February 5, 2026

How Self-Employed Borrowers in Toronto Can Qualify for Mortgages Without T4 Slips in 2026

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

Securing a mortgage as a self-employed professional in Toronto can feel like navigating a maze blindfolded. While traditional employees simply hand over their T4 slips and watch approvals roll in, entrepreneurs, freelancers, and business owners face a completely different reality. The good news? How Self-Employed Borrowers in Toronto Can Qualify for Mortgages Without T4 Slips in 2026 is not only possible—it’s becoming increasingly common as lenders adapt to Canada’s growing gig economy.

The challenge lies in proving income when tax strategies designed to minimize liability clash with mortgage requirements that demand maximum reported earnings. This comprehensive guide reveals the exact documentation alternatives, lender requirements, and strategic approaches that self-employed Torontonians need to successfully qualify for mortgages in 2026—without a single T4 slip in sight.

Key Takeaways

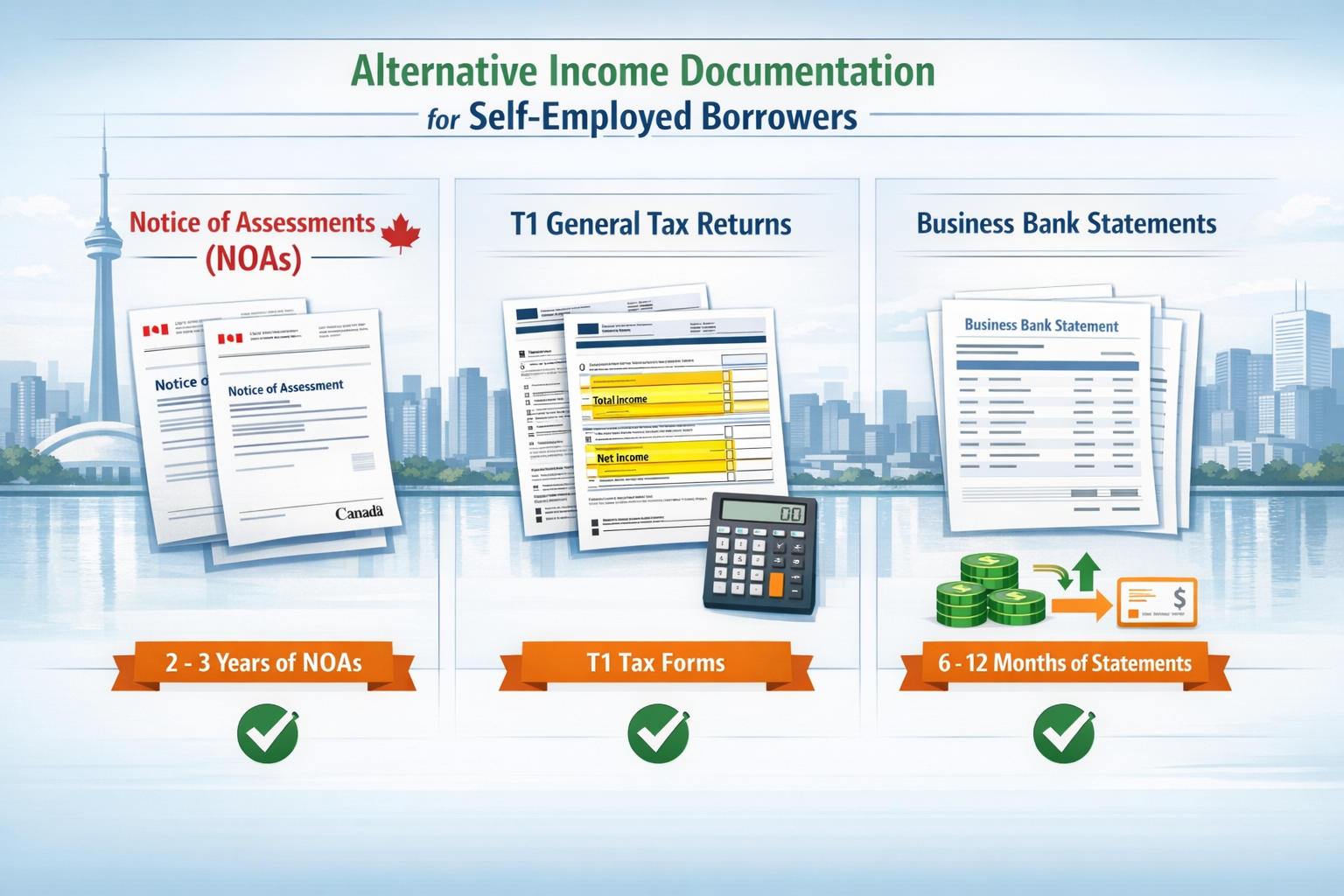

✅ Self-employed borrowers must provide 2-3 years of Notices of Assessment (NOAs) paired with T1 General forms as the primary alternative to T4 slips for traditional mortgage qualification[1][2].

✅ Stated-income mortgage products accept 6-12 months of business bank statements instead of tax documents, though they typically carry interest rates 2-4% higher than prime lending[3][6].

✅ The mandatory stress test requires qualification at 5.25% or contract rate plus 2%, significantly impacting affordability for Toronto’s high property values in 2026[2].

✅ Tax deductions create a borrowing paradox—while lowering taxable income saves money on taxes, it simultaneously reduces mortgage qualification amounts since lenders only use reported income[2].

✅ Down payment requirements range from 5-20% depending on property value and documentation strength, with conventional mortgages (20%+ down) offering more flexibility for self-employed applicants[1][4].

