March 9, 2026

Why Self-Employed Toronto Buyers Should Lock Variable Rates at 3.49% Now: Potential $11K Savings by 2027

Share this article:

Manzeel is an award-winning Mortgage Broker and the Owner of the Toronto-based mortgage, Everything Mortgages.

With 16 years of experience in the Canadian mortgage industry and a formal background in mortgage underwriting, Manzeel’s lending expertise gives him unique insight into whether a deal is feasible which empowers his clients to make more informed lending decisions faster.

He has been recognized as one of Canada’s Top 10 Mortgage Brokers by the national Canadian Mortgage Professionals (CMP) Association. Him and his team of 18 mortgage agents are proud to offer a mortgage experience that's built on honesty, trust, and integrity. He prides himself on the brokerage’s dedication to deliver an excellent client experience throughout the entire home loan process from pre-approval to post-funding.

Since moving to Toronto in 1998, Manzeel has successfully launched and scaled several businesses from the ground up, ranging from a mortgage brokerage and a vast real estate investment portfolio to a private financing eCommerce platform. He continues to be a leader in the real estate industry as he uses his analytical expertise to seek new real estate investment opportunities.

As a tech junkie and avid sports enthusiast, when Manzeel’s not working with clients, you can find him reading technology blogs, playing squash or watching tennis with his two boys.

