaking a mortgage early means paying a penalty, but falling Canadian interest rates in 2026 may make it worthwhile for many homeowners.

- The Bank of Canada’s policy rate dropped to 2.25% (as of January 2026), and the best 5-year fixed rates now sit around 3.89%, down from 6.49% peaks in 2022–2023. [1]

- Variable-rate mortgage penalties are typically 3 months’ interest ($3,550–$4,450 on a $400K balance), while Big 6 bank fixed-rate IRD penalties can reach $8,000–$25,000 on the same balance. [1]

- A simple break-even formula: divide your total penalty by your monthly savings. If the result (in months) is less than your remaining term, breaking early likely makes financial sense.

- A 1.5% rate drop on a $500K mortgage could save roughly $37,500 over five years, often exceeding the penalty cost. [1]

- Monoline lenders charge significantly lower penalties ($3,500–$5,000 on $400K) compared to the Big 6 banks, making early breaks more viable. [1]

- Approximately 60% of Canadian mortgages are set to renew in 2025–2026, making this analysis especially relevant right now. [1]

- Always request a formal mortgage payout statement before making any decision — the penalty amount can surprise you.

- Breaking early is generally not worth it if fewer than 12–18 months remain in your term, or if your rate drop is under 0.75%.

Quick Answer

Breaking your mortgage early in 2026 can save thousands of dollars if you’re locked into a rate from the 2022–2023 peak period and your remaining term is long enough to recover the penalty. The key question is whether your monthly interest savings, multiplied by the months left in your term, exceeds the penalty you’ll pay. For many Canadian homeowners with 24+ months remaining and a potential rate drop of 1.5% or more, the math often works in their favour.

What Does It Mean to Break Your Mortgage Early?

Breaking your mortgage early means ending your current mortgage contract before the term expires. When you do this, your lender charges a prepayment penalty as compensation for the interest income they lose.

This can happen for several reasons:

- Refinancing to access a lower interest rate

- Selling your home before the term ends

- Consolidating debt into your mortgage

- Switching lenders for better terms or features

The penalty amount depends on your mortgage type, your lender, how much time is left in your term, and the difference between your current rate and today’s posted rates. Understanding this penalty is the first step in any penalty vs savings analysis.

How Are Mortgage Prepayment Penalties Calculated in Canada?

The calculation method depends on whether your mortgage is fixed or variable rate. Variable-rate penalties are straightforward; fixed-rate penalties can be much larger and harder to predict.

Variable-Rate Mortgages

The penalty is almost always 3 months’ interest on your outstanding balance. On a $400,000 balance at a 4.45%–5% rate, that works out to roughly $3,550–$4,450. [1]

Fixed-Rate Mortgages

Fixed-rate mortgages use the Interest Rate Differential (IRD) — and this is where penalties can get painful. The formula is:

IRD Penalty = (Your Rate − Comparison Rate) × Balance × Remaining Years

For example, if you’re at 5.5% and the lender’s comparison rate is 3.89%, the difference is 1.61%. On a $400,000 balance with 3 years remaining:

- 1.61% × $400,000 × 3 = $19,320 penalty

Big 6 bank fixed-rate IRD penalties typically range from $8,000 to $25,000 on a $400K balance. Monoline lenders (like True North Mortgage or First National) generally charge $3,500–$5,000 on the same balance because they use a different comparison rate methodology. [1] [7]

Common mistake: Many homeowners assume the penalty will be small because their rate has dropped. In reality, banks use posted rates (not discounted rates) in their IRD calculation, which inflates the penalty significantly. Always request a formal payout statement from your lender before deciding anything. [2]