Understanding the Self-Employed Mortgage Landscape in Toronto for 2026

The Toronto real estate market presents unique challenges for self-employed borrowers in 2026. With average home prices consistently exceeding $1 million in many neighborhoods, proving sufficient income becomes critical. Traditional lenders have historically viewed self-employed applicants as higher-risk borrowers, but the landscape has evolved significantly.

Why T4 Slips Don’t Work for Self-Employed Professionals

T4 slips represent employment income paid by an employer—a document that simply doesn’t exist for business owners, independent contractors, and freelancers. Instead of receiving a predictable salary with automatic tax deductions, self-employed individuals report business income through different channels entirely.

The fundamental difference:

- Traditional employees: Receive T4s showing gross employment income

- Self-employed individuals: Report business income on T1 General tax returns after deducting legitimate business expenses

This distinction creates the core challenge. When a self-employed Toronto resident writes off home office expenses, vehicle costs, equipment purchases, and other business deductions, their taxable income decreases—which is excellent for tax purposes but problematic for mortgage qualification[2].

The Growing Self-Employed Sector in Canada

Canada’s self-employed workforce continues to expand, with over 2.9 million Canadians working for themselves as of 2026. This shift has prompted lenders to develop specialized mortgage products and documentation requirements specifically designed for non-traditional income verification. Understanding 5 things you need to know about self-employed mortgages can help borrowers navigate this evolving landscape.

Primary Documentation: How Self-Employed Borrowers in Toronto Can Qualify for Mortgages Without T4 Slips in 2026 Using Tax Returns

The gold standard for self-employed mortgage qualification remains tax-based income verification. This approach satisfies traditional lenders’ requirements while avoiding the premium interest rates associated with alternative documentation methods.

Notice of Assessment (NOA) Requirements

The Notice of Assessment serves as the cornerstone document for self-employed mortgage applications. Issued by the Canada Revenue Agency (CRA) after processing your tax return, the NOA confirms:

- Your reported income for the tax year

- Tax amounts paid or owed

- RRSP contribution room

- Government benefit eligibility

Lender requirements for NOAs:

- Minimum timeframe: 2-3 consecutive years of NOAs[1][2]

- Income calculation: Lenders average the reported income across multiple years

- Consistency requirement: Income should demonstrate stability or growth patterns

- Recent filing: Most lenders require the most recent tax year to be filed and assessed

💡 Pro Tip: If your income has increased significantly in recent years, some lenders will weight the most recent year more heavily in their calculations, potentially increasing your borrowing power.

T1 General Tax Forms: The Complete Picture

While NOAs confirm what you filed, T1 General forms provide the detailed breakdown lenders need to assess your financial situation comprehensively. These multi-page documents include:

- Line 15000: Total income before deductions

- Line 23600: Net income (after deductions)

- Line 26000: Taxable income

- Schedule C: Interest and investment income

- Business income sections: Detailed revenue and expense reporting

Lenders typically focus on Line 15000 (total income) but may add back certain business deductions that don’t represent actual cash outflows, such as:

- Capital Cost Allowance (CCA) depreciation

- Non-cash expenses

- One-time write-offs

This “add-back” approach can significantly improve your qualifying income without requiring higher tax payments[2].

Income Averaging and Stability Demonstration

Traditional lenders calculate qualifying income by averaging your reported earnings over 2-3 years. Here’s how it works in practice:

Example calculation:

- Year 1 (2023): $85,000 net business income

- Year 2 (2024): $92,000 net business income

- Year 3 (2025): $98,000 net business income

- Average qualifying income: $91,667

However, if income shows significant fluctuation or decline, lenders may:

- Use the lowest year as the qualifying amount

- Require additional documentation explaining variations

- Request business financial statements for context

- Decline the application if instability appears excessive

For borrowers with less than 1 year’s accounts, alternative approaches become necessary.

Tax Compliance: A Non-Negotiable Requirement

Beyond simply filing returns, lenders in 2026 demand complete tax compliance as a prerequisite for mortgage approval. This includes:

✔️ All personal and business taxes fully paid—no outstanding balances with CRA[1][2][3]

✔️ HST/GST remittances current—if your business exceeds $30,000 in quarterly revenue, HST/GST registration and payment compliance is mandatory[1]

✔️ No tax liens or garnishments—these automatically disqualify applicants from traditional lending

✔️ Authorized CRA release forms—lenders typically require signed authorization to verify your tax status directly with CRA

Important: Even payment plans with CRA can complicate mortgage approval. Lenders prefer to see tax obligations completely satisfied before advancing mortgage funds.

Alternative Documentation: Stated-Income Mortgages and Bank Statement Programs

For self-employed Toronto borrowers who cannot or prefer not to use tax returns for qualification, stated-income mortgage programs offer a viable alternative path—though with distinct trade-offs.

Business Bank Statement Verification Programs

Stated-income mortgages replace tax documentation with direct evidence of business cash flow through bank statements. This approach benefits borrowers who:

- Legitimately write off substantial business expenses, reducing taxable income

- Have recently become self-employed (less than 2 years)

- Experience seasonal income fluctuations that don’t average well

- Prefer privacy regarding detailed tax information

Bank statement requirements:

- Duration: 6-12 consecutive months of business account statements[3][6]

- Activity level: Consistent deposits demonstrating active business operations

- Account type: Business bank accounts (personal accounts typically insufficient)

- Verification: Lenders analyze deposit patterns, transaction frequency, and cash flow consistency

How Lenders Calculate Income from Bank Statements

Rather than using reported tax income, lenders employing bank statement programs apply formulas to estimate qualifying income:

Common calculation methods:

- Gross deposit method: Total all deposits, multiply by 50-70% to account for business expenses

- Average monthly method: Calculate average monthly deposits, annualize, apply expense factor

- Net cash flow method: Analyze deposits minus withdrawals to determine actual business profit

Example:

- Monthly average deposits: $15,000

- Annualized: $180,000

- Expense factor (60%): $180,000 × 0.60 = $108,000 qualifying income

This approach often yields higher qualifying income than tax-based methods for borrowers who maximize deductions[6].