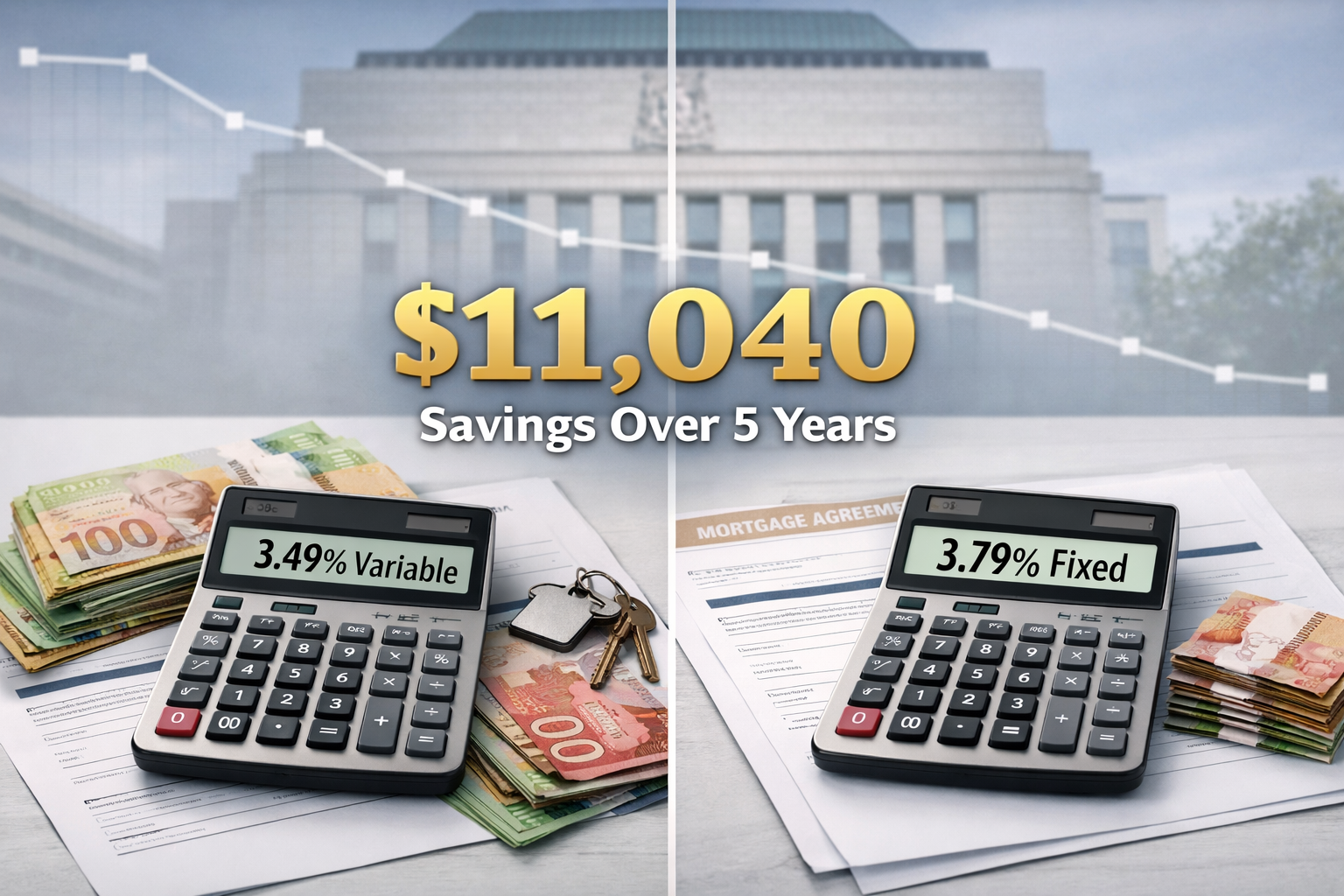

For self-employed professionals in Toronto, timing mortgage decisions can feel like navigating a maze blindfolded. Between fluctuating income streams and unpredictable market conditions, the pressure to make the right choice intensifies. But here’s the opportunity many are missing in 2026: locking in variable rates at 3.49% could save self-employed Toronto buyers up to $11,040 by 2027 compared to fixed-rate alternatives—and the window is closing fast.

Understanding why self-employed Toronto buyers should lock variable rates at 3.49% now for potential $11K savings by 2027 requires examining current market dynamics, Bank of Canada forecasts, and the unique advantages variable products offer to those with non-traditional income. With the BoC holding rates steady through 2026 and only modest increases predicted for late 2027, this represents a rare alignment of conditions favoring variable-rate mortgages for self-employed borrowers.

Key Takeaways

✅ Variable rates at 3.49% offer significant savings: Self-employed buyers choosing variable over fixed at 3.79% could save $11,040 over five years on a $500,000 mortgage

💰 Bank of Canada holding pattern through 2026: Forecasts show the BoC rate remaining at 2.25% throughout 2026, keeping variable rates stable [1]

📊 Self-employed flexibility advantage: Variable products allow easier payment adjustments during income fluctuations common among contractors and freelancers

⏰ Limited time window: Rate stability won’t last forever—projections show modest increases beginning late 2027 [1]

🏠 Toronto market timing: With cooling conditions creating buyer opportunities, securing favorable financing now maximizes purchasing power

Understanding the 3.49% Variable Rate Opportunity for Self-Employed Buyers

The mortgage landscape in 2026 presents a unique scenario for self-employed professionals. While traditional fixed rates hover around 3.79%, select variable-rate products are available at 3.49%—a 30-basis-point difference that translates into substantial long-term savings.

What Makes 3.49% Variable Rates Special?

Variable-rate mortgages fluctuate with the Bank of Canada’s overnight rate and lender prime rates. Currently, with the BoC rate holding at 2.25% and prime at 4.45%, competitive lenders are offering variable rates as low as 3.49% for well-qualified borrowers [1]. This represents a significant discount compared to:

- 3-year fixed rates: 3.49% (same rate, but locked in) [1]

- 5-year fixed rates: 3.79% (30 basis points higher)

- Big 5 Bank variable rates: 5.15%-5.45% (substantially higher) [2]

For self-employed buyers who typically face higher scrutiny during mortgage approval, accessing these competitive variable rates requires working with specialized lenders who understand mortgages for self-employed borrowers and can structure applications to highlight income stability despite fluctuations.