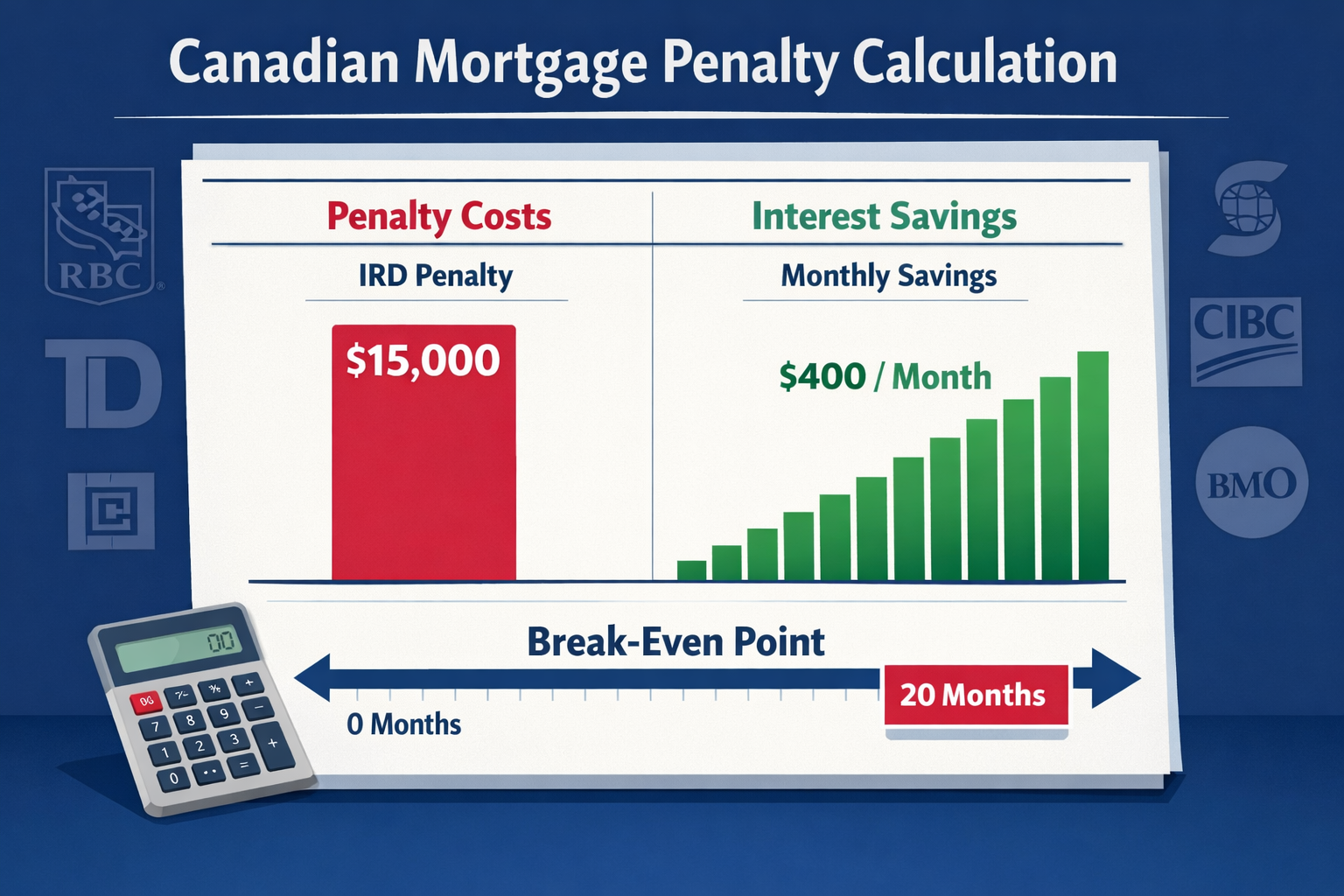

The Break-Even Formula: How to Run Your Own Penalty vs Savings Analysis

The break-even calculation is the core of any decision to break your mortgage early in 2026. It tells you exactly how many months it takes for your monthly savings to cover the penalty you pay upfront.