Interest Rate Premiums and Trade-Offs

The convenience of stated-income mortgages comes with measurable costs:

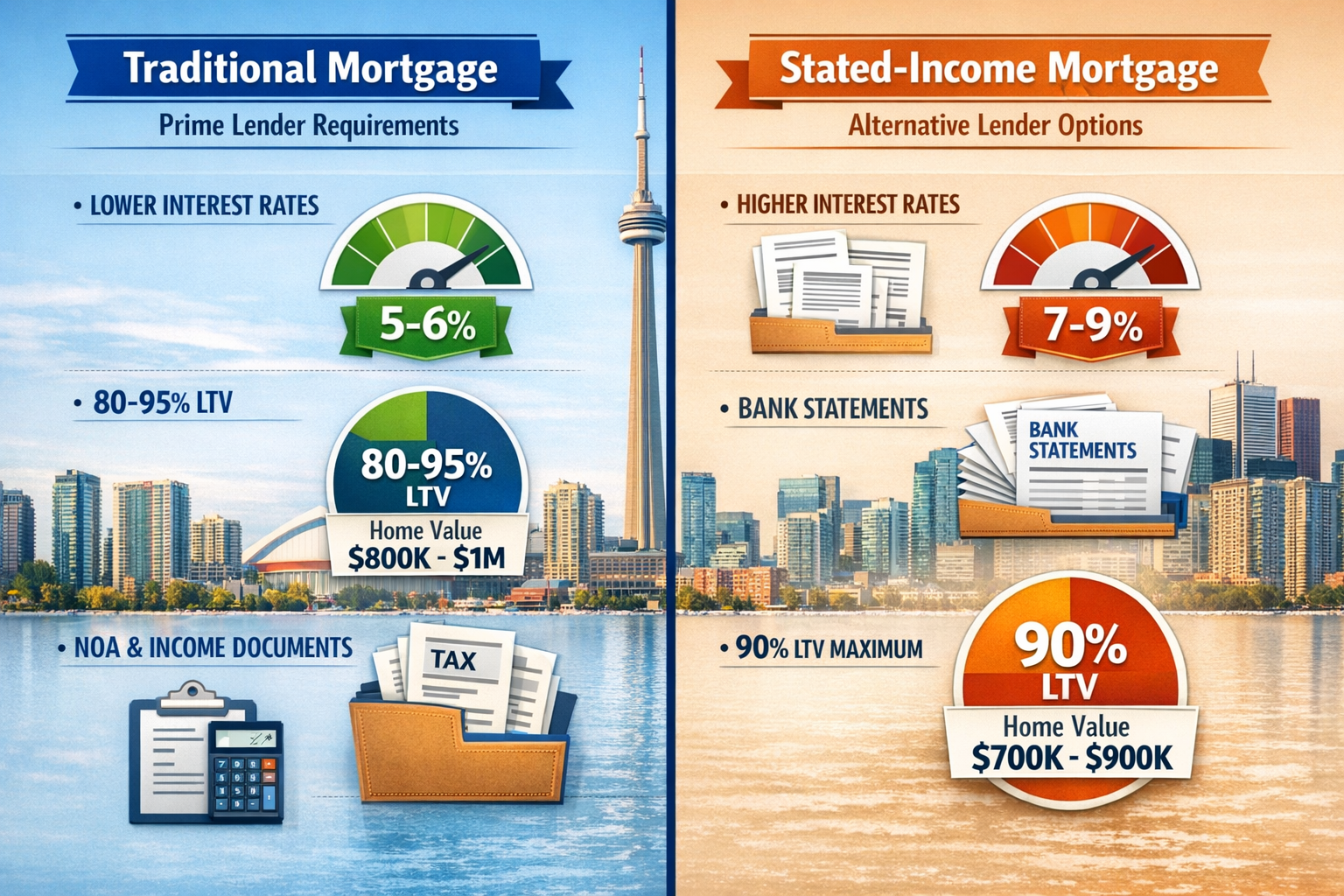

| Mortgage Type | Typical Interest Rate (2026) | Documentation Required | Maximum LTV |

|---|---|---|---|

| Prime/Traditional | 5.0% – 6.0% | NOAs, T1 Generals (2-3 years) | 95% (insured) / 80% (conventional) |

| Stated-Income | 7.0% – 9.0% | Bank statements (6-12 months) | 90% (insured) / 80% (conventional) |

| Private Lending | 8.0% – 12.0% | Minimal documentation | 75% – 80% |

Cost impact example:

- Mortgage amount: $600,000

- Prime rate (5.5%): Monthly payment $3,406

- Stated-income rate (8.0%): Monthly payment $4,401

- Monthly difference: $995

- Annual cost increase: $11,940

For many Toronto borrowers, the higher carrying costs make stated-income products a short-term solution—used to secure the property, then refinanced to traditional lending once sufficient tax history accumulates. Learning how to get approved for a mortgage using your business income can help optimize this strategy.