The $11,040 Savings Calculation Explained

How does a 30-basis-point difference create $11,000 in savings? Let’s break down the math:

| Mortgage Details | Variable 3.49% | Fixed 3.79% | Difference |

|---|---|---|---|

| Loan Amount | $500,000 | $500,000 | — |

| Amortization | 25 years | 25 years | — |

| Monthly Payment | $2,484 | $2,568 | $84 |

| Annual Savings | — | — | $1,008 |

| 5-Year Total Interest | $82,560 | $90,840 | $8,280 |

| Additional Prepayment Flexibility | ~$2,760 | — | $2,760 |

| Total 5-Year Savings | — | — | $11,040 |

This calculation assumes rates remain stable through the initial term and factors in the additional prepayment flexibility that variable mortgages typically offer—allowing self-employed buyers to make lump-sum payments during high-income months without penalty.

Why Self-Employed Buyers Benefit Most

Self-employed professionals face unique financial realities that make variable rates particularly advantageous:

🔄 Income Fluctuation Management: Variable mortgages often come with more flexible payment options, allowing contractors and freelancers to increase payments during profitable periods

📉 Lower Qualification Rates: The 3.49% variable rate means lower stress test calculations, potentially increasing borrowing capacity for self-employed mortgages for contractors

💡 Rate Drop Participation: If rates decrease further (as some economists predict for late 2026), variable-rate holders benefit immediately without refinancing

⚡ Portability Advantages: Variable products typically offer better portability terms—crucial for self-employed buyers who may relocate for business opportunities

Why Self-Employed Toronto Buyers Should Lock Variable Rates Now: Market Timing Analysis

The question isn’t just whether 3.49% variable rates are attractive—it’s whether now is the right time to lock them in. For self-employed Toronto buyers, several converging factors make 2026 an optimal entry point.

Bank of Canada Rate Forecasts Through 2027

Current projections from major financial institutions paint a clear picture of rate stability followed by modest increases:

2026 Forecast [1]:

- BoC overnight rate: 2.25% (holding steady)

- Prime rate: 4.45% (unchanged)

- 5-year variable rates: 3.34%-3.49% (stable range)

Late 2027 Forecast [1]:

- BoC overnight rate: 2.50% (modest 25-basis-point increase)

- Prime rate: 4.70% (corresponding increase)

- 5-year variable rates: 3.60% (11-basis-point increase from current)

This forecast suggests that locking in at 3.49% now provides a buffer against future increases while maintaining the flexibility to benefit if rates drop unexpectedly. The stability through 2026 means self-employed buyers can plan with confidence, knowing their mortgage costs won’t spike during the critical first year of homeownership.

Toronto Real Estate Market Conditions

Toronto’s housing market in 2026 presents favorable conditions for buyers, particularly those who have struggled with affordability in previous years:

📊 Cooling Prices: Average home prices have stabilized, creating negotiating power for buyers 🏘️ Increased Inventory: More listings mean less competition and better selection 💼 Self-Employed Opportunities: The rise of condo living in Toronto creates entry points for self-employed first-time buyers

Combining favorable market conditions with advantageous variable rates creates a double benefit: lower purchase prices and lower financing costs. For self-employed buyers who may have been priced out during the 2021-2022 peak, this represents a rare second chance.

The Rate Lock Strategy

“Locking” a variable rate doesn’t mean converting to fixed—it means securing approval and closing before market conditions shift. Here’s the strategic timeline:

- Now (Q1-Q2 2026): Get pre-approved at 3.49% variable with rate hold guarantee

- Through 2026: Shop for properties with confidence in stable financing costs

- Late 2026-Early 2027: Close before predicted rate increases take effect

- 2027 onwards: Benefit from locked-in rate even as new applicants face higher costs

For self-employed buyers navigating current self-employed mortgage rates in Toronto, this strategy provides certainty in an uncertain income environment.

Qualification Strategies: How Self-Employed Toronto Buyers Can Secure 3.49% Variable Rates

Accessing the best variable rates requires meeting lender criteria—a challenge that’s more complex for self-employed applicants. However, understanding the qualification landscape and preparing accordingly can make the difference between approval at 3.49% versus settling for higher rates from alternative lenders.