Break-Even Formula:

Break-Even (months) = Total Penalty ÷ Monthly Interest Savings

Example Calculation

| Item | Amount |

|---|---|

| Outstanding balance | $400,000 |

| Current rate | 5.5% |

| New rate available | 3.89% |

| Rate drop | 1.61% |

| Monthly interest savings | ~$537 |

| Fixed-rate IRD penalty (Big 6 bank) | $15,000 |

| Break-even period | ~28 months |

| Remaining term | 36 months |

| Net savings after break-even | ~$4,300 |

In this example, breaking early makes sense because the 28-month break-even is shorter than the 36 months remaining. [1]

Choose to break early if: Your break-even period is at least 6 months shorter than your remaining term, giving you a meaningful net benefit.

Don’t break early if: Your break-even period equals or exceeds your remaining term — you’d pay the penalty and never fully recover it.

For a deeper look at strategies to reduce your mortgage balance faster, see this guide on how to pay off your mortgage early.

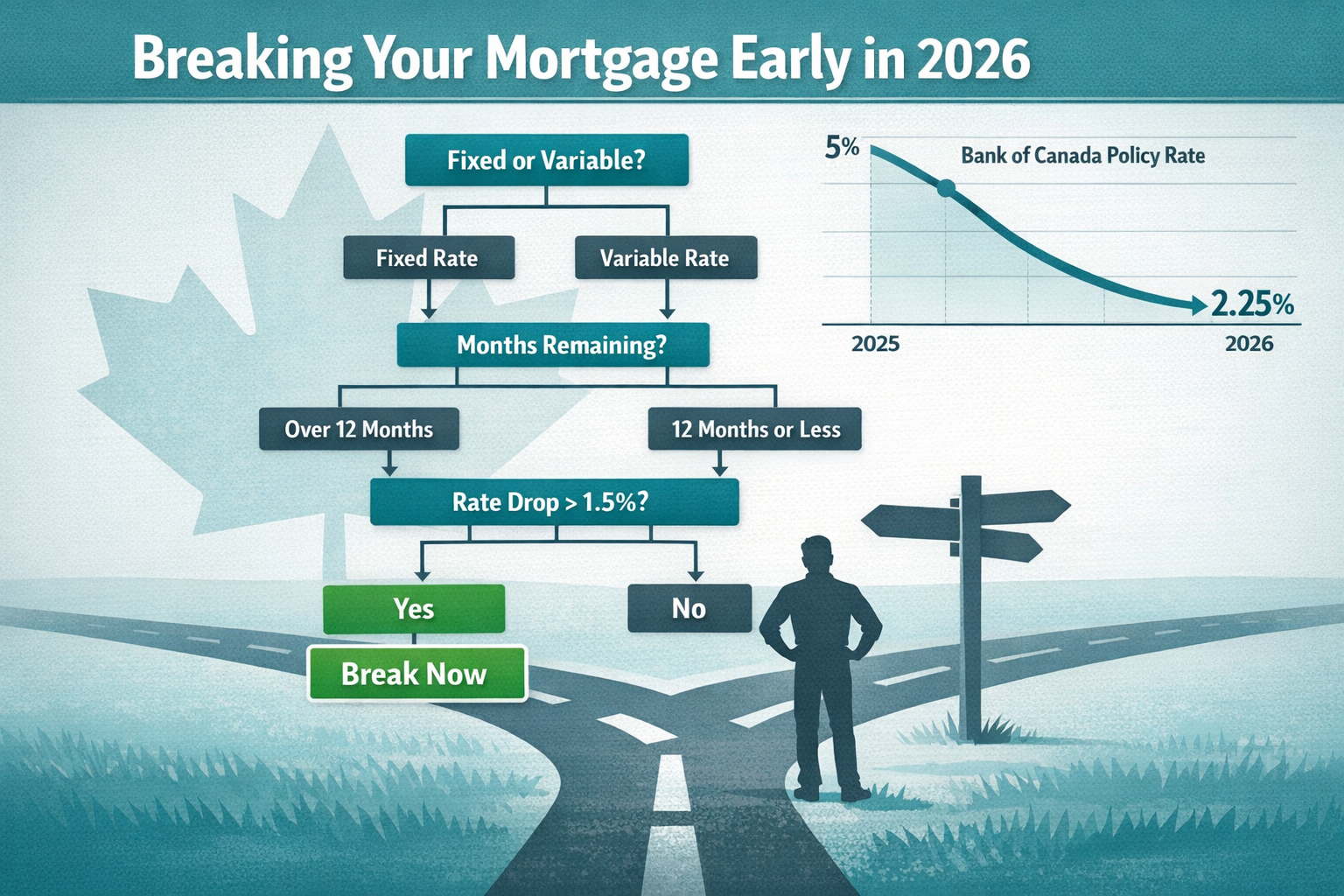

What Are Current Mortgage Rates in 2026, and Why Does the Rate Environment Matter?

Canada’s rate environment in 2026 is significantly more favourable than 2022–2023, which is exactly why so many homeowners are running a penalty vs savings analysis right now.

As of January 2026:

- Bank of Canada policy rate: 2.25% (down from a 5.0% peak) [1]

- Best 5-year fixed rate: approximately 3.89% [1]

- Best 5-year variable rate: approximately 3.55% [1]

Homeowners who locked in at 5.5%–6.49% during the 2022–2023 rate hike cycle are now sitting on a potential savings gap of 1.5–2.5 percentage points. On a $500,000 mortgage, a 1.5% rate reduction could save approximately $37,500 over five years — a figure that frequently exceeds the penalty cost. [1]

Meanwhile, approximately 60% of Canadian mortgages are scheduled to renew in 2025–2026, and the Bank of Canada estimates that fixed-rate holders from the low-rate era could face payment increases of 6–20% at renewal. [1] For many of those households, breaking early and locking in now — rather than waiting for a scheduled renewal — could reduce the payment shock.