Alternative Lender Options in Toronto

Several lender categories serve self-employed borrowers with varying documentation requirements:

🏦 Traditional Banks (A-Lenders):

- Strictest documentation requirements

- Best interest rates

- Require full tax compliance and 2-3 year history

- Examples: RBC, TD, Scotiabank, BMO

🏢 Alternative Lenders (B-Lenders):

- More flexible documentation standards

- Moderate interest rate premiums (1-3% above prime)

- Accept stated-income with strong credit

- Examples: Equitable Bank, Home Trust, MCAP

🏘️ Private Lenders:

- Minimal documentation requirements

- Highest interest rates (8-12%+)

- Focus on property equity rather than income

- Typically short-term solutions (6-24 months)

For borrowers exploring this route, understanding how to get a mortgage with a private lender in Toronto provides valuable context.

Navigating the 2026 Stress Test and Qualification Requirements

Understanding How Self-Employed Borrowers in Toronto Can Qualify for Mortgages Without T4 Slips in 2026 requires mastering the stress test and debt service ratio calculations that determine maximum borrowing capacity.

The Mandatory Mortgage Stress Test Explained

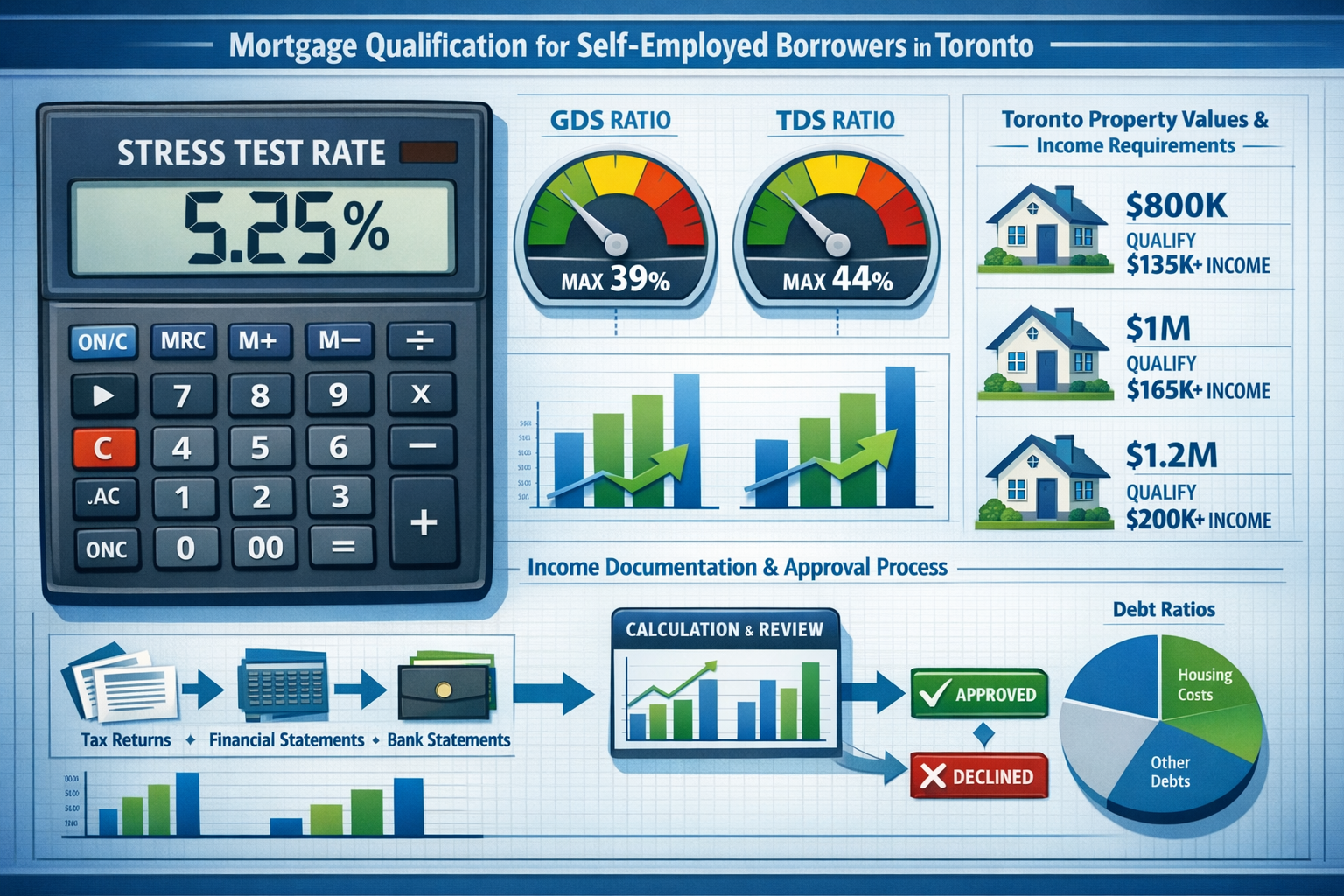

Implemented by the Office of the Superintendent of Financial Institutions (OSFI), the mortgage stress test ensures borrowers can afford payments even if interest rates increase. In 2026, all mortgage applicants must qualify at the higher of:

- 5.25% (the benchmark qualifying rate), OR

- Your contract rate plus 2%[2]

Practical example:

- Actual mortgage rate offered: 5.5%

- Stress test qualifying rate: 7.5% (5.5% + 2%)

- You must prove you can afford payments at 7.5%, even though you’ll actually pay 5.5%

This requirement significantly reduces maximum borrowing amounts, particularly impactful for Toronto’s high property values.