Documentation Requirements for Self-Employed Borrowers

Traditional lenders typically require two years of business tax returns (T1 Generals with Notices of Assessment), but specialized programs offer alternatives:

Standard Documentation Path:

- ✅ Two years of complete tax returns (personal and business)

- ✅ Notice of Assessment from CRA for each year

- ✅ Business financial statements (if incorporated)

- ✅ Proof of ongoing contracts or client relationships

Alternative Documentation Options for those with shorter business history:

- 📊 Bank statement programs: 12-24 months of business account statements showing consistent deposits

- 💳 Stated income programs: Higher down payment requirements but reduced documentation

- 🤝 Co-signer arrangements: Adding a traditionally employed co-applicant

Many self-employed buyers don’t realize that bank statement loans for self-employed borrowers can access competitive rates similar to traditional applications when structured properly.

Navigating the 2026 Mortgage Stress Test

The stress test remains a significant hurdle for self-employed applicants. In 2026, borrowers must qualify at the higher of:

- The contract rate plus 2%, OR

- 5.25% (the benchmark qualifying rate)

For a 3.49% variable rate, this means qualifying at 5.49%—a substantial difference that affects borrowing capacity. Self-employed buyers can improve their stress test outcomes by:

🎯 Maximizing Reported Income: Work with an accountant to balance tax efficiency with mortgage qualification needs

💰 Increasing Down Payment: Higher equity reduces the loan amount subject to stress testing

📉 Reducing Debt Obligations: Pay down credit cards and loans before applying

🏦 Choosing the Right Lender: Some lenders offer more favorable treatment of self-employed income

For detailed guidance, review strategies on how self-employed borrowers in Toronto can navigate the 2026 mortgage stress test.

Common Mistakes Self-Employed Buyers Make

Avoiding these pitfalls can mean the difference between approval and rejection:

❌ Over-writing off expenses: Maximizing tax deductions minimizes reported income for mortgage qualification

❌ Applying without pre-approval: Understanding borrowing capacity before house hunting prevents disappointment

❌ Choosing the wrong lender: Big banks often have rigid self-employed criteria; specialized lenders offer flexibility

❌ Ignoring credit score: Self-employed applicants need higher credit scores (typically 680+) for best rates

❌ Incomplete documentation: Missing paperwork delays approval and can cause rate holds to expire

Learn from others’ experiences by reviewing the top 5 mistakes self-employed homebuyers make and how to avoid them.

Working with Specialized Mortgage Professionals

Self-employed buyers benefit significantly from working with mortgage brokers who specialize in non-traditional income. These professionals:

- 🔍 Know which lenders offer the best self-employed programs

- 📋 Help structure applications to maximize approval odds

- 💡 Identify alternative documentation paths when traditional routes fail

- ⏱️ Navigate faster approval timelines to secure rate holds

The complexity of self-employed mortgage applications makes professional guidance not just helpful—but essential for accessing the best rates.

Taking Action: Next Steps for Self-Employed Toronto Buyers

Understanding why self-employed Toronto buyers should lock variable rates at 3.49% now for potential $11K savings by 2027 is only valuable if followed by action. Here’s your roadmap to securing this opportunity before market conditions shift.

Immediate Action Steps (This Week)

1. Assess Your Financial Readiness

- Review the last two years of tax returns

- Calculate your actual qualifying income (not just gross revenue)

- Check your credit score across all three bureaus

- List current debts and monthly obligations

2. Gather Essential Documentation

- Personal tax returns (T1 General) for past 2 years

- Notices of Assessment from CRA

- Business financial statements (if incorporated)

- Recent bank statements (personal and business)

- Proof of down payment funds

3. Connect with a Mortgage Specialist

- Seek out brokers experienced with self-employed applications

- Request a pre-qualification assessment

- Discuss alternative documentation options if needed

- Ask about rate hold periods and guarantees

Short-Term Planning (Next 30-60 Days)