The broader rate trend also matters. Markets anticipated a possible 0.25% Canadian Prime rate adjustment by end-2026 due to inflation remaining in the high-2% range and unemployment around 6.8%. [1] If rates tick back up, the window for locking in near 3.89% may narrow.

For context on how Bank of Canada decisions affect your mortgage, read The Impact of Bank of Canada’s Policy Decisions on Your Mortgage.

Who Should (and Shouldn’t) Consider Breaking Their Mortgage Early in 2026?

Breaking early makes the most sense for homeowners with significant rate gaps, long remaining terms, and lower-penalty lenders. It’s rarely worth it for those near the end of their term or with small rate differences.

Strong Candidates for Breaking Early ✅

- Locked in at 5.0%–6.49% during 2022–2023 and have 24+ months remaining

- Holding a variable-rate mortgage (lower penalty, easier math)

- Mortgage is with a monoline lender (lower IRD penalty)

- Planning to refinance for debt consolidation anyway

- Considering a debt consolidation mortgage to roll high-interest debt into a lower rate

Poor Candidates for Breaking Early ❌

- Fewer than 12–18 months remaining in the current term (just wait for renewal)

- Rate drop is under 0.75% (savings rarely cover Big 6 bank penalties)

- Mortgage is with a Big 6 bank and the IRD penalty is $20,000+

- Planning to sell the home within 12 months (penalty eats into sale proceeds)

- Recently renewed or refinanced (penalty resets the clock)

Edge case: If you’re breaking to consolidate high-interest debt (e.g., credit cards at 19.99%), the combined savings on both the mortgage rate and the consumer debt interest can dramatically shorten the break-even period — sometimes to under 12 months. In that scenario, even a larger penalty may be justified. See Mortgage Tips: How to Refinance Your Mortgage to Save Money for more on this approach.

Fixed vs. Variable: Which Mortgage Type Has the Lower Breaking Cost?