Debt Service Ratio Calculations

Lenders use two key ratios to assess affordability:

📊 Gross Debt Service (GDS) Ratio: Maximum 39% of gross income[4]

Formula: (Mortgage payment + Property taxes + Heating + 50% of condo fees) ÷ Gross monthly income

📊 Total Debt Service (TDS) Ratio: Maximum 44% of gross income[4]

Formula: (GDS expenses + All other debt payments) ÷ Gross monthly income

Example calculation for self-employed Toronto borrower:

- Qualifying income: $100,000 annually ($8,333 monthly)

- Maximum GDS (39%): $3,250

- Maximum TDS (44%): $3,667

Proposed housing costs:

- Mortgage payment (at stress test rate): $2,800

- Property taxes: $350

- Heating: $100

- Total GDS: $3,250 (exactly 39% ✓)

Other debts:

- Car payment: $400

- Credit card minimum: $150

- Total TDS: $3,700 (44.4% ✗ EXCEEDS LIMIT)

In this scenario, the borrower would need to either:

- Reduce the mortgage amount

- Pay off other debts before applying

- Increase qualifying income

How the Stress Test Impacts Self-Employed Borrowers

The stress test creates disproportionate challenges for self-employed applicants because:

- Lower reported income: Tax optimization strategies reduce qualifying income

- Income averaging: Multi-year averaging may not reflect current earning capacity

- Variable income: Fluctuations trigger conservative lender assessments

- Higher Toronto prices: Expensive properties require substantial qualifying income

Affordability comparison:

| Annual Income | Max Mortgage (No Stress Test) | Max Mortgage (With Stress Test) | Reduction |

|---|---|---|---|

| $80,000 | $440,000 | $340,000 | -23% |

| $100,000 | $550,000 | $425,000 | -23% |

| $150,000 | $825,000 | $640,000 | -22% |

Assumptions: 5.5% contract rate, 7.5% stress test rate, 25-year amortization, 39% GDS, no other debts

Understanding these calculations helps self-employed borrowers set realistic expectations and plan documentation strategies accordingly. Those facing stricter lending standards and higher scrutiny can benefit from professional mortgage broker guidance.

Down Payment Requirements and LTV Ratios

Down payment amounts directly impact qualification difficulty and product availability for self-employed Toronto borrowers in 2026:

📍 5% – 19.99% Down Payment (Insured Mortgages):

- Requires mortgage default insurance (CMHC, Sagen, Canada Guaranty)

- Property value maximum: $1,000,000[1][4]

- Stricter income documentation requirements

- Insurance premiums add 2.8% – 4.0% to mortgage amount

- Best suited for borrowers with strong tax-reported income

📍 20% – 34.99% Down Payment (Conventional Mortgages):

- No mortgage insurance required

- Maximum loan-to-value (LTV): 80%[1]

- More flexibility for alternative documentation

- Lower qualification barriers for self-employed

- No property value ceiling

📍 35%+ Down Payment:

- Significantly easier qualification

- Some lenders reduce documentation requirements

- Access to best interest rates

- Demonstrates financial stability

Strategic consideration: Self-employed borrowers with marginal qualification often benefit from increasing down payments to 20%+ to access conventional mortgage flexibility and avoid insurance premiums that increase carrying costs.

Business Documentation Requirements: Proving Legitimacy and Longevity

Beyond income verification, lenders require comprehensive business documentation to confirm your self-employment is legitimate, established, and likely to continue.

Essential Business Registration Documents

📄 Articles of Incorporation (for incorporated businesses):

- Proves legal business structure

- Confirms business name and registration date

- Demonstrates professional business setup

- Required for corporations claiming business income[1]

📄 Business Number and GST/HST Registration:

- Business Number (BN): 9-digit identifier issued by CRA

- GST/HST Account Number: Required if quarterly revenue exceeds $30,000[1]

- Proves tax compliance and legitimate business operations

- Lenders verify registration directly with CRA

📄 Business License (if applicable):

- Required for certain professions and industries

- Municipal business licenses for Toronto operations

- Professional designations (CPA, lawyer, engineer, etc.)

- Trade certifications for contractors and skilled trades

Proof of Business Continuity

Lenders assess whether your self-employment represents stable, ongoing income or temporary contract work:

✅ Strong continuity indicators:

- 2+ years of continuous self-employment

- Established client base with recurring contracts

- Business growth trajectory in revenue

- Professional website and business infrastructure

- Multiple income streams within the business

- Industry credentials and certifications

⚠️ Weak continuity indicators:

- Recently transitioned from employment to self-employment

- Single client providing all revenue (appears like disguised employment)

- Declining revenue trends

- Seasonal business without off-season income sources

- No business infrastructure or professional presence

For professionals like IT consultants seeking self-employed mortgages, demonstrating contract continuity and recurring client relationships strengthens applications significantly.

Industry-Specific Documentation

Certain professions require additional verification:

🏗️ Contractors and Trades:

- WSIB clearance certificates

- Liability insurance documentation

- Municipal permits for completed projects

- Contracts for upcoming work

👨⚕️ Healthcare Professionals:

- Professional college registration

- Clinic ownership or partnership agreements

- Billing number registration

- Malpractice insurance

💼 Consultants and Professionals:

- Client contracts or letters of engagement

- Professional liability insurance

- Industry certifications or designations

- Portfolio of completed projects

🎨 Creative Professionals:

- Portfolio of work

- Client testimonials or contracts

- Invoicing history

- Royalty or licensing agreements

Strategic Tax Planning: Balancing Deductions with Mortgage Qualification

The central paradox facing self-employed Toronto borrowers involves tax efficiency versus mortgage qualification—a challenge requiring careful planning and timing.