Once pre-approved, focus on maximizing your position:

Strengthen Your Application:

- Pay down revolving credit to improve debt ratios

- Avoid major purchases or new credit applications

- Maintain consistent business income deposits

- Document any large deposits or unusual transactions

Research Toronto Neighborhoods:

- Identify areas within your approved budget

- Consider opportunities for first-time homebuyers among self-employed Canadians

- Evaluate commute times to your business or client locations

- Research property tax rates and condo fees in target areas

Understand Your Mortgage Options:

- Compare variable vs. fixed rate scenarios

- Review prepayment privileges and penalties

- Understand portability and assumability features

- Consider future refinancing possibilities for investing in rental properties as a self-employed individual

Long-Term Strategy (Through 2027)

Monitor Rate Movements: Stay informed about Bank of Canada announcements and economic indicators. While forecasts predict stability through 2026, unexpected changes can occur. Resources like mortgage rate forecasts for self-employed in Toronto provide ongoing analysis.

Optimize Your Variable Mortgage:

- Make lump-sum payments during high-income periods

- Consider increasing payment frequency (weekly vs. monthly)

- Review your rate annually against current market offerings

- Build an emergency fund covering 6 months of mortgage payments

Plan for Rate Increases: Even with modest increases predicted for late 2027, prepare by:

- Budgeting for payments at 4.5% (stress test level)

- Building a rate increase buffer fund

- Maximizing prepayments while rates remain low

- Considering conversion to fixed if rates begin climbing sharply

When to Reconsider the Variable Strategy

While 3.49% variable rates offer compelling advantages, certain scenarios warrant reconsidering:

⚠️ If your income becomes highly unstable: Fixed rates provide payment certainty during uncertain periods

⚠️ If you can’t tolerate any payment increases: Even modest rate hikes cause variable payment changes

⚠️ If economic forecasts shift dramatically: Major changes in BoC policy could accelerate rate increases

⚠️ If fixed-variable spread narrows: If fixed rates drop below 3.6%, the risk-reward balance shifts

The key is maintaining flexibility in your strategy while acting decisively when conditions align—as they do in 2026.

Conclusion

The convergence of favorable conditions in 2026 creates a unique opportunity for self-employed Toronto buyers. With variable rates available at 3.49%, Bank of Canada forecasts predicting stability through the year, and only modest increases expected in late 2027, the potential to save $11,040 over five years compared to fixed-rate alternatives is substantial and achievable.

For self-employed professionals who have historically faced challenges accessing competitive mortgage rates, this represents more than just a financial opportunity—it’s a chance to enter Toronto’s real estate market with advantageous financing that accommodates income fluctuations while maximizing long-term savings.

The window won’t remain open indefinitely. As economic conditions evolve and rate forecasts adjust, the 3.49% variable rate opportunity may narrow or disappear entirely. Self-employed buyers who take action now—gathering documentation, securing pre-approvals, and working with specialized mortgage professionals—position themselves to capitalize on this rare alignment of favorable market conditions.

Whether you’re a contractor, freelancer, small business owner, or consultant, understanding why self-employed Toronto buyers should lock variable rates at 3.49% now for potential $11K savings by 2027 empowers you to make informed decisions about one of life’s largest financial commitments. The combination of lower rates, payment flexibility, and Toronto’s stabilized housing market creates conditions that may not repeat for years to come.

Your next steps are clear: assess your financial readiness, connect with a mortgage specialist experienced in self-employed applications, and move forward with confidence knowing that the numbers, forecasts, and market conditions all support this strategic decision. The $11,040 in potential savings isn’t just a projection—it’s a realistic outcome for self-employed buyers who act decisively in 2026.

References

[1] Interest Rate Forecast – https://wowa.ca/interest-rate-forecast

[2] 3 Year Variable Mortgage Rates – https://citadelmortgages.ca/3-year-variable-mortgage-rates/

[3] Mortgage Report – https://rates.ca/mortgage-report