Variable-rate mortgages are almost always cheaper to break than fixed-rate mortgages. The 3-month interest penalty on a variable is predictable and relatively modest. Fixed-rate IRD penalties are larger and vary significantly by lender.

| Mortgage Type | Typical Penalty ($400K balance) | Predictability |

|---|---|---|

| Variable-rate | $3,550–$4,450 | High |

| Fixed (monoline lender) | $3,500–$5,000 | Medium |

| Fixed (Big 6 bank) | $8,000–$25,000 | Low |

The wide range for Big 6 bank fixed penalties comes from how each bank calculates its comparison (posted) rate. Some banks use a 3-year posted rate as the comparison even if you have 4 years left — this inflates the IRD and your penalty. [1] [7]

Decision rule: If you have a fixed-rate mortgage with a Big 6 bank and your penalty quote is above $15,000, the rate drop needs to be substantial (1.5%+) and your remaining term needs to be 30+ months for the numbers to work.

For guidance on fixed vs. variable rate choices going forward, see the Mortgage Rate Guide: Fixed or Variable Mortgage Options.

What Are the Alternatives to Breaking Your Mortgage Early?

Breaking your mortgage isn’t the only way to reduce your interest costs. Several alternatives carry no penalty and can still improve your financial position.

1. Prepayment Privileges

Most Canadian mortgages allow annual lump-sum prepayments of 10–20% of the original balance, penalty-free. Using this option reduces your principal and cuts the total interest you pay. [2]

2. Accelerated Biweekly Payments

Switching from monthly to accelerated biweekly payments effectively makes one extra monthly payment per year, shaving years off your amortization. Read more about the power of biweekly mortgage payments.

3. Blend-and-Extend

Some lenders offer a “blend-and-extend” option, where your current rate and the new lower rate are blended together, and your term is extended. There’s no penalty, but you won’t get the full benefit of today’s lowest rates.

4. Wait for Scheduled Renewal

If fewer than 12 months remain, waiting is almost always better. The penalty savings outweigh the rate benefit at that stage.

5. Second Mortgage or HELOC

If the goal is to access equity or consolidate debt, a second mortgage or home equity line of credit may achieve the objective without triggering a first-mortgage penalty.

Step-by-Step: How to Decide Whether to Break Your Mortgage Early in 2026

Here’s a practical checklist to work through before making any decision:

- Request a payout statement from your lender. This gives you the exact penalty amount — don’t estimate.

- Get a rate quote for a new mortgage at today’s best available rate (ideally from a mortgage broker who can shop multiple lenders).

- Calculate your monthly savings: (Current rate − New rate) × Balance ÷ 12.

- Calculate break-even: Penalty ÷ Monthly savings = Break-even months.

- Compare to remaining term: If break-even months < remaining term months, the math supports breaking.

- Factor in other costs: Legal fees for refinancing ($800–$1,500), appraisal fees ($300–$500), and any discharge fees.

- Consider your plans: Are you selling, moving, or changing income in the next 2 years? That changes everything.

- Speak with a mortgage broker to confirm the analysis and explore lender options. A broker can often find a lender with lower penalties or better blended rates.

Working with a mortgage broker adds value here because they can access rates and lender terms that aren’t always available directly. Learn more about what a mortgage broker does and how they help.

Conclusion: Should You Break Your Mortgage Early in 2026?

The penalty vs savings analysis for breaking your mortgage early in 2026 comes down to three numbers: your penalty, your monthly savings, and your remaining term. For homeowners who locked in at 2022–2023 peak rates and still have 24 or more months left, the math frequently supports breaking early — especially with 5-year fixed rates now near 3.89% and variable rates around 3.55%.

That said, this is not a one-size-fits-all decision. Big 6 bank IRD penalties can be steep enough to erase the benefit, while monoline lender penalties often make the calculation much more favourable. Variable-rate holders face the lowest barriers and should run the numbers first.

Actionable next steps:

- Call your lender today and request a formal payout statement with the exact penalty amount.

- Contact a mortgage broker to get current rate quotes and a personalized break-even analysis.

- Run the break-even formula (penalty ÷ monthly savings) and compare it to your remaining term.

- Consider the alternatives — prepayment privileges, biweekly payments, or blend-and-extend — if the penalty is too high.