The Tax Deduction Dilemma

Every dollar claimed as a business expense reduces taxable income, which:

✅ Tax benefits:

- Lower income tax payable

- Reduced CPP contributions

- Potential HST/GST refunds

- Increased after-tax cash flow

❌ Mortgage qualification drawbacks:

- Lower qualifying income for lenders

- Reduced maximum borrowing capacity

- Potential disqualification from prime lending

- Forced reliance on higher-rate products[2]

Example impact:

| Scenario | Gross Revenue | Business Deductions | Net Taxable Income | Approximate Max Mortgage |

|---|---|---|---|---|

| Maximum Deductions | $150,000 | $70,000 | $80,000 | $340,000 |

| Moderate Deductions | $150,000 | $40,000 | $110,000 | $470,000 |

| Minimal Deductions | $150,000 | $20,000 | $130,000 | $555,000 |

Assumes stress test qualification, 39% GDS, no other debts

The difference between aggressive and conservative tax strategies can mean $215,000 in additional borrowing capacity—often the difference between qualifying for a Toronto property or not.

Strategic Planning Timeline

For self-employed individuals planning to purchase within 2-3 years:

📅 Year 1 (2-3 years before purchase):

- Consult with both accountant and mortgage professional

- Understand income requirements for target property price

- Begin moderating business deductions if necessary

- Maximize add-back opportunities (CCA, non-cash expenses)

📅 Year 2 (1-2 years before purchase):

- Report income levels that support mortgage goals

- Maintain consistent or growing income trajectory

- Ensure complete tax compliance

- Build credit score above 680 for optimal rates

📅 Year 3 (Purchase year):

- File taxes early to obtain NOA before shopping

- Gather all business documentation

- Pre-qualify with multiple lender types

- Secure mortgage pre-approval before house hunting

This strategic approach allows self-employed borrowers to balance tax efficiency in non-purchase years while positioning for mortgage qualification when needed. Resources on tax smarts and maximizing benefits for the self-employed in Canada provide additional planning insights.

Add-Back Strategies to Maximize Qualifying Income

Experienced mortgage professionals and accountants can identify legitimate add-backs that increase qualifying income without requiring higher tax payments:

💰 Common add-back opportunities:

Capital Cost Allowance (CCA): Depreciation claimed on vehicles, equipment, and property represents a non-cash expense that can often be added back to income[2]

One-time expenses: Major equipment purchases, business expansion costs, or unusual expenses in a single year

Personal use portions: If claiming vehicle or home office expenses, the personal-use portion may be added back

Non-recurring losses: Business losses from previous years carried forward

Discretionary expenses: Some lenders add back excessive meal/entertainment expenses or travel costs

Important: Add-backs require lender approval and detailed documentation. Not all lenders accept all add-back types, making professional guidance essential.

Working with Mortgage Professionals: Maximizing Approval Chances

Successfully navigating How Self-Employed Borrowers in Toronto Can Qualify for Mortgages Without T4 Slips in 2026 almost always requires expert guidance from experienced mortgage professionals.

Why Mortgage Brokers Are Essential for Self-Employed Applicants

Unlike traditional employees with straightforward applications, self-employed borrowers benefit enormously from broker expertise:

🎯 Lender matching: Brokers access 30+ lenders with varying self-employed policies, matching your specific situation to the most favorable options

📋 Documentation optimization: Experienced brokers know exactly which documents each lender requires and how to present income most favorably

💡 Strategic guidance: Brokers advise on timing, tax planning, and documentation preparation months before applying

🔍 Pre-screening: Brokers identify potential issues before formal applications, protecting your credit score from multiple rejections

💰 Rate negotiation: Access to wholesale rates and lender competition often yields better terms than direct bank applications

Broker vs. Bank comparison:

| Factor | Mortgage Broker | Direct Bank Application |

|---|---|---|

| Lender options | 30+ lenders | 1 lender |

| Self-employed expertise | Specialized knowledge | General lending guidelines |

| Documentation guidance | Comprehensive support | Basic requirements list |

| Approval probability | Higher (lender matching) | Lower (one-size-fits-all) |

| Rate competitiveness | Excellent | Variable |

| Cost to borrower | Free (lender-paid) | Free |

Preparing Your Application Package

Professional mortgage brokers typically request a comprehensive documentation package:

📑 Income documentation:

- ✅ 2-3 years of complete NOAs

- ✅ 2-3 years of T1 General tax returns (all schedules)

- ✅ 6-12 months of business bank statements (if using stated-income)

- ✅ Year-to-date profit/loss statement (current year)

📑 Business verification:

- ✅ Articles of Incorporation or business registration

- ✅ GST/HST account number documentation

- ✅ Business license (if applicable)

- ✅ Professional designations or certifications

- ✅ Contracts or client letters (for continuity proof)

📑 Personal financial documents:

- ✅ Personal bank statements (90 days)

- ✅ Credit report authorization

- ✅ Down payment source documentation

- ✅ List of assets and liabilities

- ✅ Government-issued identification

📑 Property documents:

- ✅ MLS listing or property details

- ✅ Purchase agreement (once in contract)

- ✅ Property tax assessment

- ✅ Condo documents (if applicable)

Pro tip: Organize documents in clearly labeled folders (digital or physical) with dates and descriptions. This professionalism signals financial competence to lenders.

Common Mistakes to Avoid

Even well-prepared self-employed applicants make errors that jeopardize approval:

❌ Applying too early: Before 2 years of tax history or with incomplete current-year filing

❌ Inconsistent information: Discrepancies between tax returns, bank statements, and application details trigger red flags

❌ Undisclosed debts: Failing to mention all credit obligations (lenders discover them anyway)

❌ Insufficient down payment verification: Unable to prove legitimate source of down payment funds

❌ Recent credit issues: New collections, late payments, or credit inquiries immediately before applying

❌ Overstating income: Claiming higher income than tax documents support

❌ Mixing business and personal finances: Lack of clear separation raises legitimacy concerns

❌ Ignoring tax compliance: Outstanding tax debts or unfiled returns automatically disqualify

Avoiding these pitfalls significantly improves approval probability and access to favorable rates.

Alternative Mortgage Solutions and Creative Strategies

When traditional and stated-income paths prove challenging, self-employed Toronto borrowers have additional options worth considering.

Co-Signers and Guarantors

Adding a co-signer with traditional employment income can bridge qualification gaps:

Benefits:

- ✅ Co-signer’s income and credit strengthen the application

- ✅ Access to prime lending rates

- ✅ Lower down payment requirements possible

- ✅ Faster approval process

Considerations:

- ⚠️ Co-signer assumes equal liability for the mortgage

- ⚠️ Impacts co-signer’s borrowing capacity

- ⚠️ Requires strong personal relationship and trust

- ⚠️ Legal implications if primary borrower defaults

Best candidates for co-signers:

- Parents helping adult children purchase first homes

- Spouses with traditional employment income

- Business partners with complementary income profiles

Equity-Based Lending Strategies

For borrowers with substantial down payments or existing home equity, equity-based lending focuses less on income verification:

Home Equity Lines of Credit (HELOCs):

- Leverage existing property equity

- More flexible income requirements

- Higher interest rates than traditional mortgages

- Useful for investment properties or renovations

Private mortgages:

- Minimal income documentation

- Focus on property value and equity position

- Short-term solutions (6-24 months)

- Higher rates (8-12%+) but accessible approval

Understanding how private mortgages work in Ontario helps borrowers evaluate this option realistically.

Bridge Financing and Transition Strategies

Self-employed borrowers often use temporary higher-cost financing with plans to refinance:

Common transition path:

- Initial purchase: Private or alternative lender (higher rate, flexible documentation)

- Build tax history: 1-2 years of consistent reported income

- Refinance: Switch to traditional lender at prime rates

Example:

- Year 1: Purchase with alternative lender at 7.5% using bank statements

- Years 2-3: Report strong business income, maintain perfect payment history

- Year 3: Refinance to traditional lender at 5.5%, saving $800+ monthly

This strategy allows immediate homeownership while working toward optimal financing. Information about mortgage refinancing and switching lenders provides valuable context for this approach.

Investment Property Considerations

Self-employed borrowers purchasing investment properties face additional complexity:

Rental income treatment:

- Lenders typically count 50-80% of projected rental income

- Requires lease agreements or rental market analysis

- May require landlord experience or property management plan

- Higher down payments often required (20-35%)

Portfolio lending:

- Borrowers with multiple properties may access specialized programs

- Demonstrated real estate investment experience valued

- Cross-collateralization opportunities

- Relationship-based lending with portfolio lenders

Real-World Examples: Toronto Self-Employed Mortgage Success Stories

Understanding how other self-employed Toronto borrowers successfully qualified provides valuable insights and encouragement.

Case Study 1: The Conservative Tax Filer

Profile:

- Freelance graphic designer, 4 years self-employed

- Gross revenue: $120,000 annually

- Aggressive tax deductions: Net income $62,000

- Excellent credit score: 750

- Down payment available: $80,000

Challenge: Reported income only qualified for $265,000 mortgage—insufficient for Toronto market

Solution:

- Worked with mortgage broker specializing in stated-income products

- Provided 12 months of business bank statements showing consistent $10,000 monthly deposits

- Lender calculated income at 60% of gross deposits: $72,000 qualifying income

- Approved for $310,000 mortgage at 7.8% interest rate

- Combined with $80,000 down payment, purchased $390,000 condo

Outcome: Successfully purchased property using bank statement program, plans to refinance after building 2 more years of higher reported income

Case Study 2: The Strategic Tax Planner

Profile:

- Self-employed IT consultant, 3 years in business

- Gross revenue: $180,000 annually

- Planned mortgage purchase 2 years in advance

- Target property price: $850,000

Strategy:

- Year 1: Claimed $75,000 in deductions, reported $105,000 income

- Year 2: Reduced deductions to $45,000, reported $135,000 income

- Year 3: Minimal deductions $30,000, reported $150,000 income

- Average qualifying income: $130,000

Documentation:

- 3 years of NOAs and T1 Generals

- Add-backs for CCA and one-time equipment purchases: +$15,000

- Final qualifying income: $145,000

- Excellent credit: 780

Outcome: Qualified for $620,000 mortgage at prime rate (5.4%), combined with $230,000 down payment (27%), purchased $850,000 Toronto home with conventional financing

Key lesson: Strategic tax planning 2-3 years before purchase enabled prime rate qualification and substantial savings versus alternative lending

Case Study 3: The New Business Owner with Co-Signer

Profile:

- Former employee turned business owner (1.5 years self-employed)

- Previous employment income: $95,000

- Current business income: $110,000 (only 1 year of tax history)

- Parent willing to co-sign

- Down payment: $60,000

Challenge: Insufficient self-employment history for traditional qualification

Solution:

- Added parent (retired, pension income $55,000, owns home free-and-clear) as co-signer

- Combined qualifying income: $110,000 + $55,000 = $165,000

- Parent’s excellent credit (810) strengthened application

- Qualified for insured mortgage with 10% down

Outcome: Approved for $540,000 mortgage at 5.6%, purchased $600,000 Toronto townhouse, plans to remove co-signer after 2 years of business history

Frequently Asked Questions

Q: Can I qualify for a mortgage with only one year of self-employment?