- Act before rates shift. The current rate environment is favourable, but market forecasts suggest potential movement by late 2026. [1]

For more strategies on reducing your mortgage costs without necessarily breaking your contract, explore saving tips to become mortgage free.

Frequently Asked Questions

Q: What is the average penalty for breaking a mortgage early in Canada in 2026?

Variable-rate penalties average $3,550–$4,450 on a $400,000 balance (3 months’ interest). Fixed-rate IRD penalties at Big 6 banks range from $8,000 to $25,000 on the same balance. Monoline lenders typically charge $3,500–$5,000. [1]

Q: Is it worth breaking a fixed mortgage to get a lower rate?

It depends on your remaining term and penalty amount. If the break-even period (penalty ÷ monthly savings) is shorter than your remaining term by at least 6 months, it’s generally worth it. A 1.5%+ rate drop with 30+ months remaining often passes this test. [1]

Q: Can I break my mortgage without paying a penalty?

Some lenders allow penalty-free breaks at renewal, or if you use their blend-and-extend option. Prepayment privileges (10–20% lump sum annually) also reduce your balance without penalty. A full early break almost always triggers a fee. [2]

Q: How do I calculate the IRD penalty on my mortgage?

The IRD = (Your Rate − Comparison Rate) × Outstanding Balance × Remaining Years. The comparison rate varies by lender and is often a posted rate, not a discounted rate. Always get the exact figure from your lender in writing. [1] [7]

Q: What’s the difference between breaking a mortgage and refinancing?

Breaking a mortgage means ending the current contract early (and paying a penalty). Refinancing typically involves breaking the existing mortgage and replacing it with a new one, often at a lower rate. The terms are often used interchangeably, but refinancing implies a new loan structure. [2]

Q: Should I break my variable-rate mortgage in 2026?

Variable-rate mortgages carry lower penalties (3 months’ interest), so the break-even calculation is more forgiving. If you can lock into a fixed rate that’s meaningfully lower and you have 18+ months remaining, it’s worth running the numbers. [1]

Q: What happens to my mortgage penalty if I sell my home?

If you sell your home and pay off the mortgage before the term ends, the prepayment penalty still applies. It’s deducted from your sale proceeds at closing. Factor this into your net sale calculation when pricing your home.

Q: Does breaking your mortgage affect your credit score?

No. Paying out a mortgage early — even with a penalty — does not negatively affect your credit score. In fact, if you refinance into a new mortgage, your credit profile may improve over time with on-time payments.

Q: How long does it take to break a mortgage and get a new one?

The process typically takes 30–60 days from application to closing for a refinance. Your lender will require a new appraisal, income verification, and legal work. A mortgage broker can often accelerate this timeline.

Q: Is now a good time to break my mortgage given 2026 rate forecasts?

Current rates are near their lowest since 2022. Markets anticipate potential rate movement by late 2026. [1] If your break-even analysis is favourable, acting sooner rather than later reduces the risk of missing the current rate window.

References

[1] Breaking Mortgage Early Canada Worth It – https://www.neobanc.com/articles/breaking-mortgage-early-canada-worth-it

[2] Break Mortgage Contract – https://www.canada.ca/en/financial-consumer-agency/services/mortgages/break-mortgage-contract.html

[4] Tembo Market Watch January 2026 – https://www.tembomoney.com/learn/tembo-market-watch-january-2026

[7] How Much Will It Cost To Break Your Mortgage – https://www.truenorthmortgage.ca/blog/how-much-will-it-cost-to-break-your-mortgage

[9] Mortgage Rates Broker Forecast Fix – https://www.moneysavingexpert.com/news/2026/01/mortgage-rates-broker-forecast-fix/

Tags: breaking mortgage early, mortgage prepayment penalty, IRD penalty Canada, mortgage refinancing 2026, Canadian mortgage rates, penalty vs savings analysis, fixed vs variable mortgage, Bank of Canada rate, mortgage break-even calculation, early mortgage payout, mortgage refinance Canada, mortgage renewal 2026