A: Traditional lenders typically require 2-3 years of tax history, but options exist for newer businesses. Alternative lenders may accept 1 year of strong income documentation combined with higher down payments (20%+), or you can explore stated-income products using bank statements. Having previous employment in the same field strengthens applications significantly.

Q: Will lenders accept my business bank statements instead of tax returns?

A: Yes, stated-income mortgage programs specifically accept 6-12 months of business bank statements as primary income verification[3][6]. However, these products typically carry interest rates 2-4% higher than traditional mortgages and may require stronger credit scores and larger down payments.

Q: How much down payment do I need as a self-employed borrower in Toronto?

A: Minimum down payments range from 5-20% depending on property value and documentation strength. While 5% is technically possible for insured mortgages under $1 million, self-employed borrowers often find 20%+ down payments provide access to better rates, more flexible documentation requirements, and conventional mortgage benefits[1][4].

Q: Can I use my corporation’s income for mortgage qualification?

A: Yes, incorporated business owners can use corporate income for qualification, but lenders typically require 2-3 years of corporate tax returns (T2), personal NOAs showing dividend or salary income, and Articles of Incorporation. Some lenders add personal salary/dividends plus a percentage of retained corporate earnings to calculate qualifying income.

Q: What credit score do I need as a self-employed mortgage applicant?

A: Minimum credit scores start at 600 for most programs[1][4], but self-employed borrowers benefit significantly from scores above 680 for prime lending access. Stated-income programs often require 650-700+ to offset documentation flexibility. Higher scores also improve interest rate offerings and approval probability.

Q: How does the stress test affect my maximum mortgage amount?

A: The stress test requires qualification at 5.25% or your contract rate plus 2%, whichever is higher[2]. This typically reduces maximum borrowing capacity by 20-25% compared to qualifying at the actual mortgage rate. For a borrower qualifying at $100,000 income, the stress test might reduce maximum mortgage from $550,000 to approximately $425,000.

Q: Can I refinance from a stated-income mortgage to traditional lending later?

A: Absolutely. Many self-employed borrowers use stated-income products as bridge financing, then refinance to traditional prime lending after accumulating 2-3 years of tax-reported income history. This strategy allows immediate homeownership while working toward optimal long-term financing. Understanding mortgage refinancing advantages for self-employed borrowers helps plan this transition.

Conclusion: Your Path to Homeownership as a Self-Employed Toronto Borrower in 2026

Understanding How Self-Employed Borrowers in Toronto Can Qualify for Mortgages Without T4 Slips in 2026 empowers entrepreneurs, freelancers, and business owners to achieve homeownership despite non-traditional income documentation. While the path requires more preparation than traditional employment, multiple viable routes exist—from tax-based qualification using NOAs and T1 Generals to stated-income programs accepting bank statements.

The key to success lies in strategic planning, comprehensive documentation, and expert guidance. Whether you choose to optimize tax reporting for traditional lending, leverage stated-income products for immediate qualification, or employ creative strategies like co-signers or bridge financing, Toronto’s self-employed professionals have more mortgage options in 2026 than ever before.

Actionable Next Steps

Ready to move forward with your self-employed mortgage application? Follow these concrete steps:

📋 Step 1: Assess Your Current Position

- Gather 2-3 years of NOAs and T1 Generals

- Calculate your average reported income

- Check your credit score and report

- Determine available down payment amount

- List all current debts and obligations

📋 Step 2: Consult with Professionals

- Connect with a mortgage broker experienced in self-employed lending

- Discuss your situation with your accountant regarding tax strategy

- Obtain pre-qualification to understand realistic borrowing capacity

- Explore multiple lender options through broker access

📋 Step 3: Optimize Your Documentation

- Ensure complete tax compliance (all returns filed, all taxes paid)

- Organize business documentation (incorporation, GST/HST registration, licenses)

- Prepare bank statements if considering stated-income route

- Document income stability and business continuity

📋 Step 4: Plan Your Timeline

- If purchasing within 6-12 months: Work with current documentation and explore all lender options

- If purchasing in 1-2 years: Consider strategic tax planning to optimize reported income

- If purchasing in 2+ years: Implement comprehensive income documentation strategy

📋 Step 5: Secure Pre-Approval

- Submit complete application package to broker

- Obtain formal pre-approval before house hunting

- Understand exact qualification amount and conditions

- Lock in rate (if applicable) and begin property search

The Toronto real estate market remains competitive, but self-employed borrowers equipped with knowledge, preparation, and professional support successfully secure mortgages every day. Your entrepreneurial success deserves to translate into homeownership—and with the right approach, it absolutely can.

For additional guidance on self-employed mortgage qualification, explore resources on opportunities for first-time homebuyers among self-employed Canadians and take the first step toward your Toronto homeownership goals today.

References

[1] Self Employed Mortgage Options Qualifications In Canada – https://www.nesto.ca/mortgage-basics/self-employed-mortgage-options-qualifications-in-canada/

[2] Buying A Home In Toronto As A Self Employed Individual – https://smithproulx.ca/buying-a-home-in-toronto-as-a-self-employed-individual/

[3] Self Employed Mortgage – https://www.ratehub.ca/self-employed-mortgage

[4] Self Employed Mortgage Requirements – https://www.frankmortgage.com/blog/self-employed-mortgage-requirements

[5] Self Employed – https://www.nbc.ca/personal/mortgages/self-employed.html

[6] Guide – https://tridacmortgages.com/services/self-employed-mortgage/guide/

[7] New Canada Mortgage Programs – https://peterpaley.com/new-canada-mortgage-programs/

[8] Self Employed Mortgage – https://www.rbcroyalbank.com/mortgages/self-employed-mortgage.html